Market insight for the week ending 24 March

Weekly review

It has been a volatile week across the financial markets.

Unless you have been hiding under a rock, you will recall that two US banking institutions recently collapsed: Silicon Valley Bank and Signature Bank, which sparked contagion fears. Also in the spotlight last week was Credit Suisse, falling to its knees and clocking record lows. However, the banking giant has avoided total collapse thanks to the Swiss National Bank’s (SNB) backing, offering liquidity of up to US$54 billion.

This led banking stocks and broader equity indexes largely lower last week. Energy stocks fell nearly 7.0%, followed by financials, down by around 6.0%. European equity indices posted heavy losses across the board; the FTSE 100 shed an eye-watering 5.3%, with the DAX, the CAC and the Euro Stoxx 50 trailing not too far behind, erasing 4.3%, 4.1% and 3.9%, respectively.

We also saw a classic flight to safe-haven assets. The US dollar, as measured by the US Dollar Index, gained strongly on Wednesday, adding 1.0% against currency peers, and US government bonds as well as the price of gold (XAU/USD) caught a strong bid. Note that the biggest falls were seen in yields across short-dated US Treasury rates, sparking concerns about growth; the 2-year US yield dropped 44 basis points to 3.504% while the benchmark 10-year yield plunged nearly 30 basis points. Gold is nearing $2,000 per troy ounce, following Friday’s spirited 3.6% rally (WTD, the yellow metal added 6.5%).

It would be remiss not to direct the limelight to the cryptocurrency space, as major cryptocurrencies aggressively navigated higher terrain in recent trading. BTC/USD printed its largest one-week gain this year, adding more than 20.0%.

In the macro space, the European Central Bank (ECB) remained on course and delivered a 50 basis-point increase, despite markets pricing in the chance of a smaller rate hike considering the banking sector concerns. Market participants also welcomed the latest US inflation data. In the twelve months to February, inflation cooled to 6.0%, marking an eighth consecutive decline since peaking in June 2022. According to the University of Michigan (UoM) preliminary survey, consumer sentiment also sunk for the first time in four months despite expectations for inflation showing improvement. Consumer sentiment fell to 63.4 in March from 67.0 in February, and inflation expectations for the year ahead fell from 4.1% to 3.8%.

Markets this week

This week’s biggest driver for the financial markets is the central banks and how they will respond to the latest events. Of note, we have three major central bank announcements to monitor: the US Federal Reserve (Fed), the Swiss National Bank (SNB) and the Bank of England (BoE). The big question is whether the central banks press ahead with rate hikes. According to STIR markets, all three banks are expected to hike rates this week, with the US and the UK poised to increase rates by 25 basis points and the SNB by 50 basis points.

Additional risk events to monitor this week:

Tuesday 21 March

Reserve Bank of Australia (RBA) Meeting Minutes at 12:30 am GMT

Following the RBA hiking rates by 25 basis points, the RBA’s Meeting Minutes will offer investors a comprehensive analysis of the most recent meeting.

Tuesday 21 March

Annual Headline Inflation Rate for Canada for February at 12:30 pm GMT

Since June’s 8.1% peak (2022), we have seen a gradual slowdown in consumer prices, with Canada’s annual inflation rate falling to 5.9% in January 2023. The median consensus forecasts a fourth consecutive decline to 5.2%.

Wednesday 22 March

Annual Headline Inflation Rate for the UK for February at 7:00 am GMT

The consensus heading into the event calls for a fourth consecutive easing of consumer prices to 9.6% in the 12 months to February, following January’s 10.1% rate.

Friday 24 March

Eurozone, UK and US S&P Global (Flash) Manufacturing and Services PMIs for March at 9:00 am, 9:30 am and 1:45 pm GMT, respectively

Expectations for the respective Manufacturing events are 49.0 (Previous: 48.5), 48.3 (Previous: 49.3) and 47.0 (Previous: 47.3).

