Nickel surplus to build

Nickel has had a tumultuous year amid Russia’s invasion of Ukraine in February and March’s short squeeze, and the subsequent temporary suspension of LME nickel trade. The short-term outlook for nickel remains bearish amid a deteriorating macro picture and sustained market surplus.

Nickel price slips on recession fears

The metals complex has had a volatile year. Most metals performed strongly in the first quarter given the growing supply uncertainty due to Russia’s invasion of Ukraine. However, a stronger US dollar, rising rates and weaker downstream demand weighed heavily on metals markets for the remainder of the year. Nickel is the standout across the complex, managing to hold onto year-to-date gains. Still, the LME price is down significantly from its year-to-date highs in March following a short squeeze, as recession fears have undermined market sentiment.

Volatility in the nickel market has become more common in recent months with reduced liquidity ever since the short squeeze seen back in March, when fears of sanctions on Norilsk Nickel coincided with a huge short bet by the world’s largest stainless steel producer, Tsingshan. This caused prices to more than double in a matter of days. The LME was forced to suspend trading for a week and cancel billions of dollars’ worth of nickel trades.

The LME has subsequently imposed price limits for the first time and introduced requirements for disclosure of business done over the counter via derivatives to the exchange.

LME volumes have declined since then as many traders have reduced activity or cut their exposure due to a loss of confidence in the LME and its nickel contract after its handling of the March short squeeze. Volumes on the LME three-month nickel contract since March have been 30% of levels in the six months before the market chaos following the short squeeze.

These low levels of liquidity have left nickel exposed to sharp price swings – even amid small shifts in supply and demand balances.

Most recently, nickel prices on the LME spiked briefly to hit the LME’s daily trading limit of 15%, reaching almost $31,000/t, on a report of an explosion at an Indonesian plant. Gains were pared after the facility’s owner denied any incident. That was followed by a 5% rise the following day after a nickel mine in New Caledonia, which supplies Tesla, cut its 4Q production forecast.

In an effort to stabilise the recent volatility, the LME said it undertook “enhanced monitoring” of market participants’ trading activities and lifted initial margins for nickel trades by 28% to $6,100/t.

The LME recently defended its decision in a legal filing following lawsuits from Elliott Investment Management and Jane Street, saying that the spike in nickel prices on 8 March would have led to margin calls of about $19.75 billion if the trades hadn’t been cancelled. The exchange said that subsequent analysis has shown that at least seven clearing members would have gone into default. On the morning of 8 March, six members had not paid their overnight margin payments, totalling $2 billion. The bourse said that it saw the risk of a ‘death spiral’ without nickel trade cancellations.

We expect more near-term volatility to continue until the LME rebuilds trust in the benchmark nickel contract, volumes pick up again and the market’s confidence in it recovers.

Weak stainless steel output pushes nickel to surplus

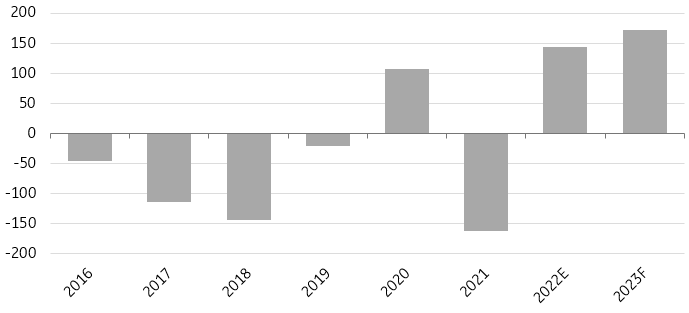

Continued weakness in demand from the stainless steel sector has meant that the global nickel market is expected to be in surplus this year. However, the surplus is mostly in the class 2 - ferronickel and NPI - market. The LME deliverable class 1 market has been relatively tight with LME stocks falling by around 50kt since the start of the year and recently hitting a 14-year low. The reported LME stocks are now below three weeks of consumption – another factor driving the price swings in the LME nickel contract.

