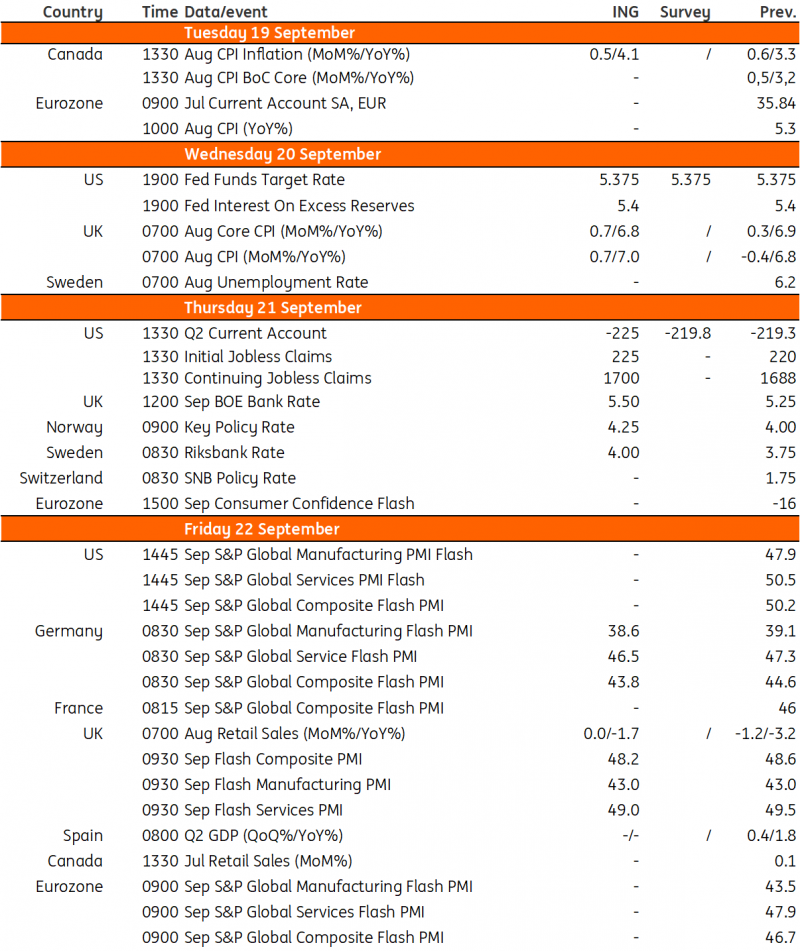

Key events in developed markets next week

We expect the US Federal Reserve to leave interest rates unchanged next week, although the door will be left open for future hikes. The Bank of England, on the other hand, is expected to hike rates, although a pause should not be ruled out. We think there'll be further rate hikes at both the Sweden and Norway central bank meetings.

US: We except to see the Fed leave interest rates on hold

The Federal Reserve has received some encouraging news on US inflation over the past few months, with two consecutive 0.2% month-on-month prints and a third coming in at 0.278%, much better than the 0.4-0.5%MoM consecutive prints we got over the prior six months. There has also been good news on moderating labour costs (the Employment Cost index and cooling average hourly earning growth) and more modest job creation. Yet activity data continues to run hot and the Fed doesn’t want to take on any chances that inflation lingers. So while we expect to see the Fed leave interest rates on hold next week, the door will be left open for a potential future hike. Economists are universally expecting the Fed funds target rate range to be left at 5.25-5.5% on 20 September, with markets not pricing even 1bp of potential tightening.

In terms of its forecasts, the key change in June was the inclusion of an extra rate hike for this year, leaving the Fed funds range at 5.5-5.75%. It seems highly doubtful this will be changed given the data flow, while the unemployment and inflation numbers seem broadly on track. GDP for 2023 will be revised up substantially though given the remarkable resilience of activity and the consumer spending splurge over the summer, much of which appears to have gone on leisure activities.

We don't think the Fed will carry through with that final forecast hike though. The combination of higher borrowing costs and less credit availability, plus pandemic-era savings being exhausted and student loan repayments restarting, should mean that households feel more of a financial squeeze in the fourth quarter and beyond. Rising credit card and auto loan delinquencies also hint at more pain with the Federal Reserve’s Beige Book warning that we may be in "the last stage of pent-up demand for leisure travel from the pandemic era".

The concern is that economic softness could go too far (as highlighted by some officials in the July FOMC minutes) and heighten the chances of recession. Given this risk and the positive developments on inflation and labour costs, we think the Fed will be on hold for a number of months with the data flow gradually weakening the case for a November or December rate hike – which the market itself only gives around a 50:50 chance of happening. Our base case continues to be: more aggressive interest rate cuts through 2024 than suggested by the Fed and priced by financial markets.

UK: Bank of England to hike rates further, but don’t rule out a pause

Markets are once again toying with the idea of a pause from the Bank of England next week. We certainly don’t rule that out, and recent comments suggest the BoE is laying the ground for the end of this tightening cycle. The central bank might be tempted by a Fed-style “skip” this month, accompanied by strong hints that it could hike again in November.

That’s not our base case, given both wage growth and services inflation – the two key metrics upon which the BoE is basing policy – are higher than forecasted back in August. We suspect the Bank will keep its options open for November, but ultimately we think September’s meeting will mark the peak in this hiking cycle.

Sweden: Riksbank set for a further 25bp rate hike

With Swedish services inflation still uncomfortably high and the trade-weighted value of the krona back to its lows, the Riksbank is set for another hike this month and we don’t rule out another by year-end. Yet the economy is clearly reacting to higher interest rates. A 0.8% decline in second-quarter GDP, while not as bad as initially reported, shows the economy is under strain. While the Riksbank clearly isn't quite done with rate hikes, the fragile economic backdrop suggests we're near the peak.

Norway: Norges Bank set for further hike amid higher oil prices and a weaker NOK

Back in August, Norges Bank all but confirmed it intended to hike rates again this month. The question is whether this will mark the top in the cycle. That was what was implied by the most recent interest rate projection from the central bank in June. Since then oil prices have risen a fair bit, and that’s viewed as a hawkish factor in the Bank’s models.

The krone has also started to weaken again, though on a trade-weighted basis is still slightly stronger than the Bank’s forecasts had been assuming in June. Underlying inflation has also been coming down, in line with the June projections.

We suspect the bank’s new interest rate forecast, which will accompany next week’s decision, will at least flag a risk of another hike later this year. But for now, our base case is that the central bank remains on hold beyond September.

Key events in developed markets next week

Source: Refinitiv, ING

Read the original analysis: Key events in developed markets next week

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.