New York close: The bubbly’s gone flat – Markets face the morning-after reality, “now what”?

Markets

Markets just gave back a huge chunk of Tuesday’s euphoria, diving 3% as the U.S.-China trade standoff grinds on. The optics are ugly — not just for investors, but for global diplomacy. No one likes being forced to pick sides, and right now the U.S. looks more like the classroom bully than the global ringleader.

And here's the bigger issue: there’s no US fiscal firepower waiting in the wings, and the Fed hasn’t even moved close to the rate cut lever yet. That puts stocks — and global sentiment — in a delicate spot. Confused, fragile, and exposed.

Meanwhile, the bond market still isn’t reflexing like it used to. Tens are stuck north of 4.40% despite the equity bloodbath — a subtle but growing “Sell America Inc.” signal. That’s a carryover from the basis trade blowout, and it’s not going away quietly.

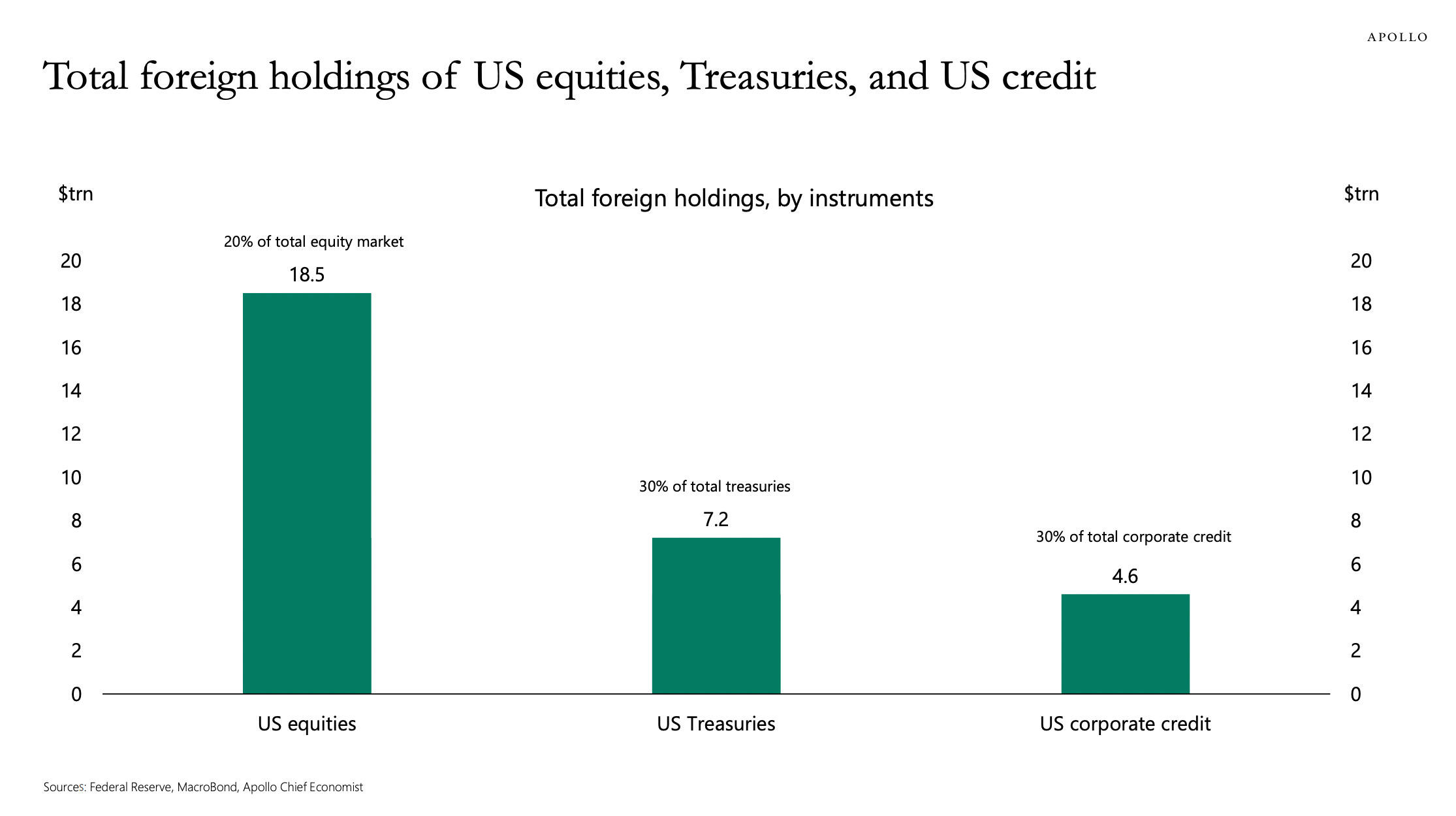

If we do flip entirely into “Sell America Inc.” mode, that chart below Torsten Sløk flagged really hit me — not just as a trader, but as someone who's been watching market plumbing for decades. It’s more than just scary, it’s a full-blown flashing red light on the dashboard.

I’ve been watching the setup build for weeks: ballooning Treasury issuance, foreign buyers stepping back, basis trade cracks widening... and now we’ve got yields ripping higher not on inflation fears, but on pure plumbing stress. That’s not your typical risk-off — that’s the market starting to question the depth of demand for U.S. paper.

If that sentiment sticks, we’re not talking about a blip — we’re staring down a structural repricing of U.S. assets. And it won’t stop at local stocks or bonds. This bleeds into FX, EM debt, commodities, vol — the whole complex.

So yeah, if the vigilantes come swinging and that dollar correlation starts to flip, watch out below !!

So what's the safe trade here? Honestly? Right now, it might be cash under the mattress until the dust settles. Treasuries aren’t catching a bid like they should in risk-off mode. Spreads are widening. Yields look more likely to grind toward 4.50%, maybe even 4.75% in a worst-case scenario.

That’s a problem. Because if risk can’t rally and bonds won’t bounce, we’re left floating in a vacuum — and the market hates a vacuum.

