Markets took Powell’s “Fed on hold” remarks very much in stride

Outlook

Markets took Powell’s “Fed on hold” remarks very much in stride, since they had already come to the same conclusion. We get the Beige Book later today but it’s not likely to deliver anything new. Markets also waved off remarks from the IMF about US over-indebtedness, while appreciating the new forecast of US growth up 2.7% this year, a whopping 1.2% higher than the forecast only 6 months ago.

You don’t have to work very hard to hear the most important thing the central bank chiefs are saying—they are data-dependent. ECB chief Lagarde gave a lengthy interview on US TV and every time the reporter asked a tricky question, she retreated to data-dependency. Still, the message is that the ECB is not a lackey to the Fed. Markets continue to see the ECB moving before the Fed, in June.

Two factors dominate—receding expectations of Fed rate cuts and looming war in the Middle East. Mr. Powell told us yesterday that the Fed is okay with deferring the first hike until the data looks more trended downward, something the Q1 data screwed up, but a hike is not on the table. In the Israeli war front, nobody knows anything for sure, but the fear gauge is rising higher every day on the idea that no government can defer a response to what Iran threw at Israel. The quest for a safe space continues, favoring the dollar.

While some EM currencies just fell off the cliff—see the chart of the peso—the worrying currency now is the Japanese yen. This is not entirely about the level, but rather the speed of the move, something the MoF has named over the years as justification for intervention. Sure enough, the dollar/yen has levelled off and lost upward momentum over the past 24 hours.

Forecast

The dollar rally was getting a little crazy and now is starting to stall. Elsewhere, other assets also took a breather, including equities, oil, gold, and some commodities. The next stage “should” be the pullback that almost always follows a shotting star. We do not expect the pullback/bounceback to be very big or last very long for the simple reason that the yield differentials favor the dollar and so does the quest for a safe room in geopolitics.

But wait, there’s a fly in the ointment. As more than one analyst has noted, we could be in for an inflation surprise when PCE comes in. Independent analyst Sahm and the FT both home in on the problem of shelter, the primary driver in CPI. As they both note, core PCE ex-housing is running at 2.1%. This is close enough to the target for government work. See below.

Tidbit: In raw politics, the latest is Pres Biden telling Pennsylvania steelworkers he is calling for a tripling of tariffs on Chinese steel and aluminum (from 7.5% now). The Trade Rep is also looking into unfair practices in Chinese shipbuilding, an inquiry initiated by the steelworkers union. The FT notes that imported Chinese steel is 0.6% of total US steel demand, so there would be almost no effect on inflation.

Separately, yesterday’s Chinese data showed industrial production up 6.1% and manufacturing up almost 10% in Q1, with export also up 14%.

TreasSec Yellen visited China and warned against overcapacity in EVs, batteries, solar panels and other goods that are flooding the global market and will flood even more. “Nothing is off the table” in terms of the US response. Then German Chancellor Scholz—the Chancellor! —visited China with the same message, naming the €250 billion trade deficit favoring China. The Chinese response from Pres Xi was to point out that the Chinese output was taming inflation and contributing to environmental protection. In other words, no.

The FT today emphasizes that the Chinese rejection of Western complaints is falling on deaf ears. “After welcoming German Chancellor Olaf Scholz outside the Great Hall of the People in Beijing on Tuesday, China’s second-ranked official Li Qiang gave his guest a lecture on basic economics…. Moderate production exceeding demand is conducive to full competition and survival of the fittest.”

One fly in the ointment is Chinese subsidies to these exporters as well as to competitors of European medical equipment, according to the Bloomberg story. It’s not he bottom line, but might as well be: “What’s becoming clearer, though, is the European Union and China risk slow-walking into a trade war as Beijing resists requests to open up its economy, triggering the bloc’s deployment of its defense measures.”

The week before, Bloomberg reported “The French government will amend regulations and provide subsidies to support the installation of domestically-made solar panels, key for its energy transition, to reduce the dominance of Chinese equipment manufacturers.”

Tidbit: There’s nothing sadder than a closed mind. CNN ran an interview with a Texas Panhandle rancher couple. They each said Trump is not fit for the office of president because of moral, ethical and legal reasons. They think he is guilty in the current trial. But they are going to vote for him anyway, because they hate the Dems/Biden to the bone.

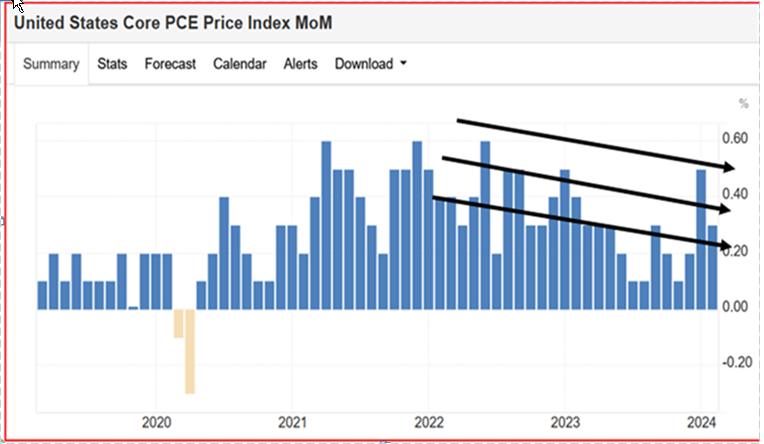

Tidbit: To add to last week’s chart of the core PCE with our trend arrows, see the second chart below. We remain impressed with the observation from Reuters that the CPI in the month/month was 0.359%, then rounded up to 0.4%, when 0.3% had been forecast. “The rounded print would have been in line with expectations had the number come in less than one basis point lower.”

Nobody knows whether the next bump in PCE inflation will be to the upside or downside. It would take a decent drop in core PCE to restore some of the expectation of rate cuts. If a drop, given the current hysterical mood, the yields and dollar are at risk.

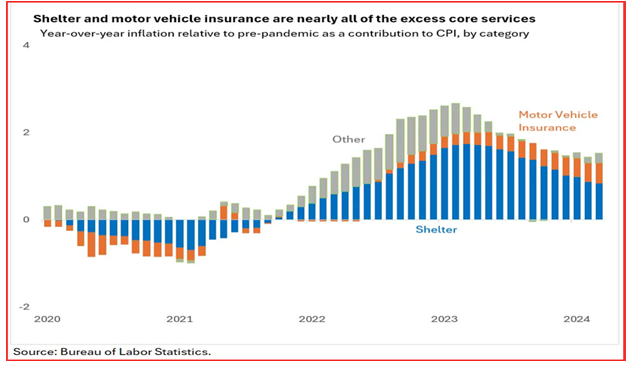

We have some hope that the next PCE print might be better. Remember, PCE tends to be about 0.5% lower than CPI. As Sahm writes, “The good news about elevated services inflation is that a much narrower set of categories are the big contributors to the current CPI inflation and even the pickup this year.

… “Within core services, excess inflation contributions to CPI are down to a handful of categories. With the year-over-year inflation, the two big contributors are shelter and motor vehicle insurance. The latter's weight in CPI is under 3%, underscoring how massive the price increases for motor vehicle insurance have been.”

Take a hard look at the chart. If shelter is the biggie and in practice, only a fraction of the population actually changes residence in any period, we could get a good print next time. In other words, all hope is not lost.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat