Learning from history: Why stocks may be about to correct

An interesting Bloomberg piece has come out recently showing the relationship between rising commodity prices and stock market corrections. Here are the details:

-

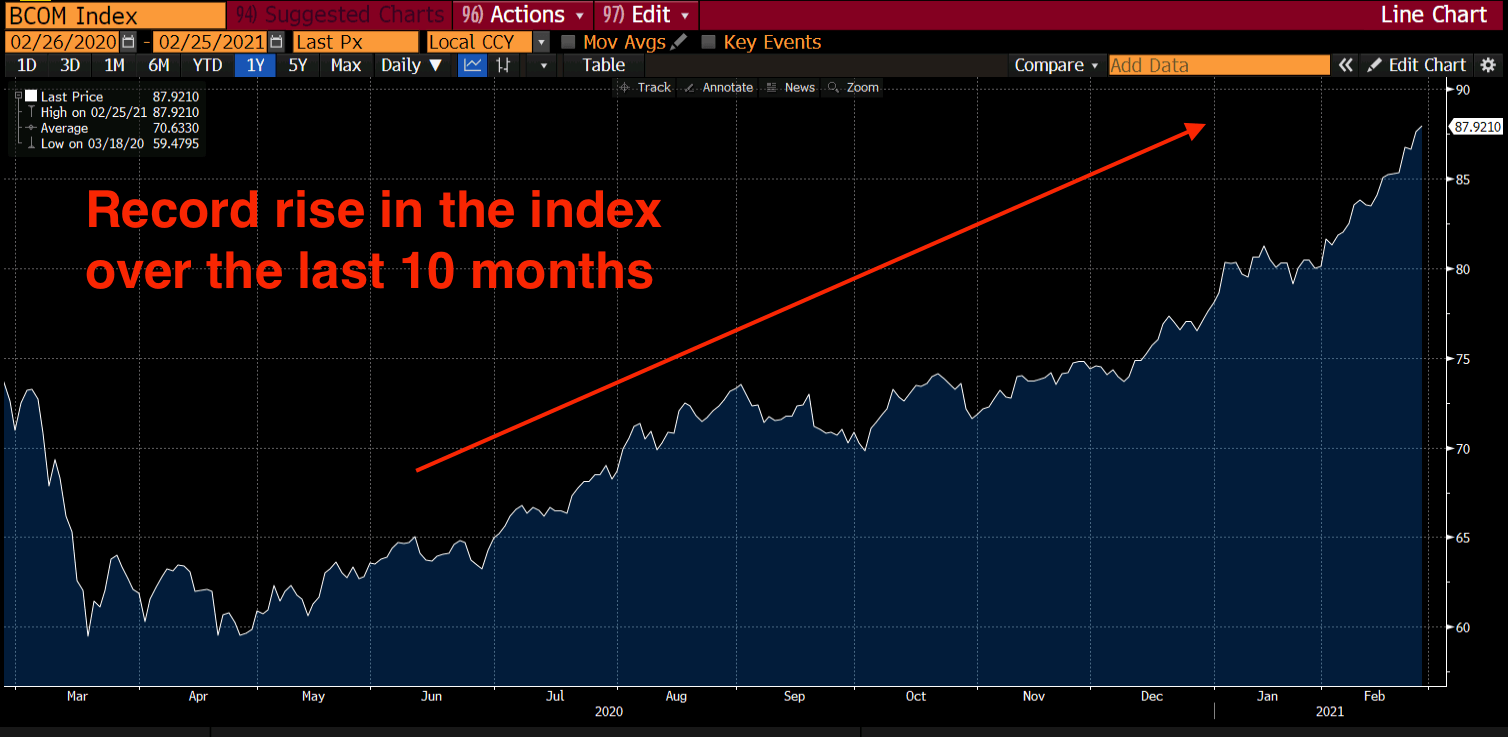

The Bloomberg commodity index has risen 60% since April 2020.

-

At present this current period of commodity growth has been the fastest climb in more than 40 years. It is the 8th largest growth period since the Bloomberg Commodity Spot Index records began more than 60 years ago.

