German economic troubles could keep the Euro heavy

-

Eurozone economy narrowly avoided a recession last year.

-

Yet situation could get worse as Germany tightens spending.

-

Can the euro ignore deteriorating economic fundamentals?

No recession, but no growth either

The euro area miraculously dodged a recession last year, even despite inflation eating into people’s real incomes and high interest rates dampening demand. Most of the heavy lifting was done by Spain, which grew at a solid pace, offsetting a contraction in Germany.

Alas, overall economic growth was not impressive. Eurozone GDP rose by only 0.5% in 2023, which pales in comparison to the stellar 3.1% growth recorded in the United States. Therefore, the European economy has not collapsed, but it is almost stagnant.

Eurozone growth has been held back by Germany. The bloc’s largest economy has fallen into a technical recession, plagued by a sharp slowdown in global trade that has crippled the nation’s export-heavy business model, as Chinese demand in particular has lost steam.

Higher energy costs following the war in Ukraine have dealt another blow to German industry, making it less competitive as Russian natural gas was phased out. The decision to switch off the country’s last three nuclear power plants last year exacerbated this problem, by taking huge amounts of cheap energy supply offline.

In other words, Germany has turned into the ‘sick man’ of Europe, something reflected in business surveys that paint a gloomy picture of future growth.

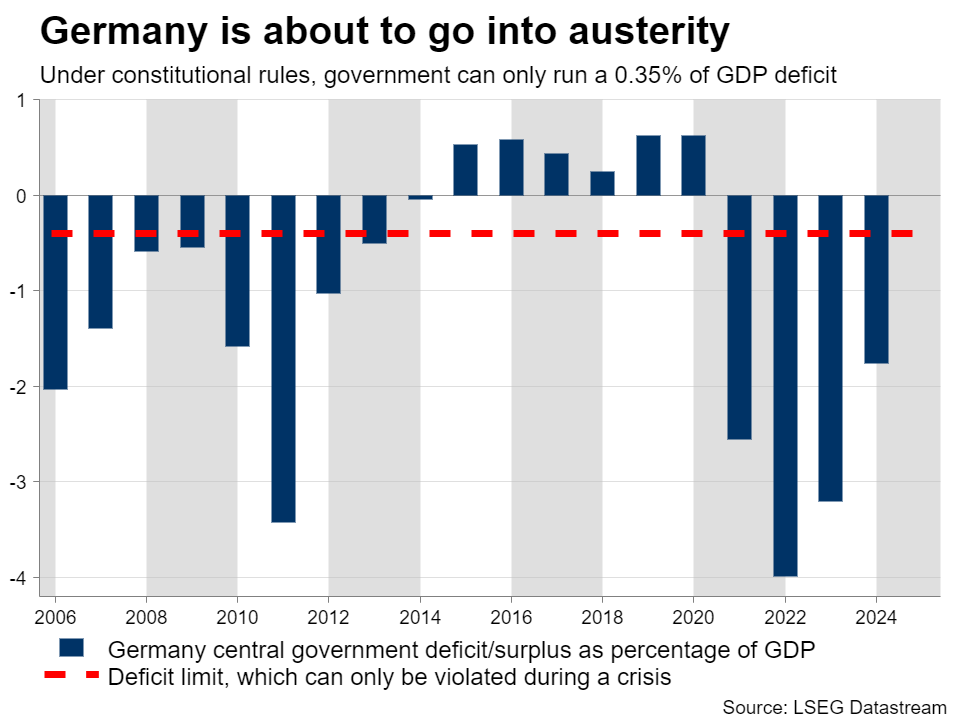

German debt rules bite

Faced with such a thorny situation, the natural response from the German government would be to stimulate the economy by raising spending levels and directing funds towards public investments and innovation.

Unfortunately, that won’t happen anytime soon. In fact, the German government is about to cut spending and investment levels, for legal reasons.

A bombshell decision by Germany’s constitutional court in November left a massive hole in public finances, after the court ruled that a plan to spend €60 billion on green investments was unconstitutional. In Germany, the government is required to balance the budget - a constitutional rule known as the ‘debt brake’.

Specifically, the government can only run a deficit of 0.35% of GDP, which is tiny. This rule was suspended in 2020 to deal with the costs of the pandemic, but the court’s ruling means these strict budget measures will return this year, bringing about a new era of austerity.

