March central bank overview

Major central bank rundown

The central banks are listed below with their current state of play. The link for each central bank is included in the title of the bank and the next scheduled meeting is in the title too.

Reserve bank of Australia, Governor Phillip Lowe, 0.10%, meets 06 April

Holding the line

There were no surprises at the last RBA rate decision earlier this month. The Cash Rate and the 3-year yield target were both kept at 0.10%. The level of bond purchases was unchanged too and stays at $100 billion AUD. The RBA also recognised that the domestic economy was recovering more quickly than expected and most firms had begun loan repayments now. The RBA’s did outline their near term focus before considering raising rates. Firstly, they want to see gains in employment and a return to a tight labour market. Secondly, inflation needs to be in the 2-3% target range. Crucially, this is not expected to occur until 2024.

Economic forecasts

The unemployment level is projected to stay around 6% for 2021 and down to 5.5% at the end of 2022. CPI inflation is expected to rise temporarily due to some short term factors and GDP is anticipated to grow by 3.5% over 2021 & 2022. The RBA can say that rates won’t rise until 2024. However, if the market questions the credibility of the RBA expect strong AUD gains pricing in a rate hike. Remember the RBA will not want to be perceived to move ahead of the Federal Reserve. The RBA brought forward bond purchases in response to the rapidly rising bond yields. The RBA was prepared to do so again if necessary. So, similar to the ECB (see below), the pace of bond purchases can be accelerated to match rising yields. All in all no surprises and the AUD should remain supported on deeper dips against the CHF and the JPY. No change expected from the RBA at the next meeting though recent Australian data has been encouraging, especially employment.

European central bank, President Christine Lagarde, -0.50%, meets April 22

Pressured by slow vaccine roll-out

At their last meeting this month the ECB kept interest rates unchanged as expected. They also kept the size of the bond purchases (PEPP) unchanged at €1.85 trillion. However, like the RBA, they expect the pace of the bond purchases to be at a faster rate during the first months of the year. The ECB agreed on a monthly PEPP purchase target lower than 100 billion euros, but higher than the 60 billion seen in February. A sources piece after the ECB decision stated that there were different opinions over whether the recent rise in yields needs to be unwound. Remember that by speeding up bond purchase that keeps the yield lower. So, the ECB is divided the same way the market is divided. Is the rise in yields a sign of an economic recovery or a threat to the economic recovery? The pick up in the speed of bond purchases is seen as enough to halt any disorderly action in the bond market for now. For 2021 inflation was upgraded to 1.5% from 1.0%, but longer-term inflation kept at 1.4% for 2023. So, a short term and temporary inflationary move higher is expected similar to what the RBA expect.

The ECB’s actions were not particularly surprising. However, if the bond purchases accelerate to 100bln and, this is the crucial part, remain accelerated then that should have a more negative impact on the EUR. There is around €1 trillion of the €1.85 PEPP package still to purchase, so the ECB has plenty of room to speed up (or slow down) bond purchases. The slowing down of PEPP purchases is also an option which Lagarde reminded the market of, so two-way risks here. However with Germany recently extending their lockdown and the vaccine rollout dragging for Europe that would favour EURUSD sellers, especially with the FED being pretty indifferent to rising US10 year yields.

Bank of Canada, Governor Tiff Macklem, 0.25%, meets April 21

Optimistic, but cautious over low paid employment

Interest rates were unchanged on March 10 at 0.25% and bond purchases are to continue at the pace of $4billion per week. However, the Bank of Canada still doesn’t want to bring rate hikes for-ward and the Governing Council expects that economic slack will not be absorbed until 2023. The economy is currently 1% higher than the BoC had anticipated and in terms of tone one of the most optimistic central banks. The BoC expect inflation to move above 2% towards 3% temporarily over the coming months. This inflation is expected to be driven by the prices of numerous goods and services that fell sharply during the pandemic and rising oil prices. Another central bank seeing inflation higher, at least temporarily.

One of the major concerns of the BoC rate meeting was over job losses. These are concentrated among low age workers, young people and women. This theme was picked upon by Deputy Gover-nor Schembri the day after the rate meeting who said that the labour market remains a long way from a full recovery.