Currencies

Dollar Index prints weekly drop; further selling is likely according to charts

Week to date, the US dollar shed 0.7% according to the US Dollar Index. Month to date, however, the index has fallen 1.0%, on track to claw back a portion of February’s 2.8% gain.

Longer term, Q4 of 2022 saw price action on the monthly timeframe reject an ascending channel resistance taken from the high of 103.82. The key observation is that the dollar remains depressed and technical expectations call for further selling towards Quasimodo resistance-turned-support from 99.67. In the context of the Relative Strength Index (RSI), the indicator is still on the doorstep of its 50.00 centreline, which happens to be shadowed by an indicator trendline resistance-turned-support pencilled in from the high 82.87.

Technical elements on the daily timeframe show Wednesday’s 1.0% advance came within striking distance of clipping the lower base of a thin decision point from 105.35-105.15 before pulling back and throwing light on familiar support between 103.34 and 103.44 (comprises a 50.0% retracement ratio and a 78.6% Fibonacci retracement ratio, and the 50-day simple moving average). Outside these immediate structures, technical interest is directed to demand at 100.27-100.77 and resistance marked from 105.82.

In light of recent price movement, and room to push lower on the monthly chart, daily support between 103.34 and 103.44 is perhaps vulnerable this week. A breakout south of here could trigger a bearish assault in the direction of daily demand at 100.27-100.77. That said, though, a test of the daily decision point at 105.35-105.15 is not out of the question, a move that would likely be welcomed by sellers who adopt a multi-timeframe approach.

