Inflation tracker – March 2023

How much disinflation can we expect this year? The sharp drop in energy prices from their peak in the summer of 2022 is progressively pushing down headline inflation and producer prices in most OECD countries. The base effects expected on the energy component of the CPI over the next few months should prolong this disinflation dynamic. The decline in the PMI indices for input prices and delivery times and, to a lesser extent, output prices, indeed indicate waning inflationary pressures.

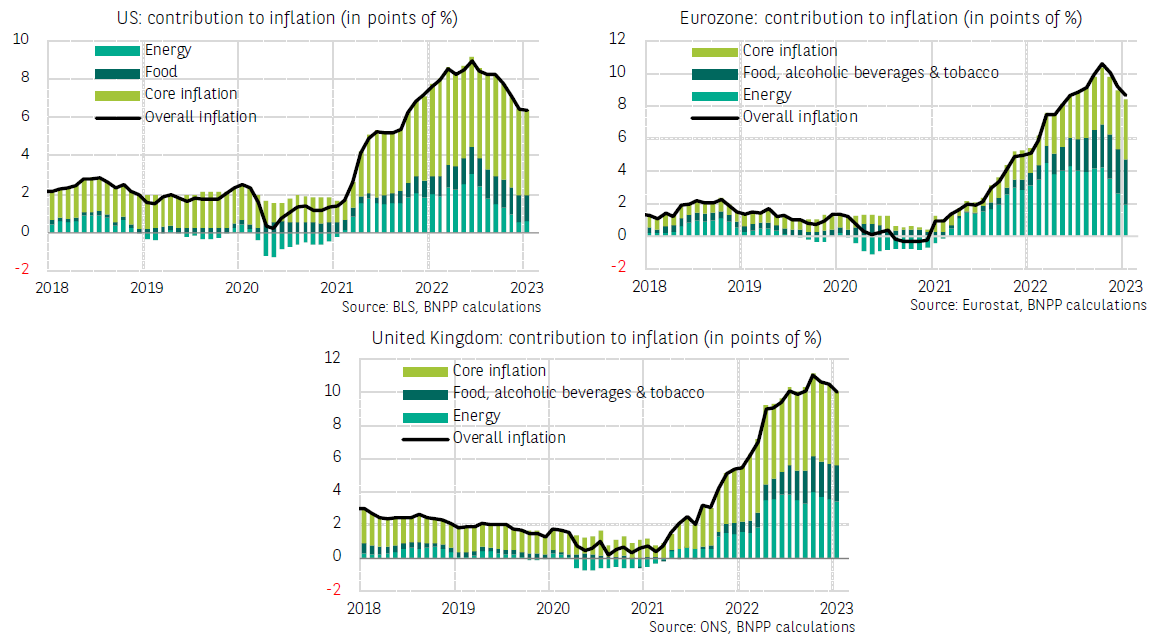

However, inflation in food products is not weakening at all, while it is accelerating in services. In the United States, services inflation reached 5.7% y/y in January on the CPI measure and 7.6% on the PCE measure, while the corresponding HICP in the eurozone rose to 4.4% y/y. Price increases in services slowed in the United Kingdom in January but remained higher than in the European Monetary Union and in the United States, at 6.0%.

The sharp rise in prices extends to different parts of the economy. The majority, if not all, of the CPI items are still rising at a rate well above 2% y/y.

Significant disparities exist between Euro Area countries. The rate of inflation remains very high in the Baltic countries (between 18% and 21%), in Slovakia (15.1%) and to a lesser extent in Austria (11.5%) and Italy (10.7%). Luxembourg (5.7%), Spain (5.9%) and Malta (6.8%) recorded the lowest price increases in January, thanks to a dissipation of energy inflation. In France, consumer inflation picked up again in January, to 7.0%, against 6.7% in the previous month.

In the United Kingdom, the surge in electricity and gas prices continued unabated in January (+89.5% y/y) and still contributed to nearly half of headline inflation. Combined with the rise in food prices, which is growing (16.8% y/y in January), and its repercussions in catering (+9.3%, included in the CPI), headline inflation in the country remains above 10%.

Long-term household inflation expectations in the United States and the eurozone have stabilized since the summer of 2022, and remain anchored at a level close to, although above, the 2% target aimed at by central bankers. Surveys of professional forecasters are in line with the household ones. The long-term expectations of British households are comparatively higher (above 4%) but remain in line with the average of the last ten years. On the markets, the break-even inflation rate fell below the 3% mark (United States, eurozone) or close to it (United Kingdom).

Wages are rising at a rapid pace in the United States and the United Kingdom, driven by a very resilient labour market and a historically low unemployment rate. While the knock-on effects of inflation on wages are, at this stage, less significant in the eurozone, they are growing.

General dynamics of inflation: Decomposition of inflation

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.