The housing market has seen strength in Canada. This is due to low-interest rates encouraging house purchases. People are also seeking more space in lockdowns. GDP grew by +9.6% in Q4 2020 led by strong inventory accumulation. GDP growth in Q1 2021 is now expected to be positive.

Personal savings are up, like much of the developed world. However, the BoC are unsure exactly how these savings will be spent in the future. There is obviously a more cautious tone around, so people will be slower to spend savings. The things most people seem to be doing with their savings now in Canada according to the BoC is: putting it in the bank as deposits (personal deposits up by $150 billion), paying off debt, buying houses (fuelling the strong housing market), and buying financial assets and retirement plans. What happens with the excess savings is important as it is enough to impact the direction of the Canadian economy. So this is why the BoC asked respondents what people would do with their savings. 5% plan to spend it all in 2021 and 14% plan on spending some. This survey was conducted in November. The BoC is working on a boost per capita to consumption of $500, but if the outlook around COVID-19 rapidly improves then more of those savings will come on line. You would expect people to be more cautious in November than now.

The BoC are optimistic, but recognise risks. Oil prices are supportive and the economy is not expected to shrink now for Q1. For now, expect CAD buyers on dips. Note the strong employment data on March 12 as Canadian employers get going again. Also, notice how there was a good pick up in jobs amongst the BoC’s target group of low wage workers. This will have reassured the BoC. The next move from the BoC will be mentioning the tapering of bond purchases. This in fact happened shortly after typing that last sentence and the BoC announced the discontinuation of market functioning programs for COVID on Tuesday. This opens up the path for bond tapering. As long as there are no further negative surprises, and if oil stays broadly supported CAD strength against the EUR would be worth considering.

Remember that stronger oil supports the CAD as around 17% of all Canadian exports are oil-related. There is a negative correlation between USD/CAD and oil has broken down recently. Canada’s top export is Crude Petroleum at over $66 billion and around 15.5% of Canada’s total exports.

Federal Reserve, chair: Jerome Powell, 0.125%. meets April 28

Federal Reserve holds to the script of ‘no rate rises until 2024’

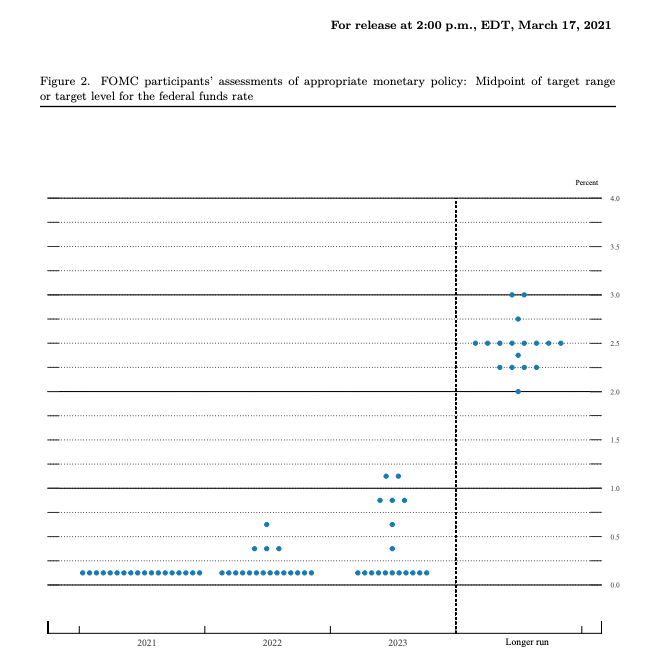

The rate was unchanged 0.25% and QE was unchanged at $120 billion per month. The headline was that the median dot plot saw ‘no interest rate rises until 2024’. However, the dot plot changed slightly with more board members now seeing sooner interest rate rises. Although the continued rise higher in yields post FOMC is showing the market is focused on sooner than expected rate hikes for now.

However, the Fed does see improved growth prospects. Some upward projections for growth and inflation and reductions in unemployment expected. The main message from Powell was that ‘the very worst economic outcomes had been avoided’. GDP for 2021 was revised higher to 6.5% from 4.2%. Unemployment for 2021 was revised lower to 4.5% from 5.0% and Inflation revised up to 2.4% from 1.8% (to reflect expectations of transitory inflation like the RBA, the BOC and the ECB).