Source: TradingView

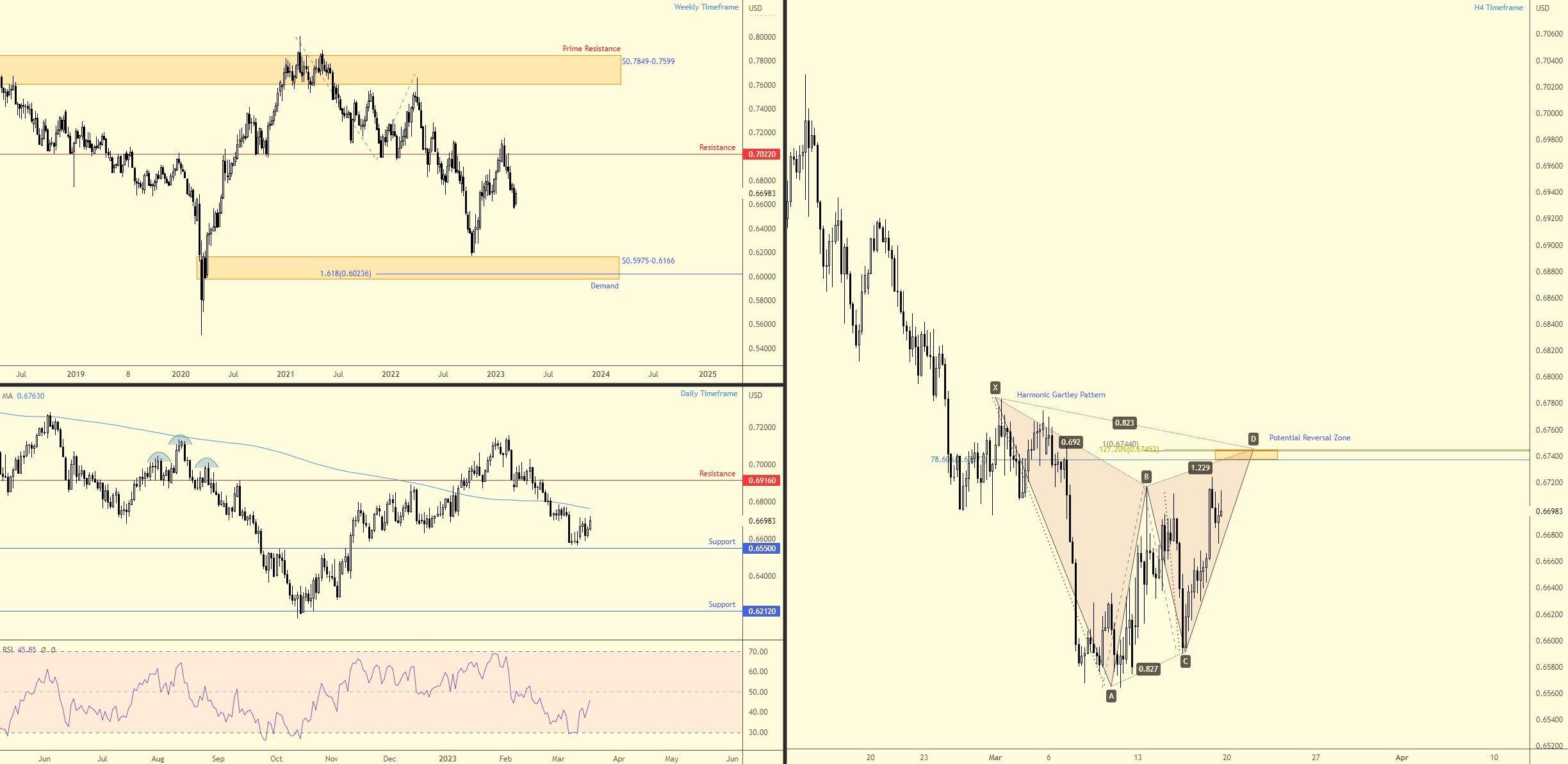

AUD/USD eyeing underside of 200-day simple moving average?

The Australian dollar ended last week on the front foot against its US counterpart, gaining 1.8% and shaping what is referred to as a bullish harami candlestick formation on the weekly timeframe. Preceding the higher high formed at $0.7158 in early February (movement that probed resistance at $0.7022), some will likely view the candlestick pattern as a medium-term buy signal. Of course, the concern with this candlestick structure is the lack of support on the weekly scale, and the overall trend has been south since February 2021, despite the moderate higher high in February.

Against the backdrop of the weekly timeframe, the technical view on the daily chart is drawn to the underside of the 200-day simple moving average, currently fluctuating around $0.6763. Note that should the aforementioned moving average welcome price this week, the Relative Strength Index (RSI) will also likely visit the lower side of its 50.00 centreline, which can form indicator resistance. Below the current price, attention shifts to support from $0.6550, while north of the moving average, resistance calls for attention at $0.6916 (a base boasting strong historical significance since July 2022).

The key technical observation, however, is found on the H4 scale, representing a harmonic Gartley bearish pattern with a Potential Reversal Zone (PRZ) between $0.6745 and $0.6737. Harmonic traders tend to short the PRZ and position their protective stop-loss orders beyond the X-point: 1 March high at $0.6784. Knowing this and understanding that the space between the X-point and the upper edge of the PRZ houses the 200-day simple moving average, along with the overall trend still pointing south (weekly chart), sellers could make a show between $0.6784 and $0.6737 this week if tested.

