Lacklustre UK growth a fresh headache for the Treasury

Fourth-quarter UK GDP wasn't as bad as it could have been, though the details weren't great. The combination of weaker growth and higher market rates has likely eroded the already-limited fiscal 'headroom' granted to Chancellor Rachel Reeves. Tweaks to future spending plans look likely in March.

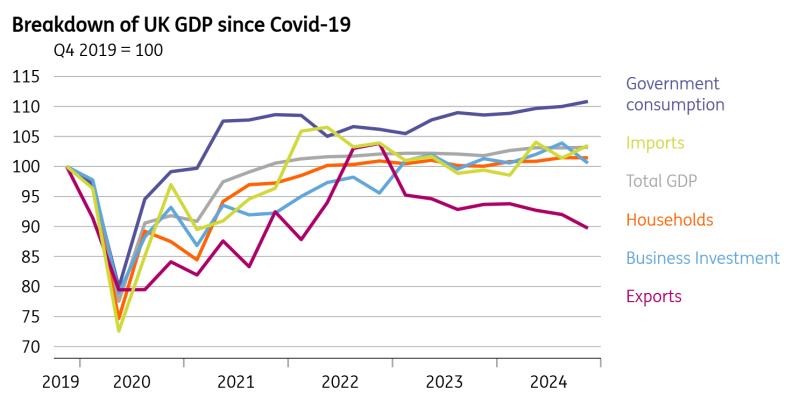

The UK economy grew by 0.1% in the final quarter of 2024, though only because of a surge in inventories. These are a notoriously volatile accounting fixture which, unlike other parts of the GDP breakdown, don't tell us much about the underlying health of the economy. The areas that do – household consumption, exports, and business investment – were all flat or negative. The latter was a particular disappointment, falling by more than 3% in Q4, having outperformed many other economies earlier in the year.

It's not all bad. December's monthly figures were better, helped by certain consumer-facing services. And 2024 as a whole was a reasonable year for the UK economy, even if virtually all of that previous strength was concentrated in just a couple of months. Even more remarkably, all of the increase in GDP across 2024 can be put down to population growth. GDP per capita actually fell slightly across the year.

2025 promises to be reasonable too, thanks to a substantial injection of government spending, which will only be partially offset by higher taxes. The jobs market is the major downside risk, but barring a spike in layoffs, real wage growth is also set to remain positive, despite rising household energy bills. That should support some modest consumption growth.

Business investment fell having performed better earlier in 2024

Source: Macrobond

Nevertheless, the lacklustre end to 2024 will only cement the loss of fiscal headroom the Treasury must now grapple with. The Office for Budget Responsibility – the government’s independent forecaster – has predicted 2% growth this year. It now looks likely it will be around half that.

The OBR will unveil new forecasts to coincide with the Spring Statement on 26 March. Lower growth forecasts will chip away at revenue predictions, while higher market rates mean debt interest forecasts will rise too.

All of this suggests the Chancellor's 'headroom' has likely been completely eroded. This headroom, which refers to the surplus funds remaining after meeting the primary fiscal rule of balancing the current budget later this decade, was just £10bn as of October.

While that's undoubtedly unwelcome news for the Treasury, let's not get too dramatic about it. The forecast changes we're likely to see in March won't be huge, and the fact that the headroom has vanished is simply because there wasn't much of it in the first place.

What's more, it shouldn't be that difficult for the Treasury to get that headroom back. Remember the key is not what the fiscal picture looks like today, but where it is projected to be in five years’ time. Small tweaks to future spending plans would probably be sufficient to get the numbers out of the red.

The million-pound question, though, is whether markets buy that. Successive chancellors have embraced the implicit flexibility that these forward-looking fiscal rules grant them. And generally, markets are unfazed. But January's gilt sell-off demonstrated that investors are more sensitive to the UK's fiscal story right now. And the risk is that they focus more on the current reality of circa 4% deficits and substantial gilt issuance plans over the government's fiscal rules.

Read the original analysis: Lacklustre UK growth a fresh headache for the Treasury

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.