In summary, the Federal Reserve stuck to the dovish script. Still, no rates expected until 2024. That’s what the Fed think. However, the market was not so convinced. Eurodollar futures see a rate hike on March 2023 and three rate hikes for that year. See Justin’s post here the morning after the FOMC. So the question is, ‘has the market misunderstood how dovish the Fed is going to be?’. Or has the ‘Fed got behind the market?’. All in all the shift in the dot plot tells you that if economic conditions continue to improve then the Fed will raise rates sooner than 2024. This has resulted in some USD strength post the FOMC and subject to any new developments it is reasonable to expect some USD strength into the next meeting from here. The USD strength this week was mainly on risk-off flows, so that was why the US was rising despite the US 10 year yields falling

Bank of England, Governor Andrew Bailey, 0.10%, meets May 06

Prior to the latest BoE meeting on March 18, there was a tail risk of a rate hike coming into the markets. The GBP has been strongly supported over the last few weeks and the last meeting continues to provide a reason for optimism regarding GBP strength. The major headlines for the Bank Of Eng-land struck me as pretty neutral. However, the minutes and the statement in full read pretty upbeat. At the last Bank of England meeting, the Monetary Policy Committee (MPC) voted unanimously to keep interest rates at 0.10% and bond purchases were unchanged at £20 billion per month as expected. There had been thoughts prior to the meeting that perhaps the BoE would be more positive as the UK’s vaccination program is coming along well. Over half of the UK adult population has now received at least one dose. Furthermore, the latest US phase III AstraZeneca trial shows that the vaccine has a 100% efficacy in preventing severe disease. As the BoE looked overseas there was a generally upbeat tone. Global GDP growth is stronger than expected. The BoE expected that the US fiscal stimulus package should provide further global support. The BoE report had considered only around a $1 trillion package according to their minutes. (confusingly labelled page 2, but is actually page 5 of the PDF). So, this much larger than expected package was expected to boost the UK’s economy as well as the globe. There was no worry about the rising bond yields and that was just seen as a natural consequence to improved conditions (don’t tell that to the Fed). There was also a note about the cost of shipping containers rising, but that prices had some-what stabilised recently. This was all before the latest Suez crisis, so that is arguably a greater issue to world trade as shipping containers have to take a two-week long detour around the bottom of S.Africa.

Domestically the BoE were pretty upbeat too. UK GDP which fell by 2.9% was less weak than expected, but GDP Is still around 10% below its 2019 Q4 level. 2021 Q2 could see ‘slightly stronger’ consumption growth, but unsure if this will impact the medium-term forecast. (so this is being down-played). CPI expected to turn to around 2% in the Spring as the impact of lower oil prices falls away. However, the latest UK CPI reading was lower than expected. Non-essential retail and outdoor hospitality to open no earlier than April 12 and entertainment and non-self-contained accommodation no earlier than May 17. A Bank of England survey saw that 15% of households would be spending more after restrictions eased and 40% said they would spend less. Economist Andy Haldane sees the change of a ‘rip roaring’ UK economy with a large build-up of UK savings at around £150 billion

One area of potential concern is that the UK trade in goods volumes has fallen substantially in January. Exports and imports fell around 19% and 21% respectively. (Some disruption around the UK-EU transition period end were cited). This is one area that I don’t have a proper handle on. Yes, a no-deal Brexit has been avoided, However, EU-UK trade is being hampered and to what extent this will continue is an area I unclear on, but warrant further research. Any helpful info that you have, please leave for readers below.

The takeaway of this report is that the Bank of England has signs of hope on the horizon. If they start to materialise further then that should support the GBP against weaker currencies like the euro with present market conditions. EURGBP remains a sell on rallies higher for now.