The International Nickel Study Group (INSG) expects nickel to record a surplus of 144kt this year and another 171kt in the next year. Historically, market surpluses have been linked to the LME deliverable class 1 nickel but in 2023 the surplus will be mainly due to class 2 and nickel chemicals – predominantly nickel sulphate, which is used in batteries, according to the INSG.

The INSG has also cut its global demand forecast for this year from 8.6% in May to 4.2%, reflecting a slide in stainless steel production.

Nickel supply/demand market balance (kt)

Source: INSG, ING Research

Global stainless growth to fall

Stainless steel is still key for nickel demand, accounting for 70% of total nickel consumption. Although demand from the battery sector is growing rapidly, making up around 5% of total demand at the moment, it isn’t enough to offset a slowdown in traditional sectors like construction.

China’s strict zero-Covid policy has hurt the country’s construction sector and has weighed on demand for nickel.

However, more recently, hopes have grown that fresh stimulus measures by China could boost demand for industrial metals after moves to shore up the country’s property sector and ease its Covid restrictions.

China's recent relaxation of its Covid-related quarantine measures includes a reduced quarantine period for inbound travellers and close contacts of those who have tested positive while secondary contacts will no longer need to be traced. China is also pushing for greater vaccination of the elderly following protests over strict Covid curbs across the country - which are likely to weigh on sentiment further. At the same time, China’s total case count remains elevated, while Beijing has reported its first Covid deaths in six months.

China’s relaxation of its Covid policy would have a significant effect on the steel market, and by extension on the nickel market. However, we believe the government is likely to stick to its zero-Covid policy through the winter and may only look to ease some of the curbs further after the National People’s Congress due to be held in March or April next year.

Indonesia supply growth in focus

Meanwhile, Indonesia’s production of nickel is surging to meet growing demand from the electric vehicle (EV) battery sector.

The country’s output was up 41% year-on-year in the first seven months of 2022, according to INSG. Year-to-date production of 814,000 tonnes accounted for 47% of the global total, compared with 38% over the same period of 2021.

Indonesia is the world’s largest nickel producer, accounting for 38% of global refined supply. The country holds a quarter of the world’s reserves of the metal with much of Indonesia’s output being of lower purity and used in stainless steel.

Indonesia is expected to produce between 1.25 and 1.5 million tonnes of nickel this year, more than 40% of world mined production estimated at between 3 million to 3.2 million tonnes, according to data from USGS.

We believe rising output in Indonesia will pressure nickel prices next year.

Supply risk around Russian metal remains

There are still plenty of supply risks around Russian metal. The LME has decided not to suspend Russian nickel but the threat of government sanctions will remain as long as the war in Ukraine rages on.

The LME was looking at potentially banning the delivery of Russian metal into its warehouses, limiting Russian flows or taking no action. The exchange said that it is likely that additional tonnages of Russian metal will, in time, if not immediately, be warranted in the LME's physical network.

Russia is the third largest primary nickel producer after Indonesia and China and the largest exporter of refined nickel metal – the type deliverable on the LME. Europe is one of the key destinations for Russian metal.

Everything depends on how many players choose not to take Russian metal in their 2023 supply contracts unless there are government sanctions. If we see more Russian metal being delivered into LME warehouses, it could potentially mean that LME prices trade at discounted levels to the actual market.

However, the LME said that the proportion of Russian metal in LME warehouses has not changed significantly over the discussion paper period.

In 2013, 65% of LME nickel inventories were of Russian origin. In more recent years, this has ranged between 0-20%. According to the latest data from the LME, only 0.5% of live nickel tonnage in its warehouses was of Russian origin.

The LME said it will publish a monthly report, starting in January 2023, which will provide the percentage of live tonnage of Russian metal on-warrant in order to provide more transparency.

Prices to remain under pressure as surplus builds

We forecast nickel prices to remain under pressure in the short term as a surplus in the market builds, however, the tightness in the class 1 market is likely to offer some support. We see prices hovering between $20,000/t and $20,500/t over the first two quarters of 2023 before gradually increasing to $21,000/t in 3Q and $22,000/t in 4Q as the global growth outlook starts to improve.

ING forecast

Source: ING research

Read the original analysis: Nickel surplus to build

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.