International trade: From shortage to surplus?

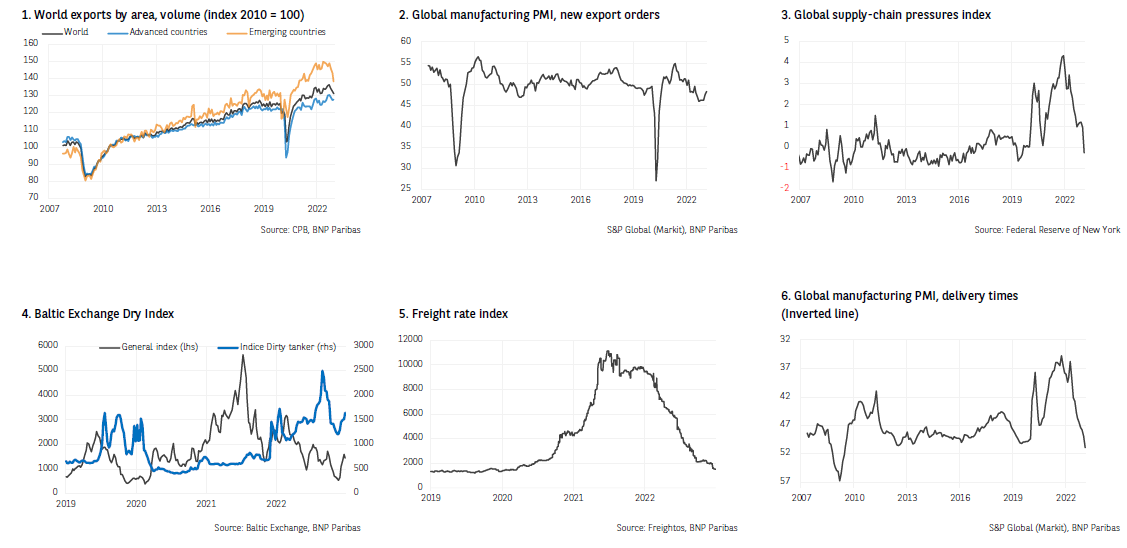

International trade data show quite clearly that the slowing of activity has been accentuated over recent months. Global export volumes (Chart 1), have continued to fall, according to the latest figures (December 2022). Health restrictions in China, which were only relaxed in mid-December, weighed on this dynamic. Nevertheless, global exports saw a 2.6% increase over the whole of 2022, relative to 2021.

The semiconductor sector, considered a good barometer of global activity, has seen falls in production levels and exports, which were amplified at the beginning of the year. This can be seen in particular in South Korea’s export figures, which are viewed as leading indicators: over the first 20 days of February exports, smoothed over three months, fell to their lowest level since October 2017. Although the risk of semiconductor shortages seems to have eased overall, supply in certain sectors, particularly the automotive industry, remains limited.

The slowdown in demand has eased further global production chains, in which bottlenecks had already largely cleared in the second half of 2022. The aggregate index of pressure on global supply chains (Chart 3) fell significantly in February as did the PMI delivery times component (Chart 6). Indeed, in February delivery times were the shortest since May 2009. Maritime freight (Chart 5) saw another fall of nearly 20% over the first half of March. Prices for container ship (Harpex index) were stable following a fall of 80% from its peak twelve months ago. However, the Baltic Dry Index of shipping costs (Chart 4) bounced back at the beginning of the year, due primarily to higher shipping costs for crude oil.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.