Hence, Germany desperately needs an injection of stimulus, but is about to be given a dose of austerity instead. That will likely dampen growth even further, raising the risk that the economy falls deeper into recession.

Reforming the debt brake to allow for larger deficits would require a two-thirds majority in Parliament, which is almost impossible right now, as the political landscape is extremely fragmented and the largest opposition parties are opposed to such a move.

Where does all this leave the Euro?

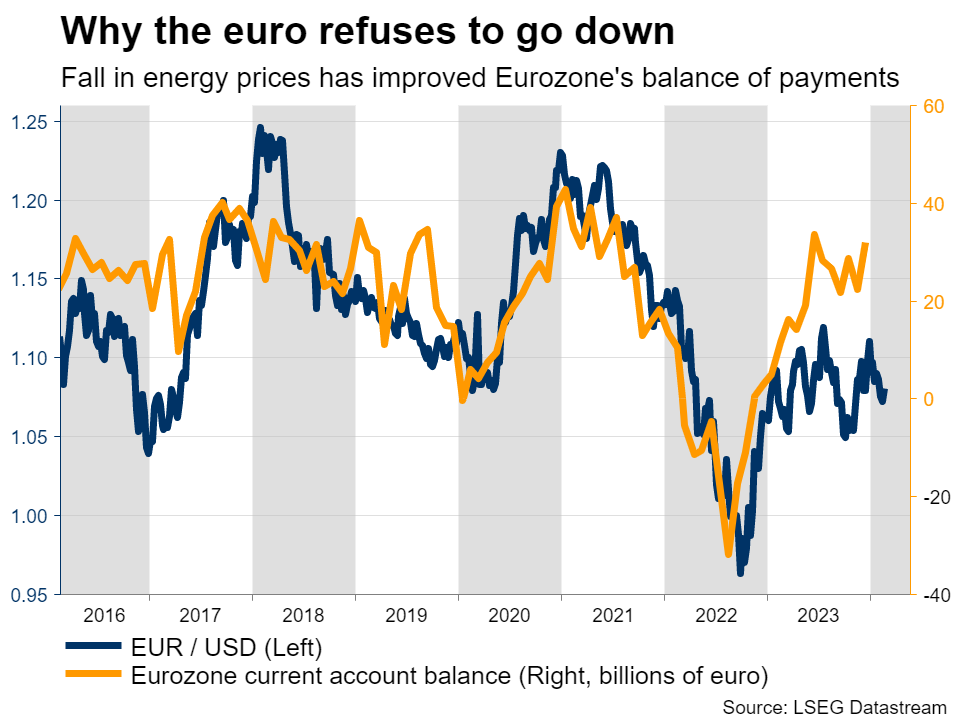

In a nutshell, worse growth in the Eurozone’s largest economy is bad news for the euro. It implies faster rate cuts by the European Central Bank, which would remove a key source of support for the single currency.

Net trade has been the main factor keeping the euro from depreciating over the last year. The Eurozone’s current account returned to a surplus in 2023, helping to fuel real demand for the currency. That said, this surplus was driven mostly by the sharp decline in global energy prices over the last year.

Another helpful element has been the astonishing rally in the stock market. A cheerful tone in financial markets is generally negative for the US dollar, which often acts like a safe-haven asset. As such, it tends to benefit the other side of the coin - the euro.

Blending it all together, the euro has been kept afloat mostly by helpful developments in global markets, which have negated the selling pressure from deteriorating economic fundamentals. The question is whether and how this dynamic will change moving forward.

The Eurozone economy has shown some early signs of stabilization lately, but with Germany’s economic malaise set to deepen as it embraces austerity, it’s probably too early to talk about a sustainable recovery. That sets up a scenario where the ECB slashes rates faster and deeper than what markets currently anticipate, which could keep the euro on the ropes.

Ultimately, investors are attracted to economies that are growing fast or offer high interest rates. If both of these factors are moving in the wrong direction, it is a tough environment for any currency.

Author

Marios graduated from the University of Reading in 2015 with a BSc in Economics and Econometrics. Prior to joining XM as an Investment Analyst in December 2017, he was providing financial analysis, reporting and consulting service