ISM Manufacturing Purchasing Managers’ Index March Preview: Consumer confidence reinforcement

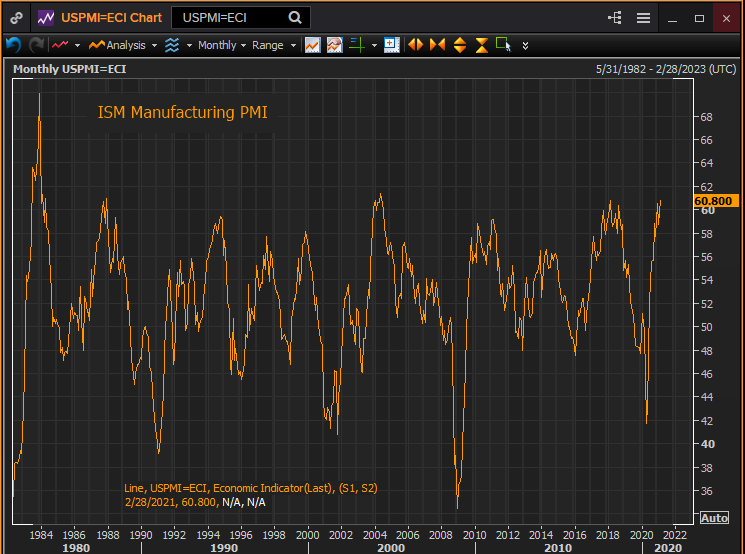

- February PMI at 60.8 was the highest since August 2018.

- March PMI forecast of 61.3 would be the highest since May 2004.

- Consumer optimism was unexpectedly strong in March.

- Markets have been keyed to improving US statistics.

Managers in the manufacturing sector have rarely been as optimistic as they are now.

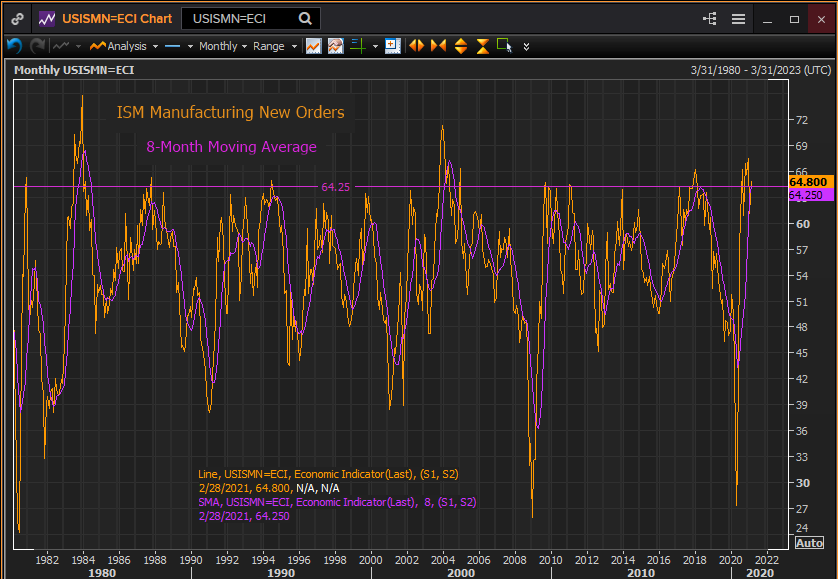

The Purchasing Managers’ Index (PMI) from the Institute for Supply Management (ISM) is forecast to rise to 61.3 in March from 60.8 in February. The Employment Index is expected to slip to 53 from 54.4 in February and the prices Paid Index should fade to 85 from 86. The crucial New Orders Index was 64.8 in February.

Manufacturing PMI, which polls the business outlook of the sector’s managers, has only been as positive three times in the last forty years: in 2005 for two months, in 1987 for one month and in 1983 and 1984 for seven months.

Manufacturing PMI

Source: Retuers

Manufacturing PMI

Manufacturing optimism is simple to fathom, incoming business is setting records.

The New Orders Index averaged 64.25 for the eight months from July to February. This is the highest this gauge has been in 16 years, since the second and third quarters of 2004.

In fact, there has only been one other run of orders as extensive as this in the past four decades and that was during the Reagan boom in 1983 and 1984.

New Orders Index

Source: Reuters

The $1400 stimulus payment that arrived for most families in March is likely to produce another consumption boom like the 7.6% burst in Retail Sales from the January $600 stipend.

The lockdowns and the induced recession of the past year delayed or blocked many consumer business purchases.Their rebound is the source of the exceptional order flow of the last eight months. Manufacturing firms may also be having a more difficult time sourcing parts and raw materials, lengthening production times and order completion..

Nonetheless, the result has been a sustained manufacturing boom the likes of which has not been seen since the 1980s. .

