Is the forex market ready for a bullish surge? Nonfarm Payrolls and Fed takeaway analysis

S&P 500 bears made good progress initially as yesterday‘s data confirmed the hawkish Fed takeaway – yet my bond targets weren‘t met, indicating that the field is now open to the bulls, which allowed me to call for ES going up all the way to the Sunday futures open in the low 4,240s.

Following today‘s non-farm payrolls, which I though expect to be revised lower in the upcoming months just as the prior months were, I‘m looking for Fed Jun 25 hike odds going up, and the talk about raising only in Jul to gradually die down.

Let‘s move right into the charts – today‘s full scale article contains 3 of them.

S&P 500 and Nasdaq outlook

Solid volume, with daily animal spirits returning. What was beaten down to the proximity of supports (IWM, XLI, XRT, XLB), stabilized via some respectable upswings within respective ranges, and the ES rally got a distinctly less defensive posture than was the case on Wednesday. What was driving the upswing and doing well before (AI connected tech, communications and consumer discretionaries), continued its bullish job; The key confirmation of a turn higher to continue, came from financials.

I‘m also looking for stocks to weather the stronger than expected (than even I expected – major banks were way more guarded) non-farm payrolls finely – and the instinctive dip reflecting better odds of Jun 25bp hike, was already bought really fast. Intraday consolidation followed by more upside is the theme of today.

4,247 with 4,236 are nearest supports, but the march towards 4,283 (more than Friday‘s job) would rightfully get more attention once the 4,247 resistance turning support is gone.

In case you took me up on the daily bullish calls, and noted the hedges idea from Sunday‘s extensive article, you benefited. And even more so in case you‘re combining the full scope of services with the Twitter feed.

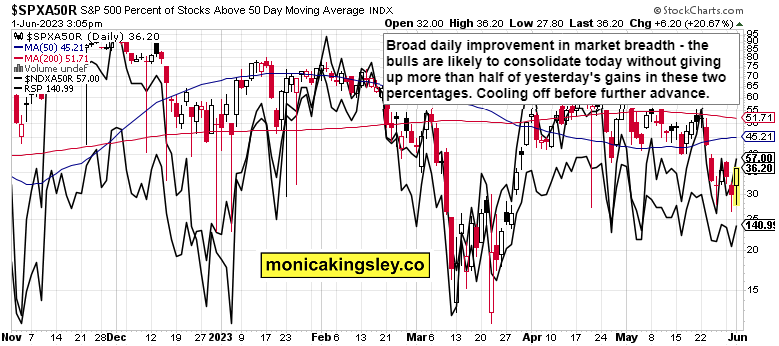

The market breadth for the whole S&P 500 and Nasdaq improved just enough yesterday to carry both sectors higher – as they consolidate sharp gains within their respective rotations. No warning sign of a crash today or Monday really.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.