Source: TradingView

Commodities

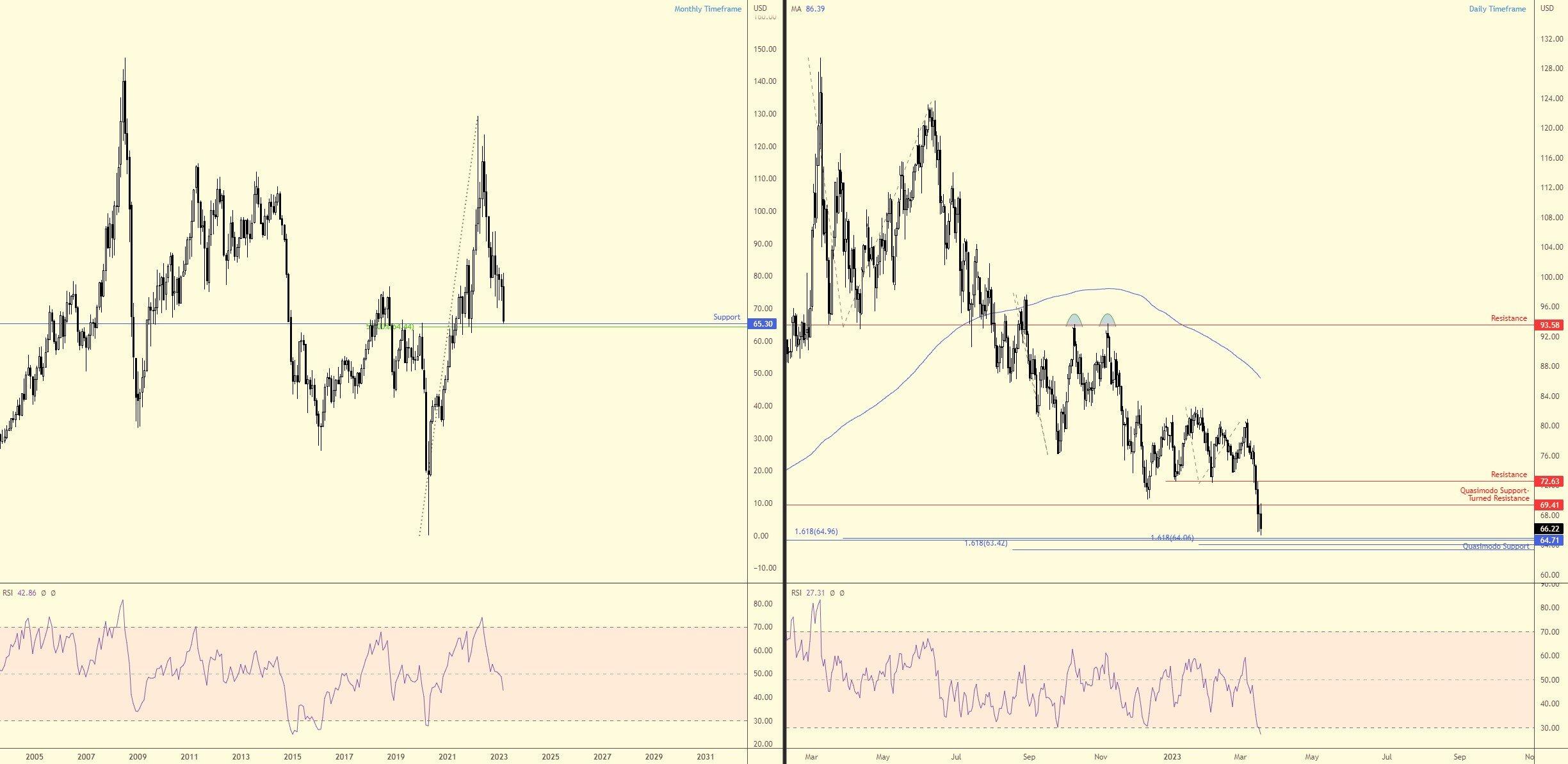

Oil dives to 15-month lows; worst week of the year

The price of oil (West Texas Intermediate [WTI]) nosedived last week, touching $66.22 per barrel. Down 13.6%, the sell-off began earlier in the week following the collapse of Silicon Valley Bank last Friday.

While sellers concluded the week in the driving seat, support on the monthly timeframe from $65.30 may offer some technical respite this week, a level closely accompanied by a 50.0% retracement ratio at $64.44. Despite the unit largely offering a one-way market since spiking to a high of $129.42 in March 2022, current support is KEY technical structure and worthy of the watchlist.

On the daily timeframe, the week finished with price retesting the lower base of a Quasimodo support-turned-resistance level from $69.41. Interestingly, there is scope to modestly refresh lows on the daily chart, targeting Quasimodo support at $67.41 (joined by a collection of 1.618% Fibonacci ratios between $63.42 and $64.96 [projections and expansions]). Another key technical observation is the Relative Strength Index (RSI) dipping a toe in oversold waters (30.00) last week. So, despite the monthly RSI crossing 50.00 (negative momentum), buyers could make a show in the short to medium term.

