NFP Preview: Four reasons why June's jobs report could be a dollar downer

- June's Nonfarm Payrolls figures could fall short of elevated expectations once again.

- Fed Chair Powell created high expectations, which will be hard to be met.

- Wage gains could reverse the previous trends, lowering inflation expectations.

- NFP could trigger a reversal of dollar gains.

Time for King Dollar to be knocked off the throne? June's highly anticipated Nonfarm Payrolls report – due on July 2 and ahead of a long weekend – could provide other currencies an opportunity to bring the greenback back to the ground.

There are four reasons to expect the NFP to down the dollar:

1) Reopening is hard

There is no Undo button for returning the economy to pre-pandemic levels – as the two disappointing jobs reports have shown. The economy has sprung back to fast growth in the spring, but while restoring jobs for those that have been furloughed may be relatively easy, matching employers' needs with employees' desires is a more complex task.

Source: FXStreet

The US gained 559,000 positions in May – extremely high in pre-pandemic times – but falling short of estimates once again. Some blame generous unemployment benefits and stimulus checks, while others mention that the covid crisis is far from over – some fear returning to being in contact.

The skill mismatch mentioned earlier was also compounded by a shortage of raw materials. Have all these issues been resolved between May and June? Probably not, yet expectations remain elevated. The economic calendar is pointing to an increase of some 700,000 jobs in June, substantially above May's hiring.

All this may lead to a third consecutive disappointment.

2) Powell's high expectations

A weaker number than economists estimate would become even worse given elevated expectations created by Federal Reserve Chair Jerome Powell. In his post-rate decision presser, the world's most powerful central banker declared that job growth would accelerate in the coming months.

Moreover, by basing the Fed's hawkish turn on this outlook rather than on outcomes, he raised the bar. Therefore, even a satisfactory figure would serve as a reminder that restoring some 7.6 million jobs lost in the pandemic will take a long time. That could weigh on the dollar.

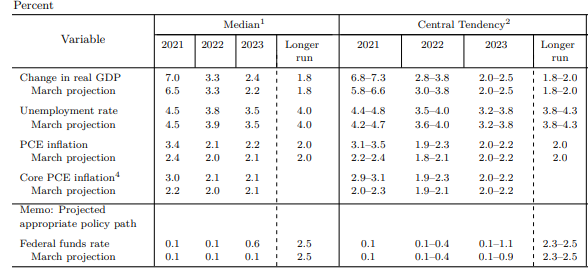

Fed projections, June vs. March:

Source: Federal Reserve

3) Wages could downplay inflation expectations

The central bank's second mandate is keeping price stability. After sticking to the script that rising inflation is only transitory, Powell and his colleagues acknowledged there is a chance that higher costs are here to stay. They upgraded their forecasts.

Nevertheless, jumps in lumber prices and also computer chips have begun unwinding. The theory that temporary bottlenecks – not a structural change – are behind most of the gains may receive more impetus if wage growth cools down.

Average Hourly Earnings rose by 0.5% in May and 0.7%, both elevated levels and beating expectations. Similar to weak job gains, another upside surprise in salaries could repeat itself for the third time. However, wages are more likely to decelerate as job growth remains weak, rather than beat expectations.

Source: FXStreet

If Americans have marginally less money in their pockets, that could ease inflation pressures and push the dollar down as well.

4) NFP as a reversal trigger

Money managers adjust their portfolios at the end of the month, and this usually results in some unwinding of the trends seen earlier in the month. Not this time. June saw the dollar gaining – mostly as a result of the Fed's hawkish tilt – and concluding the month has not resulted in any dollar downfall.

Investors seem to be keeping their powder dry ahead of the all-important NFP. It might take only a marginal miss – or even the jobs report merely meeting estimates – to trigger a move in the other direction. That means the greenback giving some ground.

EUR/USD monthly chart, showing June resulted in a fall of over 300 pips:

Conclusion

The dollar has room to fall in response to June's Nonfarm Payrolls report due to elevated expectations, undoing of existing positions and more.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.