Is Employment Growth at Risk to Waning Profits?

The financial position of the U.S. corporate sector has been deteriorating over the past few years, making it more vulnerable to any shock that would reduce earnings. Efforts to contain the new coronavirus represent one such potential shock. Could a decline in corporate profits at this stage of the economic cycle spillover into the labor market and trigger a recession?

In times of stress, one way for businesses to shore up finances is to reduce labor costs, i.e., cut jobs. We estimate that a 10% decline in before-tax profits has historically corresponded to a 1% decline in employment. That said, employment has fallen and the economy has slipped into a recession following more modest drops in profits, particularly when profits declined over a series of quarters. Timing also matters. A decline in profits is more perilous later in the economic cycle, when margins are falling and monetary policy is slow to become more accommodative.

Profit growth has been rather anemic, as economy-wide corporate profits have moved more or less sideways the past five years. Therefore with margins already falling and Fed efforts to ease financial conditions up in the air, the coronavirus and its potential hit to profits could yet lead to trouble for the jobs market.

Corporate Sector’s Financial Health Makes It Vulnerable to a Shock

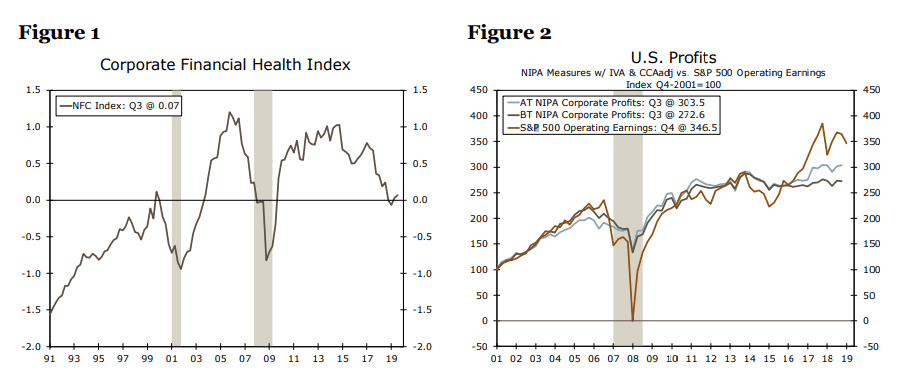

For more than a year now, we have been highlighting the deteriorating financial position of the U.S. corporate sector. Amid a record amount of debt in the non-financial corporate sector, interest coverage has eroded and net debt relative to earnings has climbed. Our own measure of corporate financial health, which captures eight financial metrics reflecting corporate balance sheets and income statements, is near its lowest levels since the past recession (Figure 1).1 At the same time, corporate profits growth remains rather anemic, as economy-wide corporate profits have moved more or less sideways over the past five years (Figure 2). While corporate finances do not appear so weak at present as to be the catalyst for the next recession, the more fragile financial position in recent years certainly makes the business sector more vulnerable to any economic shock that would reduce earnings.

Such a shock might be upon us. While currently our working assumption is that COVID-19 does not become a full-blown pandemic, it is hard to say with any certainty how events unfold from here. But measures being taken to stem the virus’ spread come with an economic cost. Corporate earnings are already in some degree of jeopardy as travel is curtailed, supply chains are disrupted and stores are closed. Could a deterioration in U.S. corporate profits spill over into key segments of the economy, like the labor market, and trigger a recession?

Source: Federal Reserve Board, U.S. Dept. of Com., S&P Dow Jones Indices and Wells Fargo Securities

How Big of a Drop in Profits Could Derail Hiring?

Businesses in financial peril are apt to cut costs where they can. Major expenditures like capital investments and labor are often on the chopping block. As we have seen in a number of recent periods, such as 2015-16 and the last three quarters of 2019, a decline in real business investment does not always translate to a recession. However, given the commanding share of economic activity driven by the consumer and households’ reliance on jobs for income, a decline in nonfarm payrolls has always corresponded to recession.

To determine the extent to which a decline in profits would affect employment, we employ a statistical technique to “shock” earnings.3 We then calculate an impulse response function between corporate profits and nonfarm payrolls. Specifically, we find that a 10% decline in corporate profits over a single quarter would lead to roughly a 1% decline in employment the following quarter. Such a shock can be long lasting, with the full effect not completely dissipating for about three years.

A 10% decline in profits over a single quarter is exceptionally rare. Indeed, such a drop has occurred once since the 1980s, when the financial crisis was at its height in the third quarter of 2008. However, employment has fallen and the economy has slipped into a recession following more modest quarterly drops in profits, particularly when profits declined over a series of quarters. By the time the past three recessions rolled around, corporate profits were down an average of 6% year-over-year.

Profits & Employment: Timing Matters

It is worth noting that wide-scale job cuts do not always follow periods of declining profits. For example, before-tax profits fell from late 1985 to the end of 1986 (Figure 3). That episode, however, was only shortly after the double-dip recessions of the early 1980s, so there had been little time for the economy to build up major imbalances. Moreover, the FOMC was still cutting interest rates from the marked levels that had been used to tame inflation early in the decade, while corporate profit margins were still expanding. Similarly, declining profits from mid-2014 to 2015 were not enough to stop job growth from strengthening over the period (Figure 3 again). There too, however, the economy was still emerging from the prior downturn, corporate margins were expanding and monetary policy was still highly accommodative.

Author

Wells Fargo Research Team

Wells Fargo