Geopolitical conflict threatens yet another shipping choke point

Global shipping routes are already heavily impacted from the Red Sea to the Gulf of Aden because of ongoing geopolitical strife. If the Strait of Hormuz is in any way disrupted, the impact on oil and global trade could be huge.

It's a stark fact: more than 80% of global goods trade is transported by sea. And any disruption in maritime trade can have a profound impact on the worldwide economy. The latest potential flashpoint is the Strait of Hormuz. It's a vital artery that carries around a fifth of the world's oil. It's been at the centre of numerous geopolitical tensions for many years. Any disruption could have yet another negative economic impact on the global economy, hampering vital trade routes and lengthening transit times, resulting in production delays and higher inflation.

But the Strait is not the only place where there's deep concern about security.

Trade and shipping are increasingly politicised

For some time now, the Strait of Bab el-Mandeb-Suez Canal, which handles around 15% of global maritime trade, has seen significant disruption due to attacks by Houthi rebels on ships in the region. The Red Sea is still largely being avoided, with daily transits down two-thirds year-on-year, according to IMF PortWatch data. On the other side of the globe, a drought at the Panama Canal, which handles 5% of global maritime trade, is slowly improving as daily transits have risen to 27 in March from 24 in January and 22 in December 2023. Yet, capacity is still off the normal daily average of 34-40 transits, a level currently only expected to be reached again by 2025. And next to this, shallow waters in the world’s main inland shipping waterways could easily return over the course of this year.

Elevated risks could quickly impact trade routes once seafarers and cargo are threatened

Due to the mounting tension in the Middle East, those risk-laden waters have spread from the Red Sea to the Gulf of Aden, and the vital Strait of Hormuz could be caught up in it too. It was only days ago that Iranian forces seized the MSC Aires container vessel. We know from all the disruption in the Red Sea that elevated risks could quickly impact trade routes once seafarers and cargo are threatened and insurance risk premiums go up. As such, trade has become increasingly politicised. It's worth noting here that another maritime area in the scope of geopolitical risks is the Taiwan Strait, which is a gateway to large Chinese ports.

When it comes to international trade, it's difficult to quantify the financial effect of one or two events, whether they're geopolitically related or not. That said, you may recall the blockage of the Suez Canal by a container ship, Ever Given, in 2021. That led to an estimated loss of 0.2 to 0.4 percentage points in global trade. Low water levels in the Rhine in Germany had a negative impact of 0.3% on GDP numbers due to higher transport and trade costs and production delays.

Three of the world’s key maritime choke points currently face disruption

-638490275747699176.PNG)

Source: ING

The Strait of Hormuz is a key route for global oil and LNG transport

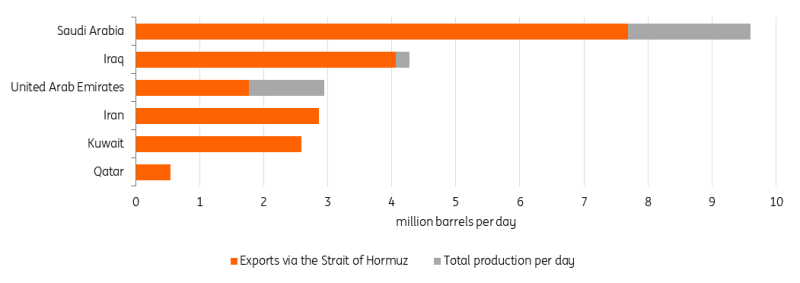

Here's why the Strait of Hormuz, that key maritime choke point connecting the Persian Gulf with the Gulf of Oman, is in trade watchers' focus. The Strait is critical for transporting oil, petroleum products and LNG. Saudi Arabia, Iraq, UAE, Kuwait, Iran and Qatar produced 22.8 million barrels of oil a day, and some 20 million were transported daily via this route. That equates to 20% of global crude and refined product consumption.

If Iran were to attempt to disrupt or block oil flows through the Strait of Hormuz, the country itself wouldn't be the only one which would suffer. Iraq, Qatar and Kuwait would be severely disrupted as these countries usually transport 100% of their crude oil exports through the Strait of Hormuz. Unlike the Red Sea, there’s no real alternative for shipments through this channel. To some extent, the East-West crude pipeline (Abqaiq-Yanbu) across the Arabian Peninsula and the Abu Dhabi Crude Oil pipeline are alternatives for Saudi Arabia and the United Arab Emirates. The former, however, leads into the already circumvented Red Sea.

In addition, a significant amount of LNG passes through the Strait of Hormuz. Qatar, the third largest LNG exporter in 2023, shipped 108bcm of Liquefied Natural Gas through the choke point, which is around 20% of total global LNG trade. Given that Qatar is set to boost capacity to more than 170bcm by 2027, the Strait will become even more important for LNG flows. Clearly, with Europe increasingly more reliant on LNG since the Russia/Ukraine war, any disruptions to the LNG market will be felt more in Europe.

Tensions have already been reflected in somewhat higher oil prices, with a large risk premium already priced in before last weekend. This could easily lead to supply concerns should the situation escalate. According to LSEG Oil Research, most of the crude and condensates shipped through the Strait of Hormuz went to Asian markets, putting those economies more at risk of a potential supply cut. However, given the global nature of the oil market, all regions would be affected by higher oil prices in the event of a blockade.

For the tanker shipping market, this means yet another headache it could do without after sanctions on Russia already led to significant shifts in oil trade patterns and much more sea mileage. These new tensions will keep tanker rates elevated and may even send them higher still.

Production and export of crude oil via the Strait of Hormuz in 2023

Exports via Strait of Hormuz based on AWR Llyod analysis estimates from 2021. Million barrels per day.

Source: OPEC MOMR April 2024, AWR Llyod analysis, ING calculations

For the time being, oil supply remains intact, although the risk of tensions in the Middle East making things much worse is growing. The lack of any significant price reaction following Iran’s recent attack on Israel is largely due to a large risk premium already having been priced into the market. ICE Brent rallied from a little more than $86/bbl at the start of April to over $90/bbl in anticipation that Iran would respond to Israel’s suspected airstrike on its embassy in Syria.

Secondly, the market is also in limbo, still waiting to see how Israel will respond to the aggression. The longer the market waits, the more likely the risk premium starts to fade. Risks to oil supply are at their highest since October last year. Any further escalation would only bring the oil market closer to actual supply losses. We believe there are three key supply risks facing the oil market as a result of current tensions, which we discuss in this article.

On the demand side, ongoing economic headwinds might also offset supply restrictions to some extent, with the Chinese and eurozone economic growth path improving but remaining subdued overall. With plenty of risk facing the market, we will not be the only ones closely monitoring the tensions in the Middle East and those crucial maritime choke points.

Read the original analysis: Geopolitical conflict threatens yet another shipping choke point

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.