The view

The 90-day pause offers breathing room — not a pivot. And judging by the tone in rates and FX, a few desks are already fading the relief and pricing in the reality that negotiations might not dilute the tariff threat all that much. Uncertainty still reigns, This story isn’t done or undone — and the risk of meaningful economic drag remains firmly in play.

China didn’t blink — and made that crystal clear Thursday, slapping 84% tariffs on U.S. imports and targeting 18 American firms with new restrictions. It’s a direct signal: Beijing won’t be cowed, and any illusion of de-escalation is now firmly off the table.

Even with Trump’s 10% universal tariffs still on the board — despite the headline hiatus — the message is unmistakable: the U.S. and China are now deep in the trenches of a full-blown trade war.

The optics are messy, the battle lines are redrawn, and the tape is driven by confusion.

Champagne popped, risk screens lit up green, and it felt like everyone exhaled at once for a hot minute. But after the high-fives came the inevitable hangover question: Now what?

It might be too early to call it definitive, but today’s market action suggests some corners are starting to absorb a harder truth: despite Trump’s walk-back, the U.S. still looks poised to impose stiff tariffs.

Forex markets

U.S. inflation undershot nearly everyone’s forecasts in March — and that alone was enough to weigh on the dollar. But let’s be real: even an upside surprise wouldn’t have saved the buck in this tape. The market’s lost its reflexivity to data, and it might stay that way for a while.

As I flagged earlier this week, it might be time to bring money home. There’s just no real advantage to holding dollars right now. Even CNH is catching a bid on fiscal stimulus hopes — something Washington is sorely lacking. The U.S. is running on fumes while Beijing still has war chest room to flex.

I’m officially off the barbell — closed my synthetic long EURCNH trade after EURUSD tagged 1.1200. Probably an overshoot, but that’s where the juice was. In hindsight, the real trade was simply long EURUSD. No one’s taking on the PBoC right now — they’ve got too much ammo.

But thank God for Gold !!!

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.