Factory employment has been the rub. The recovery of the Employment Index has only reached 54.4 in February, despite the optimism in the overall index.

This is far below the excellent labor market of 2017, 2018 and 2019. A time of rising wages and low unemployment for American workers as good as any since 1980.

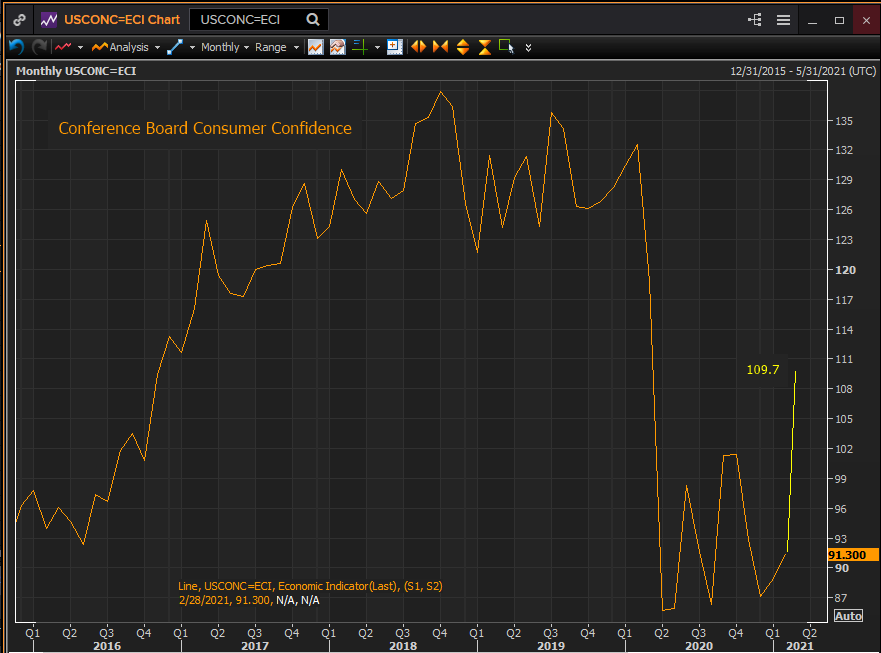

Consumer Confidence

Confidence among US consumers soared in March.

The burgeoning vaccination program coupled with a reviving labor market, the promise of stimulus payments and a government spending binge, have brought consumer optimism to its highest levels since the pandemic advent last winter.

The Conference Board March Consumer Confidence index rose sharply to 109.7 from 91.3 in February far outstripping the 96.9 forecast. Sentiment is now about half-way between the February 2020 score of 132.6 and the April panic low of 85.7.

Conference Board Consumer Confidence

Source: Reuters

Separate indexes for the Present Situation and Expectations also jumped in March, to 110.0 from 89.6 and to 109.6 from 90.9.

The Michigan Consumer Sentiment Survey reached 84.9 in March, its highest score in a year, from 76.8 prior, easily surpassing the 78.5 forecast. This index is also about half-way between its February 2020 reading of 101 and the April low at 71.8.

The unexpected strength in both consumer indexes is most likely due to a revival of labor market.

Consumer confidence and employment

The most important ingredient in consumer confidence is employment.

The greatly improved outlook for most Americans in March is not explicable without a recovery in the jobs market. .

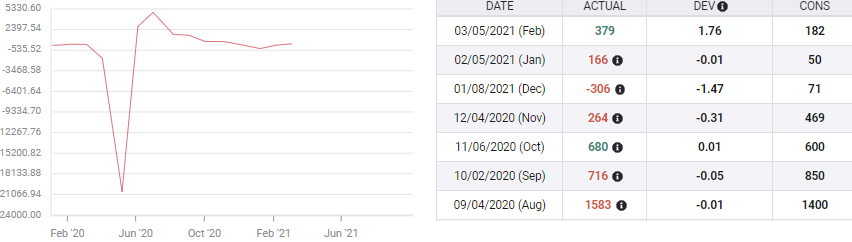

Nonfarm Payrolls are expected to add 639,000 jobs in March which would be the highest total since October’s 680,000.

Nonfarm Payrolls

Source: FXStreet

Automatic Data Processing (ADP) saw 517,000 new workers in March, slightly less than the 550,000 forecast but the February total was revised higher by 59,000 to 176,000.

Conclusion and markets

The optimism of manufacturing executives is based on reality and logic.

Orders have poured into factories for more than six months. Consumer optimism is returning with employment and consumption backed by government subsidies, the boom should continue until the end of the year.

Treasury interest rates and comparative economics with Europe and Japan have kept the US dollar and equities buoyant this year.

If the manufacturing outlook rises, especially if the Employment Index jumps, markets will have the confirmation they need for further advances.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.