Inflation tracker May 2023

Central bankers continue to face high inflation, which has spread to almost all items in the consumer price index (CPI). While food inflation is still one of the main drivers of the CPI increase, the momentum in services continues to be strong. Services inflation slowed slightly in the US in March (+7.3% y/y), whereas it accelerated in the UK (+6.6%), the Eurozone (+5.2%) and, to a lesser extent, in Japan (+1.5%). Higher rent prices largely contribute to services inflation in the UK and the US. However, in all regions, other services items are rising significantly too, including transport services (mainly in the US), leisure and culture (euro area, UK), education (Eurozone, UK), and health (UK).

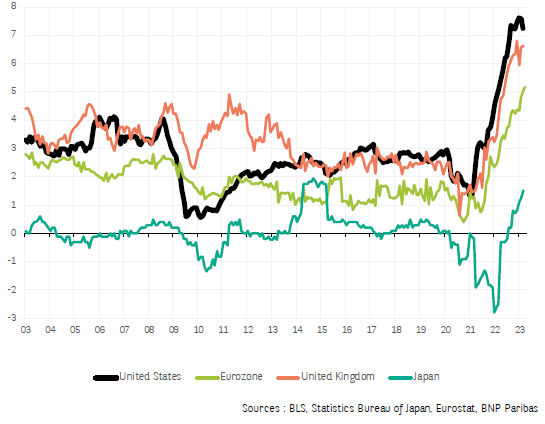

Core inflation stays elevated

High inflation is affecting almost all consumer price index (CPI) items. In Europe and the US, more than two-thirds of CPI components recorded an annual increase of over 4% in March. The UK is faring worst with 80% of components affected, while in Japan the figure is over 50% – unheard of in the country's recent past.

Eurozone inflation rose from 6.9% in March to 7.0% in April, according to Eurostat's preliminary estimate. The significant drop in energy prices in April 2022 (-4.0% m/m) led to an adverse base effect in April 2023, which contributed to the rebound in inflation for this component. A decline is likely in May: in particular, the “energy” HICP component fell again on a monthly basis in April (-0.8% m/m), down for the third consecutive month.

Underlying price pressures continued to build in the first quarter of 2023 in the euro area, although the increase slowed slightly to 5.6% in April (HICP excluding energy, food, alcohol, and tobacco). Core inflation in the US edged higher to 5.6% y/y in March, following a slowdown in previous months.

Food inflation continues to be one of the main drivers of inflation in all the regions surveyed, along with household goods and leisure and cultural activities (see heatmaps). However, even though food prices are rising strongly in the US (+8.5% y/y in March), their contributions to headline inflation is less than in the or Japan because of the significant weight of the “housing” item in the US (also up sharply by +8.2% y/y in March, CPI measure).

The situation is worse in the UK, where the surge in energy prices persists and contributed almost a quarter to headline inflation in March. Consumer price inflation in the country is still above 10% y/y, which is by far the highest level among G7 economies. This strong pace is being fuelled by significant wage increases (+7.0% y/y in February), which in turn are supported by a tight labour market.

Nevertheless, the PMI surveys give hope for a more pronounced disinflation phase to come: the price pressure indicator (aggregate of PMI indicators) has fallen sharply in recent months in all the countries covered. This corroborates the sharp slowdown in producer prices in recent months.

Household inflation expectations for the year ahead jumped in the US to 4.6% in April according to the University of Michigan survey, while they stabilised at around 4% in Japan (JCER). The figures for March in the euro area will be released by the ECB on 11 May. Forecasters have more measured expectations, with inflation in the US, Japan and the euro area not expected to exceed 3% in a year's time. Market expectations remain stable, except in Japan where the break-even inflation rate, which is structurally lower than in Europe or the US, has reached its highest level since 2014.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.