![]() Mario Blascak, PhD

Mario Blascak, PhD

Independent Analyst

- The UK parliament is expected to vote for the second time on Brexit deal. Deeply divided parliament is expected to reject it again should the UK Prime Minister Theresa May fail to deliver any amendments on the troubled issue of the backstop.

- The Federal Reserve Chairman Jerome Powell is set to testify in the US Congress on the economy and monetary policy.

- The US Dollar strength stemming from growth and yield differentials and a persistent Brexit stalemate is expected to weigh on Sterling in the upcoming week.

- The break of the confluence of 200-DMA and the Fibonacci level is likely to see Sterling falling towards 1.2770.

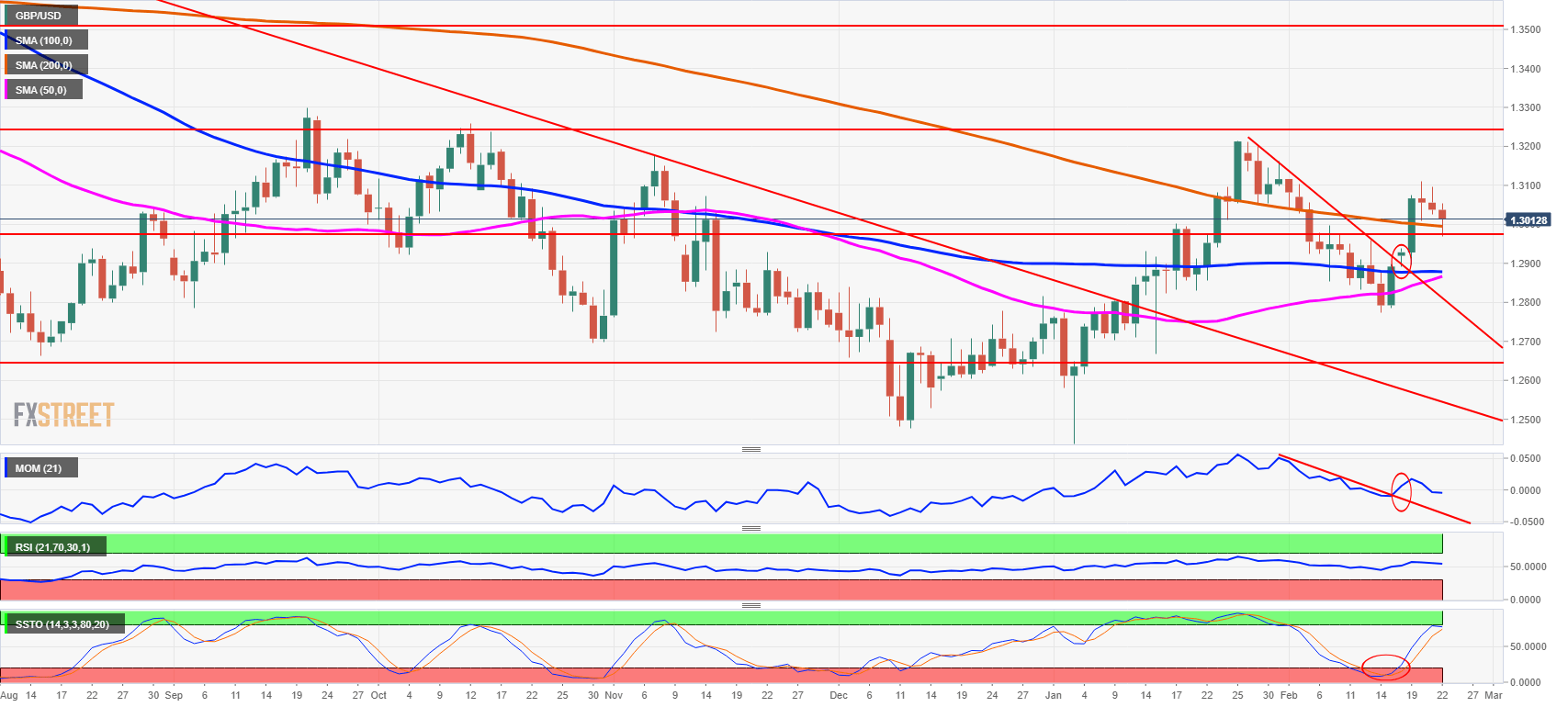

The GBP/USD is trading on the downside at around 1.2970 on Friday, falling past key support level of 200-days moving average (DMA) at 1.2996 ahead of key Brexit and the US economic events. While the UK House of Commons is deeply divided and it is not expected to pass the Brexit deal if potentially voting on it next week, the US economy is expected to yield another streak of solid economic data headlined by the Federal Reserve Chairman Jerome Powell’s Congressional testimony.