Given the current technical surroundings, the daily support zone between $63.42 and $64.96 will likely be of (bullish) interest this week, complemented by the heavyweight monthly support level of $65.30.

Source: TradingView

Bonds

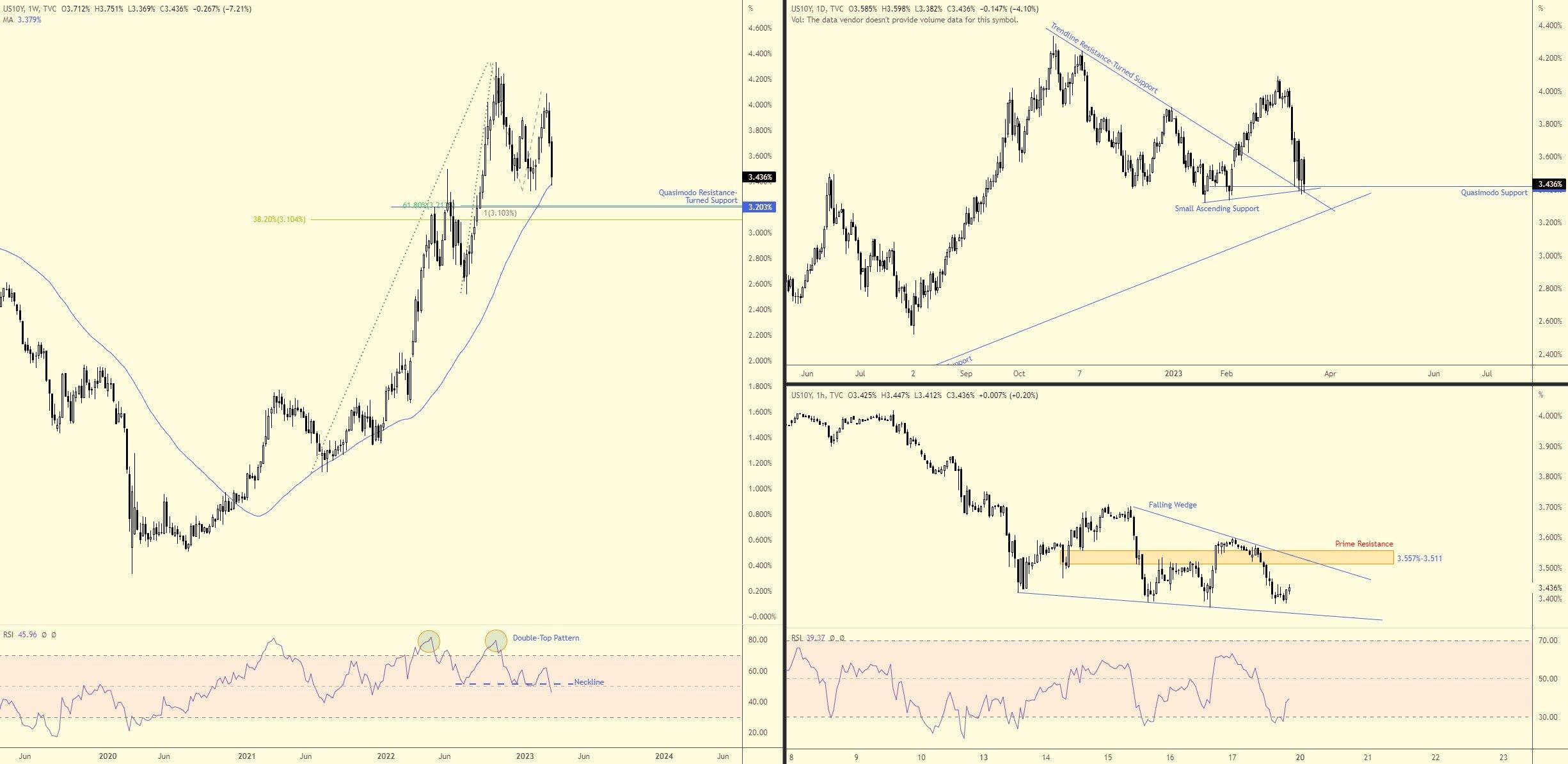

US 10-year treasury yield records steep back-to-back weekly losses

Kicking things off with the weekly chart and a chart it IS. Down 28 basis points on the week, price action welcomed the 50-week simple moving average at 3.379%. While traders/investors may view this as a possible (dynamic) floor this week, the Relative Strength Index (RSI) navigated south of its 50.00 centreline, informing market participants that average losses exceed average gains: negative momentum. Complementing this bearish vibe is also the RSI pushing through the neckline (51.34) of a double-top pattern (81.58). This indicates further downside to RSI oversold territory as well as price support from 3.203% (which is complemented by a 61.8% Fibonacci retracement ratio at 3.213%, a 100% projection at 3.103% and a 38.2% Fibonacci retracement ratio from 3.104%).

The technical landscape out of the daily timeframe currently supports a bullish atmosphere. Following the higher high at 4.089% in early March, the price corrected and greeted an area of support (confluence) which is made up of Quasimodo support from 3.420%, a trendline resistance-turned support taken from the high of 4.244% and a small local ascending support line drawn from the low of 3.321%. Should the aforementioned area cede ground, attention will shift to a longer-term trendline support taken from the low of 1.355%.

Navigating price action through the H1 timeframe shows that downside momentum has recently decreased. We can see this through the RSI visiting oversold space and the falling wedge price pattern between 3.418% and 3.703%. Nevertheless, prime resistance deserves attention at 3.557%-3.511 and might concern short-term buyers.

From the three timeframes analysed, technical studies suggest that the benchmark 10-year US Treasury yield could rebound higher this week and recoup some of its recent downside. This is evidenced through the weekly timeframe testing its 50-week moving average, the daily timeframe shaking hands with a collection of support structures and a decrease in downside momentum on the H1 scale. However, conservative traders may adopt a wait-and-see approach as the H1 prime resistance at 3.557%-3.511, and the upper edge of the H1 falling wedge might prove troublesome. Therefore, a close north of the aforesaid structures could be sufficient to prompt a flood of breakout interest in this market.

