Have we bought a golden ticket to the 1970s?

It turned out that time travel is possible, after all. All you need is reckless monetary policy and, boom, you are back in the 1970s. Gold seems to like such voyages!

Have you ever dreamed about time travel? Now it’s totally possible, courtesy of the Federal Reserve. Thanks to its dovish monetary policy, we are going back to the 1970s. Just as fifty years ago, the US central bank is letting inflation rise, claiming that the employment goal is much more important and that the Philips Curve has flattened. In the 1970s, they thought similarly, but it turned out that you can overheat the economy, after all! And just as Arthur Burns half a century ago, Jerome Powell believes that inflation is caused only by a few particular categories, and it will prove to be transitory.

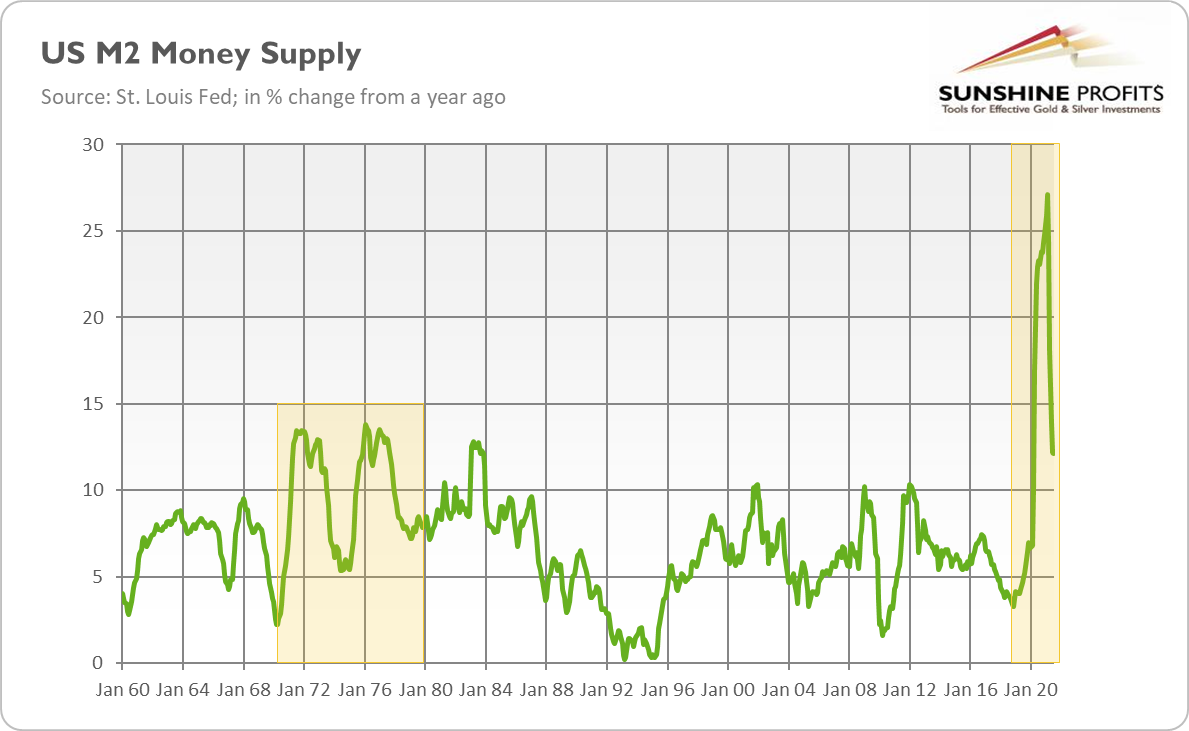

I’ve been pointing out these disturbing parallels for months. Now, as Kenneth Rogoff, Professor at Harvard University, noted, with the US humiliating exit from Afghanistan and the fall of Kabul, the similarities between the 1970s and the 2020s are growing. Other dangerous resemblances are relative fast growth in the money supply (see the chart below), fiscal deficits, and the presence of supply-side shocks (but instead of oil shocks we suffer from semiconductor shock and disruptions in other supply chains).

Rogoff also points out some important differences, namely, the independent central bank readiness to hike the federal funds rate if inflation gets out of control, and much lower interest rates that provide the Treasury with room for its lax spending.

There is a grain of truth in Rogoff’s claims. The central bank’s independence is much more strongly established, and Powell is a far cry from Burns who was submissive to President Nixon. However, please note that both private and public debts are much higher than fifty years ago. This mammoth pile of debt makes interest rate hikes much more politically painful. The high indebtedness is already a reason why the Fed maintains a dovish stance and will normalize its monetary policy at very a gradual pace.

Remember the Fed’s recent attempts to roll back quantitative easing and bring interest rates back to more normal levels? The economic slowdown and the repo crisis forced the Fed to cut the federal funds rate again and return to the asset purchases. It was in 2019, much before the pandemic started. So, never underestimate the power of the debt trap!

What does it all mean for gold? Well, if we are really going into the 1970s, gold could be one of the biggest winners. The yellow metal enjoyed a bull market then, so a similar positive scenario could replay now.

Although, fifty years ago the US economy entered stagflation, i.e., a period of high inflation and economic stagnation. The current situation is clearly not so bad — inflation is lower than in the 1970s, while the GDP growth is positive. However, the recent slowdown in economic growth, despite massive monetary and fiscal stimulus, suggests that a mini-stagflation may be underway. The spread of the Delta variant of the coronavirus hampers the economic growth, and both monetary and fiscal policies remain loose, contributing to the upward price pressure.

If the Fed’s story about transitory inflation is wrong, it will need to tighten its policy more decisively than expected. An abrupt tightening cycle could be negative for gold prices, as the yellow metal prefers an environment of low bond yields. However, aggressive steps to combat inflation could also cause a plunge in the prices of risky assets or even a financial crisis. So, if the Fed stays long behind the curve, gold should ultimately benefit – either from accelerating inflation or from the Fed’s harsh tightening triggering a sovereign debt crisis or an economic crisis (as a reminder, Paul Volcker contained inflation, but the US economy entered into a recession).

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Arkadiusz Sieroń

Sunshine Profits

Arkadiusz Sieroń received his Ph.D. in economics in 2016 (his doctoral thesis was about Cantillon effects), and has been an assistant professor at the Institute of Economic Sciences at the University of Wrocław since 2017.