Inflation picked up in the euro area and the United States in December

Inflation regained ground in the United States and the euro area in December, rising from 3.1% to 3.4% and from 2.4% to 2.9% year-on-year respectively. However, the breakeven inflation rates (10-year bonds) for the four major eurozone economies have fallen below those of the United States. The breakeven rate has also dropped in the United Kingdom, where the inflationary environment has improved, although it remains more deteriorated than in the other areas.

The rise in inflation in the euro area can be explained by less energy deflation, linked to unfavourable base effects. On the core measure, inflation fell again, as did the 3m/3m annualised which fell to 1% at the end of 2023, a level below its historical average recorded before the pandemic (1.4% over the period 2000-2019). The increase in the prices of core goods (i.e. excluding energy) also slowed significantly (to 2.5% y/y and 0.8% on a 3m/3m annualised rate). Among the alternative measures being scrutinized by the ECB, we note the return of the PCCI index to 2% in November, a strong disinflationary signal that should lead to a more significant decline in other indicators ("supercore", median, trimmed mean).

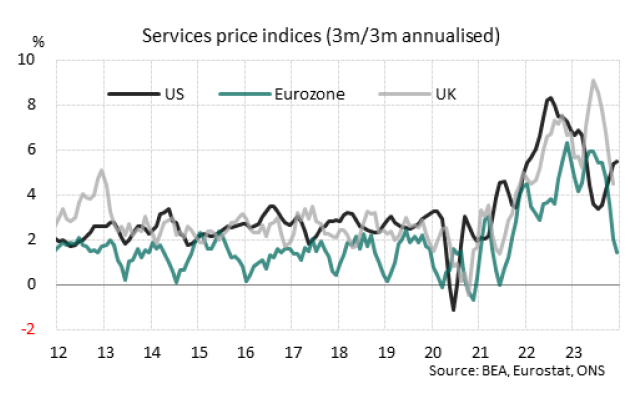

In the United States, disinflation in services (excluding shelter) continued in December, but the monthly evolution of the price index has deteriorated in recent months (the 3m/3m annualised rate has risen to 5.5%). The increase in the shelter component slowed only slightly to 6.2% y/y in December. However, household inflation expectations over the next twelve months have fallen to the lowest level in nearly three years (3.1% in December), according to the University of Michigan.

After surpassing the 4% y/y threshold at the beginning of 2023, both on the headline and core measures, inflation in Japan has gradually lost momentum. This was first achieved by a clear easing in energy deflation (favoured by the implementation of support measures for households by the government) and then, more recently, by a disinflation on manufactured goods. However, services inflation continued to strengthen to 2.3% y/y in November, the highest level since 1998.

In the United Kingdom, consumer prices fell for two consecutive months in October and November (seasonally adjusted). Inflation fell below 4% y/y for the first time in two years, but the increase in services remains significant (6.3% y/y), fuelled by significant growth in regular wages (+6.3% y/y in October).

Finally, the disruption of maritime transport in the Red Sea is causing, at the beginning of 2024, new tensions on global freight and some indices showed a sharp increase in transport costs in the first week of January (a doubling according to the Freightos index). Without generating a shock as large as in 2021, the situation could, if it continues, fuel an increase in imported inflation in 2024.

Chart of the month: More contrasted price developments in services

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.