Italian elections: Europe’s and the common currency’s next big test?

Italy will be heading to the polls to elect a new national government on March 4. This is widely viewed as the common currency’s – more widely the eurozone’s and Europe’s – next major risk event. The result of the elections is far from known, with a number of possible outcomes being at play and populist-perceived forces enjoying popularity. The euro is expected to come under intense selling pressure should for example the Five Start Movement find itself ruling the country; an outcome that doesn’t look that likely at the moment. However, the sell-off from such an outcome is likely to be short-term in nature, or at least this is the argument brought forward, as despite the initial uncertainty, at the end of the day there might not be much of a change in the eurozone’s third largest economy.

At the beginning of last year, the political landscape in the eurozone was rife with events posing downside risks to the euro, one of those being the French presidential elections. However, to the surprise of many, the bloc in large part moved against the “trend” that seemed to be evolving following the Brexit referendum and the US presidential election. This was seen as euro-supportive and led to a strong rally that eventually saw the common currency finishing last year 14.1% higher versus the greenback.

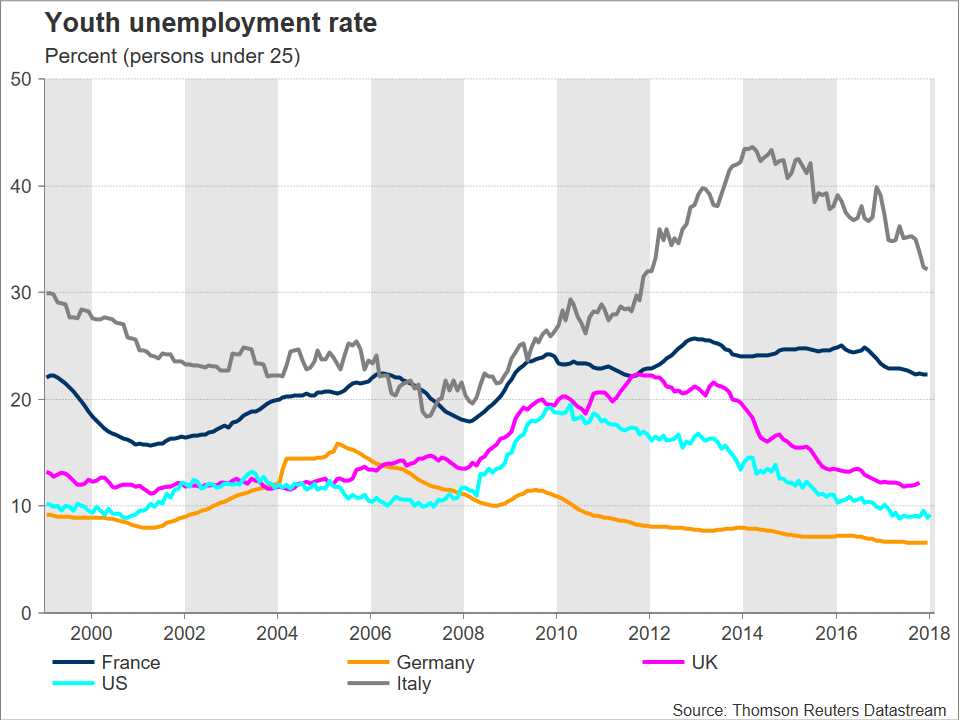

The themes of populism, immigration and social inequality that have dominated attention and led to heated debates in major elections from the recent past – among them, those mentioned previously – are making a comeback in the upcoming Italian elections. Employment opportunities are one of the hottest topics, with Italy’s unemployment rate standing at around 11%. This is one of the highest in the eurozone. The youth unemployment rate though is what is truly painting a dire picture for the country, exceeding 30%. The lack of opportunities is also contributing to “brain drain” issues, with talented youth leaving the country to make a living elsewhere, casting clouds on the outlook for growth; a similar situation is at play in Greece.

Italian election polls are showing no individual party or party coalitions securing a winning majority, and this is attributed to the country’s new electoral system, a system that was dubbed as “complicated” even by Partito Democratico (PD – Democratic Party), the very party that introduced it.

The anti-establishment Movimento 5 Stelle (M5S – Five Star Movement) is the strongest single party heading into the election, polling at around 28%. However, this is well below the 40% threshold that is required to secure a governing majority in both chambers, the parliament and the Senate. The new electoral law favors coalitions, and this comes to the detriment of M5S, whose officials have repeatedly stated that they do not intend to enter into a deal with another party as it is believed that any concessions to forge a coalition would alienate their supporters; though one might argue that in politics, statements and actions don’t always align. Other parties though have formed coalitions, with the latest polls showing them close to the 40% threshold.

Closest to that is the centre-right coalition, polling at 37%. This is made up of Berlusconi-led Forza Italia (FI – Forward Italy), Lega Nord (LN – Northern League) and Fratelli d’Italia (FdI – Brothers of Italy). It should be mentioned that if these forces take power, former prime minister Silvio Berlusconi cannot again assume the post of PM due to a 2013 tax fraud conviction – the party would have to decide who will take the reins in case of that outcome.

