![]() ING Global Economics Team

ING Global Economics Team

ING Economic and Financial Analysis

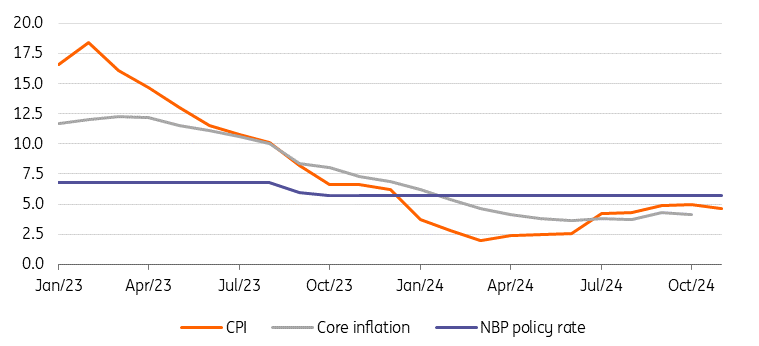

Poland’s rate-setters are expected to leave interest rates unchanged this week, with the key policy rate at 5.75%. The response from the National Bank of Poland’s governor to a dovish shift in local fundamentals and the external environment remains highly uncertain. We anticipate a rate cut in the second quarter of next year, or even as early as March.

The Monetary Policy Council’s (MPC's) decision on rates will follow two days of meeting and will be announced on Wednesday afternoon. On Thursday, National Bank of Poland (NBP) Governor Adam Glapiński will provide their rationale and the broader context during a press conference. We and the market consensus assume that rates will remain unchanged, with the key policy rate still at 5.75%.

Statements from the president and the majority of Council members in recent weeks have focused mainly on the fact that discussions about rate cuts will begin in March next year. For a while now, Glapiński has communicated that the MPC brought CPI to 2.0% in March and the recent headline CPI spike was caused by regulatory decisions by the government to unfreeze energy prices. He forgot to add that core inflation has persistently stayed above 4%YoY and is very sticky.

The government has decided to extend the energy prices freeze which means the 2025 average CPI will be 1.3pp lower than the November NBP projection. The March inflation projection should present this lower CPI path and will be very important in this context as it will incorporate regulatory decisions on continued electricity freezing and the loose fiscal policy stance in 2024-25.

Therefore, decisions about cuts before March next year would be a big surprise for the market and a communication problem for the MPC. Although headline CPI inflation declined to 4.6%YoY in November from 5.0% in October, this was mainly due to statistical base effects on fuel prices. Inflation is well above the NBP target of 2.5% with a tolerance band of +/-1 percentage point, and is expected to trend upwards in the first quarter of 2025. As long as headline CPI is rising, the MPC should refrain from easing.

CPI and core inflation and NBP policy rate, YoY, %

Source: CSO and NBP

Governor's reaction to dovish shift in local fundamentals and external backdrop is very uncertain

Since central bank decisions are stated to be data-dependent, recent data suggests an increasing number of factors justifying rate cuts or even earlier easing.

Keeping rates unchanged means a gradual increase in the restrictiveness of NBP’s monetary policy in the coming months. Externally, expectations have grown for deeper ECB easing (to 1.75%) due to the negative impact of Trump's policies on the eurozone, in addition to rate cuts by major central banks (75bp cuts by both the Fed and ECB in the current easing cycles, and in the CEE region – including the most hawkish Czech National Bank).

Local fundamentals also call for easing i.e. a gradual decline in inflation expectations, falling corporate profitability, and a deepening in private investment activity data for the third quarter.

Also, the latest GDP structure data in the third quarter is very surprising as it showed that the dynamics of private consumption (just 0.3% YoY only) were significantly below market expectations and the NBP’s November projection (2.8% YoY). This may be only partly attributed to the catastrophic floods in South-West Poland in September.

The discussion on interest rate cuts is expected in March 2025

In this context, the most important thing for us is how the latest GDP structure data will be interpreted in the statement after the MPC meeting and during the NBP press conference. If taken as a lasting trend of lower household spending, it opens up space for a faster pace of monetary policy easing after March next year. We see the odds growing that the MPC decides to surprise markets with the first cut in March and by 50bp rather than 25bp.

On the other hand, with the consumption underperformance regarded as transitory, Governor Glapiński is likely to declare that the outlook for monetary policy is broadly unchanged, even after the extension of the electricity price freeze through the majority of 2025. In such a case, the Council is unlikely to start discussing rate cuts until it sees a sustainable reversal in the inflation trend in the March 2025 projections.

Read the original analysis: National Bank of Poland preview: MPC to hibernate until March

Content disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/content-disclaimer/

Recommended Content

Editors’ Picks

EUR/USD stays defensive near 1.0500 amid French political jitters

EUR/USD is battling 1.0500 in the European session on Wednesday. The pair trades with caution amid renewed US Dollar buying and French political uncertainty as the government faces a no-confidence vote in a busy day ahead. US data, Lagarde and Powell eyed.

GBP/USD bounces back toward 1.2700 ahead of US data, Powell

GBP/USD picks up fresh bids and reverts toward 1.2700 in European trading on Wednesday. The pair reverses dovish BoE Governor Bailey's remarks-led drop as traders reposition ahead of US ADP Jobs data, ISM Services PMI data and Fed Chair Powell's speech.

Gold price treads water near $2,640, Fed Chair Powell's speech eyed

Gold price attracts some sellers following an intraday uptick to the $2,650 supply zone in the early European session on Wednesday. The precious metal, however, remains confined in a familiar range held over the past week or so as traders seem reluctant to place aggressive directional bets ahead of Fed Chair Jerome Powell's speech.

ADP report expected to show US private sector job growth cooled in November

The ADP Employment Change report is seen showing a deceleration of job creation in the US private sector in November. The ADP report could anticipate the more relevant Nonfarm Payrolls report on Friday.

The fall of Barnier’s government would be bad news for the French economy

This French political stand-off is just one more negative for the euro. With the eurozone economy facing the threat of tariffs in 2025 and the region lacking any prospect of cohesive fiscal support, the potential fall of the French government merely adds to views that the ECB will have to do the heavy lifting in 2025.

Best Forex Brokers with Low Spreads

VERIFIED Low spreads are crucial for reducing trading costs. Explore top Forex brokers offering competitive spreads and high leverage. Compare options for EUR/USD, GBP/USD, USD/JPY, and Gold.