GBP/USD Weekly Forecast: More downside in the offing, with eyes on US debt deal, NFP

- GBP/USD booked third weekly loss, as haven demand boosted the US Dollar.

- United States debt-ceiling uncertainty likely to extend ahead of the June 1 deadline.

- GBP/USD’s daily technicals point to more downside ahead of key US Nonfarm Payrolls.

Pound Sterling sellers flexed their muscles amid persistent demand for the safe-haven US Dollar, as the uncertainty over the US debt-ceiling issue sapped investors’ confidence. GBP/USD extended its corrective downside into the third week, despite the hot inflation data from the United Kingdom. The focus now shifts toward the all-important United States Nonfarm Payrolls data and US debt-ceiling updates for a fresh direction in the major.

GBP/USD: What happened last week?

The ebb and flow of risk depended on the back of the developments surrounding the United States debt-ceiling negotiations emerged as the main underlying theme, strengthening the recovery in the US Dollar across its major peers. The Greenback also benefitted from hawkish commentary from US Federal Reserve (Fed) policymakers and encouraging data, which raised expectations of a 25 basis points (bps) rate hike in June while pushing back rate cuts bets.

The US Dollar climbed to two-month highs, tracking the upsurge in the US Treasury yields, at the expense of most counterparts. GBP/USD extended its correction and challenged the 1.2300 demand area amid unabated US Dollar buying interest. The US Dollar Index surpassed the 104.00 level, while the benchmark 10-year US Treasury bond yields firmed up to two-month highs just below the 4.00% key level.

Despite mixed US Preliminary Manufacturing and Services PMI data and Federal Reserve Minutes of the May policy meeting, hawkish Fed bets were underpinned by the upward revision to the US Q1 GDP data and upbeat weekly Jobless Claims report. US Jobless Claims for the week ending May 20 increased to 229,000 but came in lower than the market expectations of 245,000. Meanwhile, the United States GDP increased at an annual rate of 1.3% in the first quarter of 2023, which is an increase from the first estimate of 1.1% and above economists' estimates of 1.1%. In the wake of strong US economic data, the market’s pricing for a 25 bps June Fed rate hike rose to nearly 40% when compared to odds of about 12% at the start of the week.

The GBP/USD pair also took the lead from the ongoing US debt-ceiling negotiations between President Joe Biden and House Speak Kevin McCarthy throughout the week. On Monday, Senior White House Adviser Steve Ricchetti said, “We’ll keep working tonight". Meanwhile, Biden said that his discussion with McCarthy "went well” following Sunday’s meeting. Talks continued and were said to be productive until negotiations remained at an impasse after McCarthy said on Wednesday that the two parties had yet to reach a deal, while senior US officials said there were no more meetings planned and announced a recess on Thursday.

However, some reports carried by Reuters on Thursday, citing US officials, stated that the negotiations between congressional leaders and President Biden advanced, adding that both parties merely need to agree on $70 billion in spending. Biden and McCarthy are near the deal that would raise the debt ceiling for two years and cap spending on most items other than military and veterans, the report added.

On the British Pound side of the equation, hot UK inflation data did offer some temporary respite to Cable but it faded amid the debt-deal anxiety and unimpressive testimonies from Bank of England (BoE) Governor Andrew Bailey and his colleagues before the UK Parliament’s Treasury Select Committee (TSC) earlier this week. According to the latest data published by the UK Office for National Statistics (ONS) on Wednesday, the United Kingdom’s annual Consumer Price Index (CPI) rose by 8.7% in April against the 10.1% jump recorded in March. The market consensus was for an 8.2% increase. The Core CPI gauge (which excludes volatile food and energy items) increased by 6.8% YoY in the same period, compared with a 6.2% rise seen in March while beating expectations of a 6.2% growth.

Friday’s mixed Retail Sales report from the United Kingdom also failed to have any positive impact on the Pound Sterling. The Retail Sales rose 0.5% over the month in April vs. 0.3% expected and -1.2% previous. The Core Retail Sales, stripping the auto motor fuel sales, increased 0.8% MoM vs. 0.3% expected and -1.4% previous. The annual UK Retail Sales declined by 3.0% in April versus -2.8% expected and March’s -3.9% figure while the Core Retail Sales decreased by 2.6% in the reported month versus -2.8% expectations and -4.0% previous.