Source: TradingView

Cryptocurrencies

Bitcoin powers to fresh YTD tops

Week to date, BTC/USD printed its largest one-week gain this year, adding more than 20.0%. Following a clear-cut Japanese hammer candlestick pattern the prior week, bulls went on the offensive last week and finally tested the pattern profit objective ($26,774) derived from a falling wedge pattern on the weekly timeframe between $17,567 and $25,214. Assuming buyers remain in control this week, weekly resistance remains a potential technical headwind from $28,844. Adding to the bullish picture, we can see that the Relative Strength Index (RSI) has further cemented its position north of the 50.00 centreline and is bound for overbought territory (therefore, this is a market demonstrating positive momentum until the 70.00 threshold is reached).

Thursday retesting a Quasimodo resistance-turned-support from $24,262 saw the major crypto launch higher on Friday, claiming the bulk of the weekly gain at nearly 10.0%. Ultimately, the picture on the daily timeframe is similar to the weekly: scope to push higher until we connect with a Quasimodo support-turned-resistance from $28,651.

From the H1, charting is largely concerned with psychological levels; immediate awareness is drawn to the $28,000 and $27,000 areas. Above $28k, breakout traders will likely hone in on weekly and daily resistances at $28,844 and $28,651, respectively, while dipping sub $27k this week opens the door for bearish breakout plays to $26,000 on the H1, with subsequent bearish focus below here likely to aim for $25,000 and a support zone between $24,680 and $24,864 (consists of 38.2% and 78.6% Fibonacci retracement ratios as well as a 50.0% retracement ratio). Notably, it is important to recognise that any bearish scenario this week will be against the tide: the current trend in this market is higher, evident on both the weekly and daily timeframes.

Source: TradingView

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,