Italy: Growth is up but significant fiscal imbalances remain

The Italian economy has seen strong recovery since the end of the Covid-19 pandemic. Since 2021, its annual growth has far exceeded that recorded on average in the Eurozone, thanks to the implementation of expansionary fiscal policies, which have buoyed consumption and investment, and the gradual recovery of tourism. Since the beginning of 2023 however, economic activity has started to moderate, due to an unfavourable international environment and the gradual abolition of these fiscal measures. In addition, the latter have, by their very nature, impacted the State's public finances, placing the country under the European Commission's excessive deficit procedure (EDP) in June 2024.

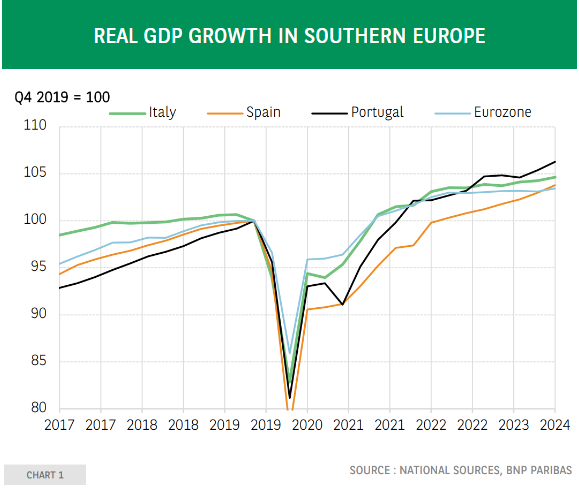

Along with the economies of Spain and Portugal, the Italian economy recovered well following the health crisis.

Between 2021 and 2023, Italian real GDP growth was quite significantly higher than that recorded in the Eurozone: in Q1 2024, Italian real GDP was 4.5% above its pre-pandemic level when that posted in the Eurozone was 3.3% above its pre-pandemic level (See chart 1).

This performance by Italy is remarkable because the country is better known for poor growth: apart from 2000, when Italian growth (4.1%) marginally exceeded growth in the Eurozone (4%), the former was one percentage point lower than the latter on average per year between 1996 and 2019.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.