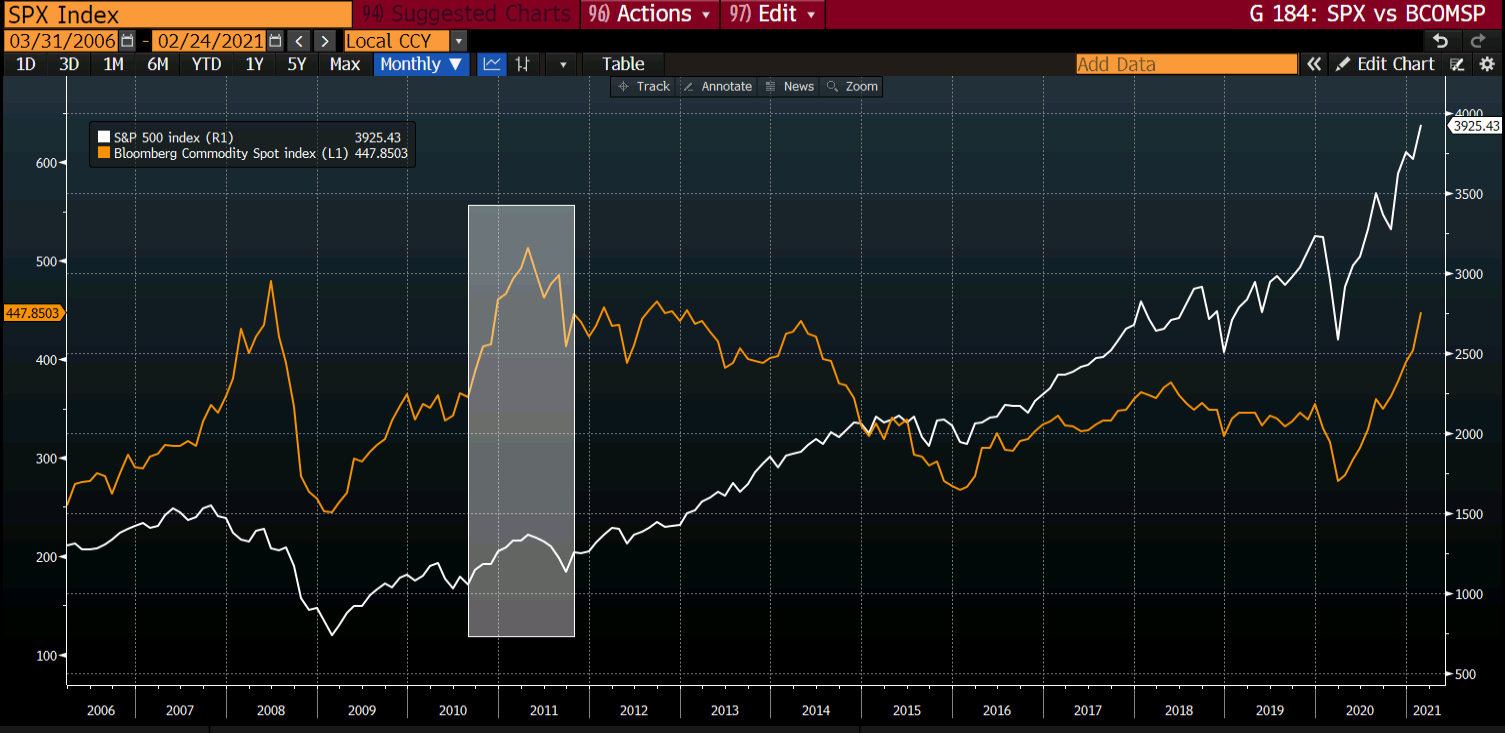

Note the following: In the top 10 months following record rises in commodity prices there tends to be a fall in the S&P500.

The record months are distributed as follows

-

6 months are from 1973.

-

2 months are from 1980.

-

The other months are from January 1974 and June 2008.

Taking these top 10 periods here is the average S&P500 performance after these strong rallies in commodities.

-

1-month afterwards: -1.1% loss (9 out of 10 falls).

-

3-month afterwards: -3.8% loss (7 out of 10 negative).

-

6-month afterwards: -7.9% loss (7 out of 10 negative).

-

12-months afterwards: -11.4% (8 out of 10 negative).

So, stock market bulls be warned. This is yet another signal that we could be close to a deeper stock market correction. Time to keep the powder dry? Certainly, it pays to keep a very close eye on developments. If commodities start dipping then expect the S&P500 to dip too.

Author

Giles Coghlan LLB, Lth, MA

Financial Source

Giles is the chief market analyst for Financial Source. His goal is to help you find simple, high-conviction fundamental trade opportunities. He has regular media presentations being featured in National and International Press.