Swiss National Bank, chair: Thomas Jordan, -0.75%, meets March 25

The SNB interest rates are the world’s lowest at-0.75% due to the highly valued Franc. As an export driven economy they hate a strong CHF and are doing their best to make it as unattractive as possible. The market generally ignores this and keeps buying CHF on risk aversion which has been here in one form or another since around 2008/2009 if the EURCHF chart is anything to go by. However, we are seeing some CHF weakness naturally creep in as the world begins to tentatively imagine a COVID-19 free world and the potential for safe haven CHF holdings to drop. A quick glance at CHF pairs we show this to be the case.

Earlier this week on March the SNB left rates unchanged. The inflation forecast was revised ever so slightly higher due to strong oil prices. The forecast for 2021 is +0.2% & +0.4% for 2022. Growth for 2021 is still seen between 2.5% -3.0%. The statement once again struck a tone of optimism vs ‘who knows what will really happen’ with upside and downside risks stated.

The SNB continue to intervene in the FX markets. The Swiss are always mindful of the EURCHF exchange rate because a strong CHF hurts the Swiss export economy. This is why the opening par-agraph, and sentence number two, reads: ‘Despite the recent weakening, the Swiss franc remains highly valued’ . The SNB want a weaker CHF. The rest of the world wants CHF as a place of safety in a crisis, so we have this constant tug of war going on.

For more details on the sight deposits check out SNBCHF.com, This site called the removal of the floor back in 2015, so well worth checking out.

The bottom line here is no real change from last meeting. However, note that a currency like CAD could offer some decent upside against CHF over the coming months as the BoC prepare to taper. The SNB are still content to be the lowest of the central bank pack and dissuade would be investors by charging them for holding CHF.

Bank of Japan, Governor Haruhiko Kuroda, -0.10%, meets March 19

The Bank of Japan met March 19. The Bank of Japan is another very bearish bank, but the latest meeting saw a small shift in their policy. The BoJ kept rates unchanged at -0.10%. The Yield Curve Control is expanding its flexible target to be +/- 25bps vs +20 bps prior, but the 10 yr JGB yield tar-get remains at 0.0%. The ETF target was removed and the BoJ is only to buy ETF’s linked with the TOPIX. This resulted in the Nikkei falling on the news, although these adjustments were not a big surprise to the markets. All in all there is not a major shift here, as the BoJ remain prepared to step in to support equity markets if needed. Kuroda said that the domestic economy remains in a severe state, but the trend is picking up.

Reserve bank of New Zealand, governor Adrian Orr, 0.25%, meets April 14

There were no major changes in the latest RBNZ meeting and Governor Orr did his part to try and talk down the NZD. The key issue for New Zealand is if their economy accelerates sharply that will benefit the NZD. Too much NZD strength hurts New Zealand exporters, so the RBNZ have an interest in trying to discourage NZD strength. However, the reality is that the market looked through the dovishness from the meeting as expected. Interest rates were kept unchanged at 0.25% as expected. Annual CPI now seen at 1.5% and TWI at 74.9% vs 71.5% expected. No additional stimulus required, but current monetary policy as-sumed to be staying at the same level for a ‘prolonged period’. Large Scale Asset Purchases (LSAP) were kept the same at $100 billion.

The RBNZ statement recognised the uptick in activity both globally and within New Zea-land. However, the statement acknowledged the problem with the strength of the NZD. This was always going to be the RBNZ’s challenge with this meeting. How do you recognise a strengthening economy without rapidly strengthening the NZD. Well, it is done by stressing the uncertainties that are ahead. So, it is unsurprising that the RBNZ said that the economic outlook was still considered uncertain by the RBNZ.

One of the helpful developments for the RBNZ was the police shift that took away from the RBNZ the mandate to keep house prices from rising too quickly. Earlier in the year this had been made their mandate and supported NZD higher as markets knew the RBNZ would be pressured to raise interest rates. That pressure went with the Gov’t announcement a few days ago that aims to contain the rising house prices. This dragged the NZD lower as a key pressure was now removed from the RBNZ and the dovish leaning can now be more easily enjoyed. House prices around the world have been supported by low mortgage rates, so this may be a pattern that other Govt’s follow.

Author

Giles Coghlan LLB, Lth, MA

Financial Source

Giles is the chief market analyst for Financial Source. His goal is to help you find simple, high-conviction fundamental trade opportunities. He has regular media presentations being featured in National and International Press.