GBPUSD Weekly Forecast: Risks skewed to the downside in US inflation week

- GBPUSD slumped to two-week lows amid Fed-BoE policy divergence.

- US Dollar cheered the hawkish Federal Reserve stance but inflation data holds the key.

- GBPUSD’s daily technical setup points to more downside in the offing.

The relief rally in the GBPUSD pair was shortlived, as the monetary policy divergence between the US Federal Reserve (Fed) and the Bank of England (BoE) overshadowed the renewed UK political calm. The pair booked the first weekly loss in four amid resurgent demand for the US Dollar (USD) and US Treasury yields. What’s next for the Pound Sterling (GBP) and the USD, as attention turns towards the United States mid-term Congressional elections and the critical Consumer Price Index (CPI) data in the week ahead.

What happened last week? Fed, BoE fade GBPUSD rally

It was all about the build-up around global tightening expectations, as the Federal Reserve and the Bank of England held their monetary policy announcements. Markets had fully priced in a 75 bps Fed rate increase while the odds of a super-sized BOE raise stood at 98%, despite the lack of clarity on the UK budget.

The GBPUSD rally, fuelled by the renewed optimism on the new UK government and its fiscal framework, quickly faded amid an extended recovery in the US Dollar alongside the US Treasury bond yields. Risk-aversion gripped the market at the start of the week on disappointing business activity and increased covid lockdowns in China, benefiting the safe-haven USD. However, the US Dollar failed to preserve its recovery momentum and slipped on Tuesday after risk-on flows seeped back on the Reserve Bank of Australia’s (RBA) only 25 bps rate hike, upbeat China’s Caixin Manufacturing PMI and reopening optimism. Pound Sterling bulls attempted a comeback but they remained rather cautious ahead of the Fed and BOE policy meetings.

On Wednesday, sellers returned after GBPUSD failed to sustain above the 1.1500 barrier, as the greenback found renewed demand on the back of above-forecasts JOLTS Job Openings data and ISM Manufacturing PMI from the United States. Investors also resorted to position adjustments ahead of the critical Federal Reserve policy decision, lifting the American Dollar in tandem with the Treasury yields across the curve. The Federal Reserve announced the expected 75 bps rate hike, with Chair Jerome Powell sticking to its hawkish rhetoric. Powell said during the press conference that further rate increases are needed and that the terminal rate is likely to be higher than previously estimated. The US Dollar dived in an initial reaction to the Fed decision but made a solid comeback on Powell’s words, drowning GBPUSD to one-week lows at around 1.1380.

The sell-off intensified on the BoE’s ‘Super Thursday’ and the currency pair tumbled to two-week lows near 1.1150. The Bank of England followed the Fed’s footsteps and raised the policy rate by 75 bps but Governor Andrew Bailey differed from Powell on the view of the terminal rate. The British central bank warned that the economy will sink into deeper recession while Bailey said that rates are likely to rise less than the market’s expectations. The monetary policy divergence between the Fed and BOE came to the fore once again and added to the Pound Sterling’s plight.

On the final trading day of the week, GBPUSD licked its wounds, awaiting the US Nonfarm Payrolls (NFP) data. The positive shift in the market sentiment pushed the US Dollar lower from nine-day highs, despite buoyant US Treasury yields. The pair witnessed a major turnaround in the American trading hours after the US Dollar correction gathered steam on the release of the NFP data. The headline payrolls climbed to 261K in October vs. 200K expected. Meanwhile, the Unemployment Rate rose to 3.7% from 3.5% and the Average Hourly Earnings, dropped to 4.7% from 5%. Softer wage inflation data from the United States seemed to have accelerated the USD sell-off while driving GBPUSD back above 1.1300 heading into the weekly closing.

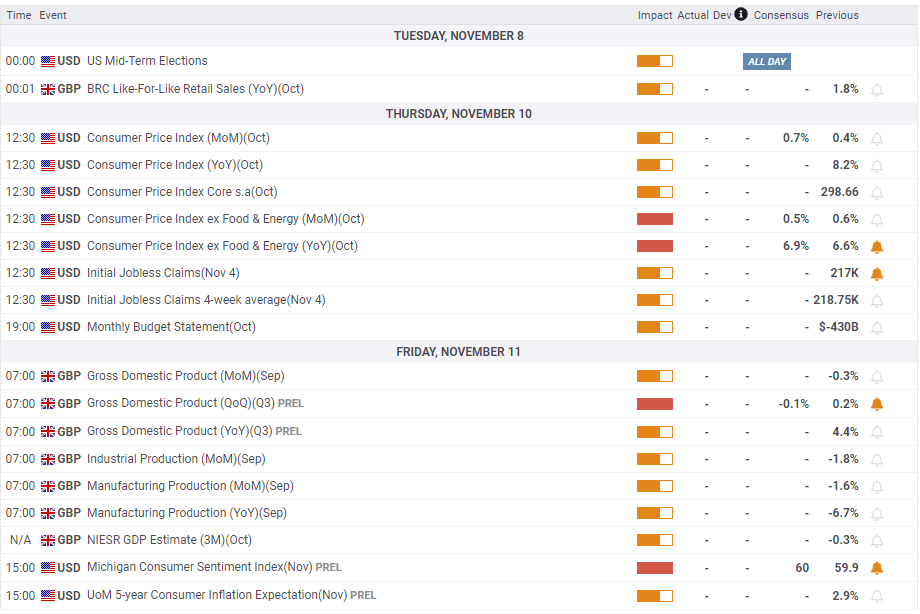

Week ahead: Critical United States events in focus

After a busy and eventful week, Pound Sterling traders brace gear up for a relatively quiet start to another data-heavy week ahead. Monday is a data-dry calendar day on both sides of the Atlantic but Federal Reserve policymakers will keep markets entertained.

