GBP/USD stays under sellers' control despite pause [Video]

![GBP/USD stays under sellers' control despite pause [Video]](https://editorial.fxstreet.com/images/Markets/Currencies/Majors/GBPUSD/uk-pound-and-united-states-ten-and-twenty-dollar-bills-60942778_XtraLarge.jpg)

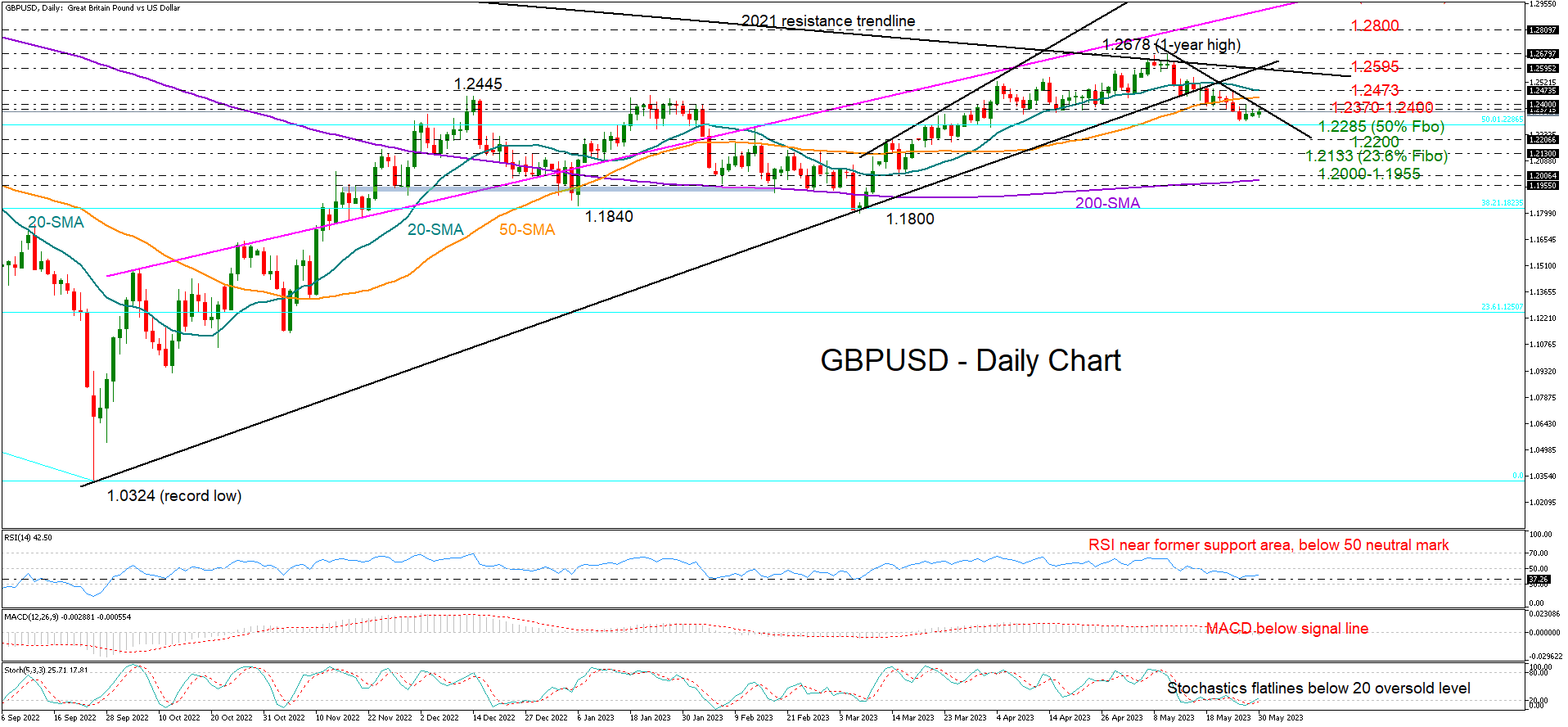

GBPUSD opened the week on a neutral note, consolidating its bearish correction from a one-year high within the 1.2300 zone.

According to the technical picture, the sideways move could be temporary within the bearish wave. The downfall below the 20- and 50-day simple moving averages (SMAs) and beneath the former 1.2445 ceiling could motivate more selling in the short term. The negative trajectory in the RSI and the MACD is another sign that the sell-off has not bottomed out yet.

An upside correction, however, cannot be ruled out either as the RSI has reached its previous support area, while the stochastic oscillator has been flattening within the oversold region for two weeks now.

If selling pressures resume, the 50% Fibonacci retracement of the 2021-2022 downtrend could provide a footing around 1.2285, preventing a continuation towards the 1.2200 mark. A steeper decline could stabilize around the 1.2130 constraining zone, while lower, the door would open for the 1.2000 number and the 200-day SMA.

On the upside, traders will likely wait for a bounce back above 1.2370-1.2400 before they target the 20-day SMA at 1.2473. A successful move above the latter could clear the way towards the tough resistance trendline at 1.2595, which has been capping bullish actions since May 2021. If buying interest persists, the pair may attempt to climb above May’s peak of 1.2678 and continue towards 1.2800, where it paused several times during 2019.

All in all, GBPUSD keeps facing a blurry short-term outlook. The next bearish round could start below 1.2285.

Author

Christina joined the XM investment research department in May 2017. She holds a master degree in Economics and Business from the Erasmus University Rotterdam with a specialization in International economics.