Germany: A structural breakdown in the trade deficit with China?

German exports of goods increased by 2.6% y/y in the first 7 months of 2023 compared with the same period in 2022, but one usual destination is missing: China (-8%).

Chinese-German trade relations have been increasingly imbalanced for almost two years, with imports growing faster than exports. One change, linked to the war in Ukraine, remained transitory: the EUR 18 bn rise in German imports of Chinese chemical products in 2022 (due to fears of energy shortages in Germany) did not continue in 2023 and was, for the most part, corrected by the end of July 2023.

But more structural changes also seem to be at work. A number of sectors in which China is developing its exports (and local production as a substitute for imports) saw German bilateral deficits widen during January-July 2023, particularly electrical equipment (EUR -11.2 bn compared with EUR -4 bn two years ago). This underlines the erosion of Germany’s competitive position in the face of China’s move upmarket in these areas.

In parallel, German surpluses have fallen. While the surplus in the automotive sector remains high (almost EUR 20 bn), the decline in exports is clear: their sum over 12 months peaked at EUR 30.7 bn in September 2022 and totalled just 26.3 bn in July 2023. At the same time, German imports from China rose from EUR 4 bn to EUR 6.2 bn.

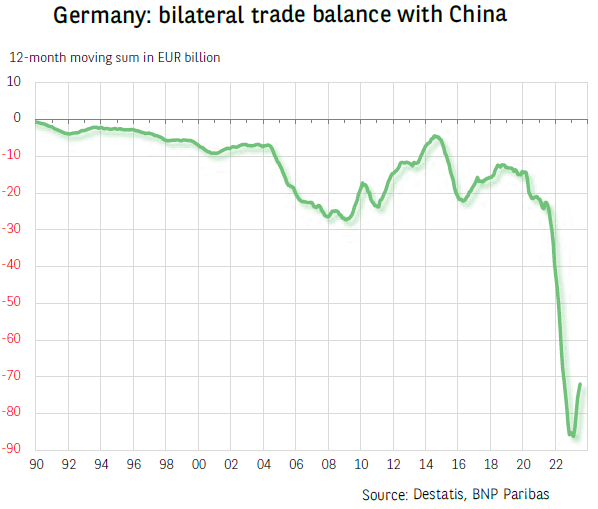

So, the situation has clearly changed. While Germany’s bilateral trade deficit with China ranged generally between EUR -15 and -20 bn in the years following China’s entry into the WTO in 2001 and up to mid-2021, it is expected to more than triple in 2023. This reflects a loss of market share for Germany in Chinese imports (4.2% of Chinese imports over the last 12 months to July 2023, when they were almost 1 percentage point higher two years earlier), while the share of China in German imports has remained stable at 12% (on the same points of comparison).

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.