On Tuesday, Bank of England Chief Economist Huw Pill will speak amid a lack of any top-tier US or UK economic data. Mid-term Congressional elections in the United States will be closely watched, as the outcome will influence the playing field for the 2024 presidential campaign and, therefore, the US Dollar valuations and risk trends. There is nothing much of relevance, in terms of economic releases, on Wednesday.

The US CPI (inflation) data will hog the limelight on Thursday, which will offer fresh hints on the potential Fed policy action. A bunch of BOE and Fed officials will be on the rostrum. The commentary will be closely scrutinized following the previous week’s policy announcements.

On Friday, the UK Preliminary Q3 Gross Domestic Product (GDP) will be reported alongside the monthly growth figures and Industrial Production data. The US will observe the Veterans Day holiday but the Preliminary University of Michigan Consumer Sentiment and Inflation Expectations data will be published.

GBPUSD technical outlook

As observed on the daily sticks, GBPUSD confirmed a rising wedge breakdown after closing Thursday below the rising trendline support, then at 1.1407.

Given that and BOE-led massive sell-off, a sharp pullback in the Cable was well-justified. However, the further upside appears elusive, as a dense cluster of healthy resistance levels is stacked up around the 1.1320 region. At that level, the bearish 21 and 50-Daily Moving Averages (DMA) coincide.

If GBPUSD bulls manage to find a foothold above the latter, then the rising wedge support-turned-resistance, now at 1.1445, could come into play. Acceptance above the latter will initiate a meaningful recovery towards the confluence of the wedge resistance and the descending 100-DMA at 1.1693.

On the downside, if the two-week low of 1.1147 gives way, then the next support is seen at the October 21 low at 1.1060. A breach of the latter will open up deeper declines towards the October 12 low at 1.0923. Failure to defend that cap could trigger a sharp sell-off towards the 1.0550 demand area.

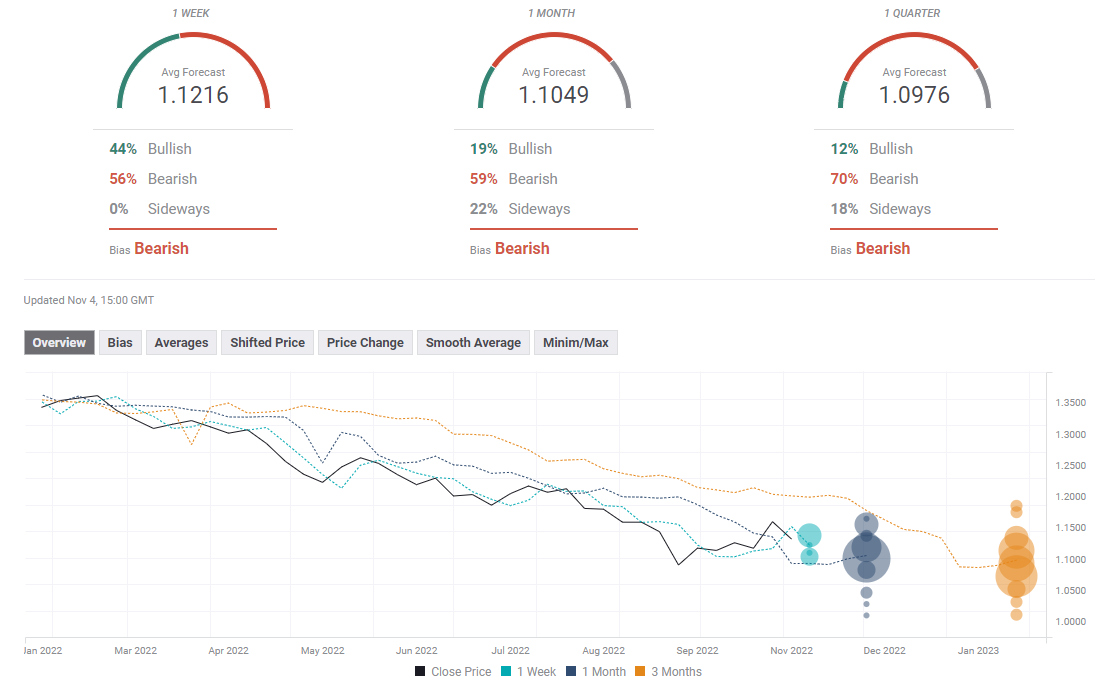

GBPUSD sentiment poll

FXStreet Forecast poll paints a mixed picture for GBPUSD in the short term. The bearish bias stays intact in the one-month view with the average target sitting at 1.1050.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.