An amazing paradox is in existence: Berlusconi – his party included – is pro-Europe and pro-euro, while LN is anti-euro and is considered a populist party; to enhance reader understanding, LN could perhaps be viewed as Italy’s equivalent of Marine Le Pen’s Front National (National Front). Berlusconi’s influence and him taking a “euro-friendly” stance on important issues that have to do with the eurozone and more widely the EU, is rendering a government involving LN as not something that markets – the euro – should view as much of a threat. In essence, Berlusconi is seen as acting as a buffer to the rise of populism. Lastly, it is worth mentioning that some analysts are saying that right-wing votes tend to be underestimated in polls due to a so-called “shy-factor”. Past Italian elections give credit to this view, which if proved right, then the centre-right might secure the desired majority.

Regarding the centre-left coalition, that is overwhelmingly led by the ruling PD and is polling at 27%. On its own, the PD is the second biggest party after M5S (23% versus close to 28%), though it’s been losing support as we’re getting closer and closer to election day. The PD has traditionally been a pro-European party.

A hung parliament and a probable grand coalition is the most likely outcome and the one preferred by markets. The potential scenarios though are numerous and delving into them might pointlessly detract from the essence – there could also be repeated failed attempts to form a government, resulting in fresh elections. It would be fruitful and interesting though to go through the one outcome (despite it not being the most probable) that undoubtedly has the higher odds of leading to the greatest market turbulence and one can extrapolate beyond that and more or less figure out the market reaction in case of an alternative scenario.

A government led by M5S would qualify as the outcome spurring the most extreme market movements, likely resulting in considerable euro weakness versus other currencies. Is that justified though? The argument being pushed forward is that such a reaction would provide opportunities to buy the dip for those investors realizing that such a behavior – shorting the euro – would merely constitute a market overreaction. The reasoning being that M5S has altered its rhetoric on many of the things it was originally against, moving towards a more moderate stance. Perhaps more importantly, the party no longer wants to hold a referendum on Italy’s membership in the single currency.

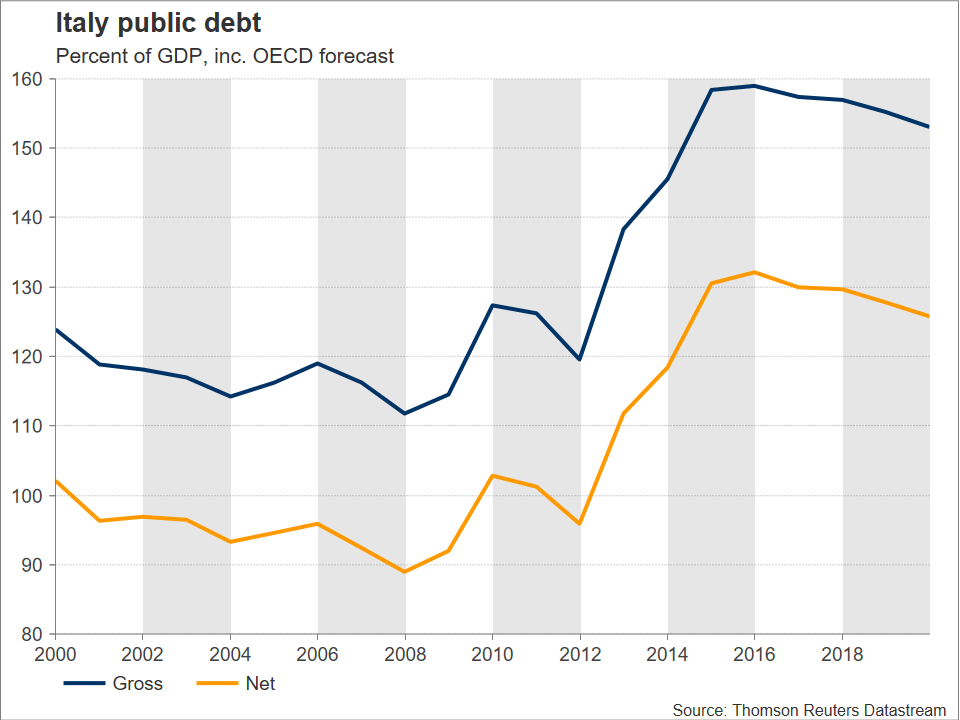

At the end of the day, the Italian elections could deliver more of the same. The real risk for Italy and the euro might not be March 4th, but a widespread crisis later on should those in power keep on kicking the can down the road, in the meantime allowing problems to grow up to the point they could not be longer be managed. Growth is picking up in Italy but is still far from inspiring (not far above 1.5% on an annual basis in Q4), Italian public debt is high, bureaucracy is stifling entrepreneurship and investment, and non-performing loans continue to haunt Italian banks despite efforts to improve the situation.

Another event that could incentivize market participants to short the euro and deserves mention is Germany’s Social Democratic Party (SPD) disapproving entering into a coalition to form a government with Chancellor Merkel’s conservative bloc. The SPD’s voting process begins on February 20 and the results could be known around the time the Italian elections take place. The odds are in favor of a ratification of the deal that was struck with Merkel’s conservatives.

Author

Andreas holds an MSc in Finance from Warwick Business School in the UK and a BSc in Business Administration (Finance major) from the University of Cyprus.