Japan’s Manufacturing activity firms as inflation accelerates

Inflation has accelerated, industrial production has beaten the market consensus, and labour conditions remain tight. We expect GDP to rebound in 2Q24 while the likelihood of a July rate hike by the Bank of Japan has increased.

Tokyo consumer prices rose mainly due to utility fee hikes in June

Tokyo’s consumer inflation data, a leading indicator of nationwide inflation, was largely in line with market expectations. Headline inflation rose 2.3% year-on-year in June (vs 2.2% in May, 2.3% market consensus), gradually accelerating for the third consecutive month. Core inflation excluding fresh food, a preferred measure of the Bank of Japan, also rose 2.1% in June, beating the market consensus of 2.0% (vs 1.9% in May).

Today’s data confirmed that underlying inflationary pressures remain intact. Utilities prices were the main driver of the increase, but service prices also firmly rose. On a month-on-month basis, inflation rose 0.3% MoM (seasonally-adjusted) in June (down from 0.4% in May) with both goods (0.4%) and services (0.3%) prices rising. We now expect June nationwide CPI inflation, due on 19 July, to reach 3% (vs 2.9% in May) and core CPI to rise 2.7% in June (vs 2.6% in May). A temporary programme to reduce energy bills for the summer heatwave (August to October) is being discussed, which, if passed, is likely to slow inflation. However, this wouldn’t change the BoJ’s normalisation efforts much.

Industrial production rose more than expected in May

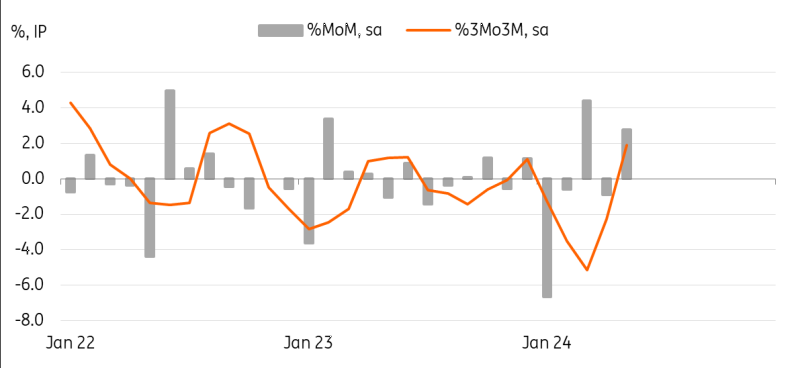

Monthly activity has been quite choppy throughout this year, mainly due to the production interruption caused by the auto safety scandal. Looking at a three-month comparison to see the underlying trend, IP rebounded to 1.9% 3M3M sa for the first time in five months.

The gradual normalisation of automobile production was the main reason for the strong increase in May but electrical/electronic machinery also grew quite firmly. Going forward, the car and semiconductor industries should be the main drivers of manufacturing output. But according to the survey of production forecast, the volatile move is expected to continue, with a decline in June but an increase in July.

Auto-led production recovery continued in May

Source: CEIC

Labour market remains tight in May

The jobless rate remained unchanged for a fourth month at 2.6% in May (vs 2.6% in April, market consensus), while the labour participation rate rose to 63.3% (vs the recent low of 62.6 in January). The job-to-application ratio edged down to 1.24 (vs 1.26 in April) as the number of applicants rose faster than the number of jobs on offer. We expect tight labour conditions to persist, together with firm wage growth, which should support household consumption in the coming months.

GDP and BoJ outlook

Today's stronger-than-expected rebound in IP and tight labour market conditions support our view that 2Q24 GDP will rebound quite smartly. The latest retail sales data showed gains in the past two months, so a positive contribution from private consumption and exports is expected. This is also in line with the BoJ's own assessment that the contraction in 1Q24 GDP should be temporary and that the economy remains on a recovery path. Meanwhile, accelerating inflation should support a BoJ rate hike as early as July. With the renewed depreciation of the yen, upside risks for inflation are increasing. If the BoJ confirms the solid wage growth in July, then the Bank is expected to raise its policy rate by 15bp at the July meeting. The market consensus is still set on an October hike, but the possibility of a July hike has risen rapidly.

We believe that quantitative tightening will not be a constraint for a July rate hike as the BoJ should acknowledge that upside risks for inflation could grow even faster if the normalisation of policy were to be postponed. Regarding QT, we think that JGB purchases are likely to be reduced from the current 6 trillion yen to 5.5 trillion yen initially and gradually to 3 trillion yen over the next two years, with the pace adjusted every six months. But there is currently no strong market consensus on the QT details.

Read the original analysis: Japan’s Manufacturing activity firms as inflation accelerates

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.