After the US Bureau of Economic Analysis announced on Friday that the annual Core Personal Consumption Expenditures (PCE) Price Index, the Fed's preferred gauge of inflation, edged higher to 4.7% in April, the USD gathered strength against its rivals and caused GBP/USD to erase a large portion of its recovery gains ahead of the weekend.

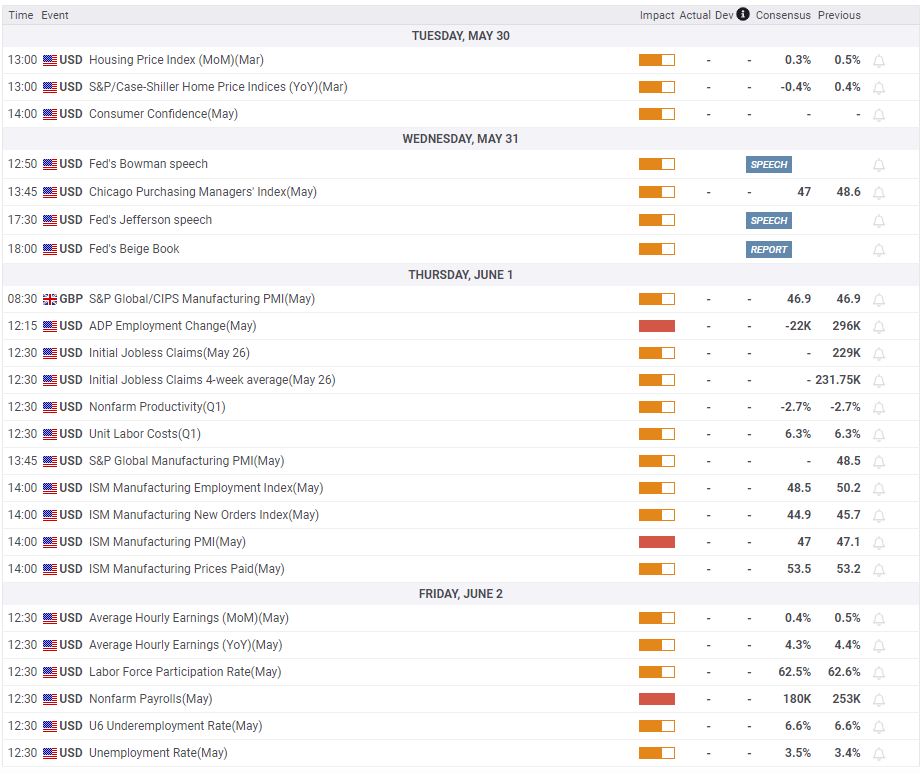

Week ahead: US Nonfarm Payrolls data stands out

With the key inflation reports from both sides of the Atlantic now out of the way, the employment data from the United States is likely to grab the eyeballs in the week ahead. The economic calendar from the United Kingdom is devoid of any top-tier data releases in the holiday-shortened week.

On Monday, the UK and US markets will be closed, in observance of Whit Monday and Memorial Day respectively, leaving minimal volatility and thin volumes.

The US Conference Board Consumer Confidence data will drop on Tuesday, the only relevant data publication for Cable traders. Therefore, they will look forward to China’s official Manufacturing and Non-Manufacturing PMI reports for a fresh take on the market sentiment, eventually impacting the risk currency, the Pound Sterling. Next of note is the JOLTS Job Openings data from the United States. A slew of speeches from the Federal Reserve policymakers will also keep GBP/USD traders on their toes on Wednesday.

The beginning of the next month on Thursday brings the final estimate of the UK Manufacturing PMI, which is unlikely to have any impact on the Pound Sterling. Across the pond, the US ADP Employment Change data and ISM Manufacturing PMI will be eagerly awaited alongside the weekly Jobless Claims data.

On the final trading of the week, the United States Nonfarm Payrolls report will stand out. The US economy added 253K jobs in April, above market expectations of 179K while wages grew the most in nine months. Strong wage inflation data helped push back markets' expectations for Fed rate cuts later this year.

