Monetary desynchronization between the ECB and the Federal Reserve and the Euro

As expected, the ECB has lowered its policy rate, despite the upward revision of the staff inflation forecast. In the US, the very strong labour market report for the month of May will probably make the Fed even more cautious in deciding on a first rate cut. Until we have resynchronisation -with both central banks being in rate cutting mode-, there should be more desynchronisation, reflecting a difference in the disinflation cycle in the US versus the Eurozone. There is concern that this might weaken the euro versus the dollar and possibly weigh on the ECB’s policy autonomy. Such fears are unwarranted. Moreover, it would require a significant depreciation of the euro -something which seems very unlikely at the current juncture- for the ECB to be constrained by the euro in setting its policy rate. it is also important to look at the US side of the EUR/USD rate. A ‘high US rates for longer’ environment means more uncertainty about the growth outlook, which entails a tail risk for US short term interest rates and hence the dollar. When reflecting about exchange rates, the entire distribution of possible outcomes should be considered.

For a central bank, being credible matters more than anything else. In the absence of credibility, inflation expectations become unanchored, and the effectiveness of monetary policy takes a hit. Credibility is all about consistency. Firstly, time consistency, which means acting in line with the guidance that has been provided previously. In recent weeks the guidance from several ECB Governing Council members had become increasingly clear that the June meeting would see its first rate cut in this cycle. Against this background, not acting was out of the question, despite the uptick in the latest inflation data. Secondly, policy consistency, which means acting in line with its mandate and its reaction function. Given the rate cut, despite the upward adjustment of the ECB staff inflation forecast, the post-meeting press conference saw a strong insistence that the decision was only “removing a degree of restriction”1, that policy remained restrictive and that further decisions would be data dependent. Unsurprisingly, 2-year German yields rose about five basis points (bp) on the news. The next day, the release of a very strong labour market report in the US2 caused a similar increase in German yields on the back of a 10 bp jump in 2-year US Treasury yields. These developments are likely to intensify the debate on policy desynchronisation between the ECB and the Federal Reserve. The latter will probably be even less inclined than before to start cutting the federal funds rate whereas the former is expected to continue reducing the deposit rate, albeit at a gradual pace.

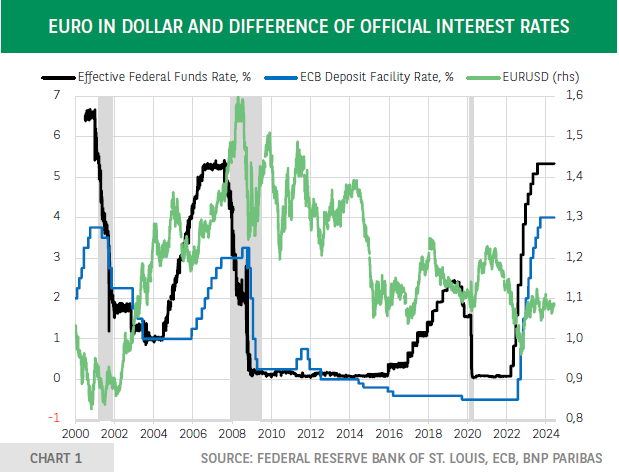

This means that until we have resynchronisation -with both central banks being in rate cutting mode-, there should be more desynchronisation. This shouldn’t be a surprise because it simply reflects a difference in the disinflation cycle in the US versus the Eurozone. However, there is concern that this might weaken the euro versus the dollar, thereby -through its impact on import price and inflation in general- complicating matters for the ECB and possibly even weighing on its policy autonomy. Such fears are unwarranted. Firstly, there is a very loose relationship between the EUR/USD rate and the difference in policy rates (chart 1).

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.