Meanwhile, all eyes will be on US debt ceiling talks, as default fears ramp up ahead of the June 1 deadline. President Biden is hoping to reach a debt limit deal that would push the next deadline out past the 2024 presidential election. McCarthy said Wednesday that policymakers could get a debt agreement in principle this weekend.

GBP/USD: Technical outlook

From a short-term technical perspective, GBP/USD remains exposed to more downside risks, as the 14-day Relative Strength Index (RSI) still holds comfortably below the midline.

The pair extended its correction and gathered downside traction following a sustained break below the critical upward-sloping 50-Day Moving Average (DMA), now at 1.2435.

Pound Sterling bears now need a daily closing below the mildly bullish 100 DMA support at 1.2287 to unleash further declines. The next relevant cushion is envisioned at the March 24 low at 1.2190. Additional declines will call for a test of the 1.2000 psychological level.

Alternatively, Pound Sterling buyers could stage a decent comeback toward the above-mentioned 50 DMA support-turned-resistance at 1.2435 should the 100 DMA support guard the downside.

Ahead of that, the 1.2400 level could challenge the bearish commitments on the road to recovery. Recapturing the 50 DMA barrier is critical to resuming the previous uptrend toward the downward-sloping 21 DMA at 1.2493.

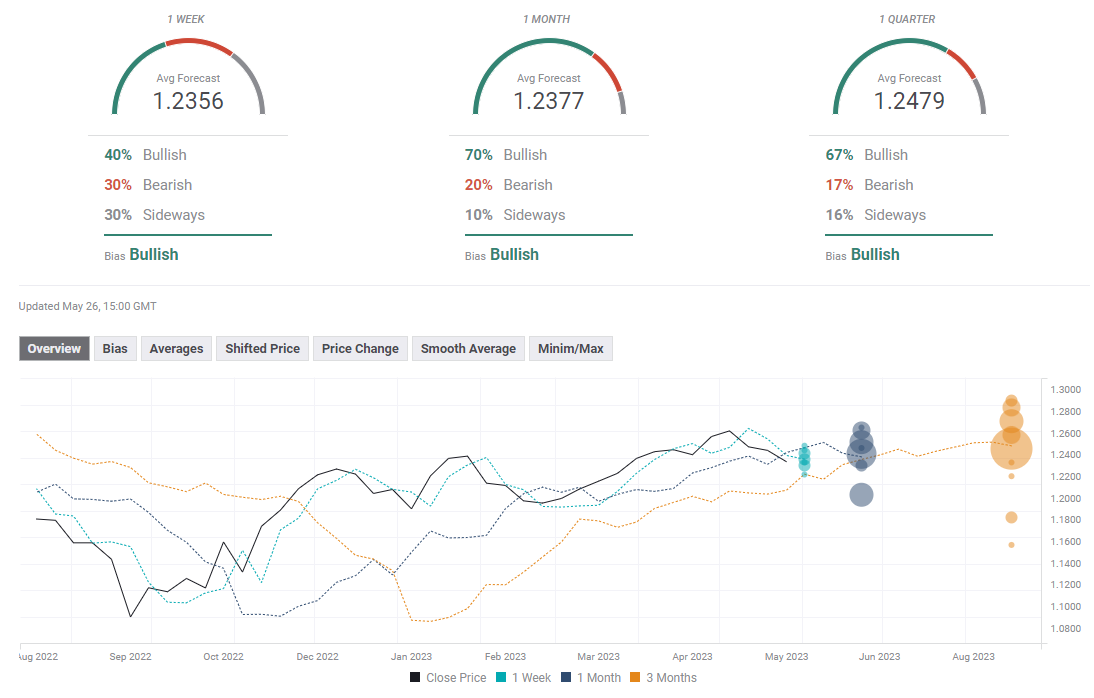

GBP/USD: Forecast Poll

Although FXStreet Forecast Poll's outlook suggests that GBP/USD could have a hard time finding direction in the near term, the one-month and one-quarter outlooks both paint a bullish picture.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.