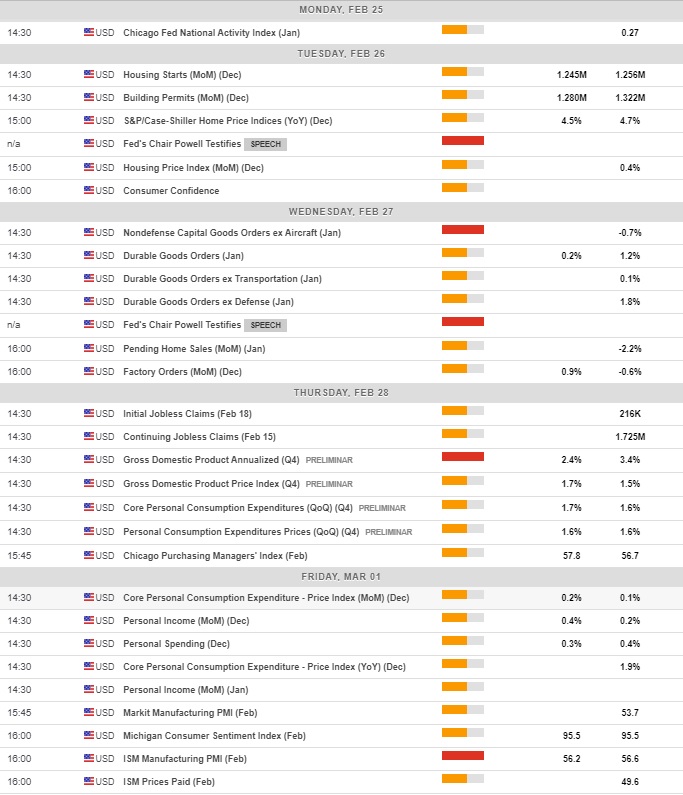

The economic events scheduled for the week ahead are expected to see the US fourth-quarter GDP rising by 2.4% quarterly annualized rate with the Federal Reserve Chairman Powell expected to confirm the strength of the US economy and central bank’s patience in the further monetary policy outlook.

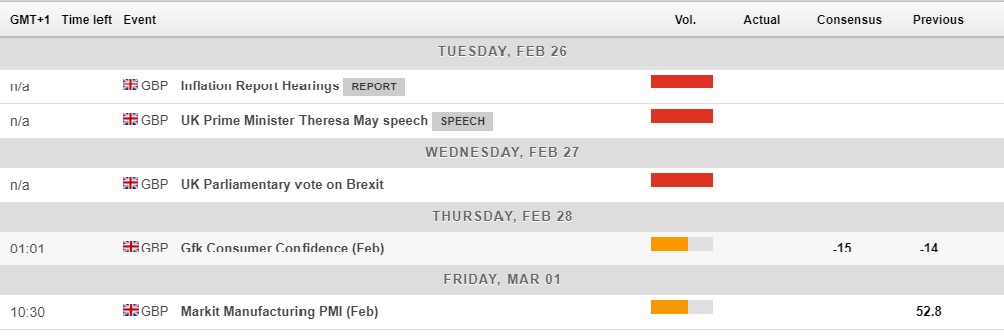

In the UK, apart from the Inflation report parliamentary hearing scheduled for Tuesday, the House of Commons voting on withdrawal agreement is playing a key role after the UK Prime Minister Theresa May managed to agree with the European Commission’s President Jean-Claude Juncker on the backstop adjustment before the European Council summit on March 20-21.

Technically the GBP/USD broke away from the downtrend and rose as high as 1.3107 on Wednesday, but the currency pair was unable to withstand the sideways trend within 1.3000-1.3100 range and fell past the key 200-DMA on Friday attacking 1.2970 representing 38.2% Fibonacci retracement of a long-term uptrend from 1.2110 to 1.4370.

The break of the GBP/USD on the upside was supported by solid UK labor market report for January that saw the UK unemployment dwelling at the lowest level since February 1975 of 4.0% while the pay increases reached 3.4% both including and excluding bonuses.

The UK January labor market report confirmed the prediction from the Bank of England that repeatedly pointed out that the UK labor market tightness is the main determinant of future inflation pressures in the UK.

"While most surveys of employment intentions softened a little in Q4, consistent with a slight slowing in employment growth in early 2019, labor market conditions are projected to remain tight, and unemployment is expected to be broadly stable in the near term,” the Bank of England wrote in its February Inflation Report on February 4.

The UK total pay growth rate ending until December 2018

The confluence of a Fibonacci retracement line at 1.2975 and a 200-DMA serves as a strong support area for GBP/USD that broke away from the downtrend on hopes for delayed Brexit.

With the UK political scene deeply divided on Brexit deal and seemingly unable to reach a consensus on generally hated issue of the Irish border backstop, the EU officials confirmed that they expect Theresa May to request an extension of Article 50 that pushes back Brexit by months.

While delayed Brexit is GBP/USD supportive, the question is if the UK Prime Minister Theresa May will be able to deliver the proposal agreed with the EU to remove or modify the backstop conditions and have this ratified by the House of Commons. And this is still rather unlikely to materialize over the course of next week.

The last week of February will formally be the last one to strike the deal between the US and China before the March 1 deadline, but the extension of current truce might follow. The risk-off market sentiment resulting from the disorderly end of the trade talks would favor the US Dollar as a safe-haven currency.

Related reading

Summary of Fed policymakers remarks in the third week of February

Cleveland Federal Reserve President and the non-voting member of the rate-setting FOMC Loretta Mester said on February 19:

- Fed funds rate may need to move “a bit higher” if the economy performs as she expects.

- The most likely scenario is that the economic growth will slow this year, job growth will slow, and inflation will stay near 2%.

- Fed is not far behind or ahead of the curve and can gather information on the economy before adjusting rate policy.

- I would be comfortable slowing or stopping reinvestment of maturing securities this year.

- If I were to make the decision on my own, I would favor slowing reinvestment of Fed's maturing securities.

- My preference is for Fed to hold primarily treasuries and I would favor shorter term treasuries.

- The rate increase may be needed later this year.

- I do not think ending balance sheet trimming would have a material impact on the economy.

New York Fed President John Williams said on February 19 for Reuters:

- I am comfortable with the interest rates level now, and I see no need to raise them again unless growth or inflation shifts to an unexpectedly higher gear.

- The Fed would continue trimming its bond portfolio well into next year.

San Francisco Federal Reserve President and the non-voting member of the rate-setting FOMC Mary Daly said on February 20:

- I see more headwinds, including slower global growth, uncertainty, and tighter financial conditions.

- There's nothing on the radar that says that the US is slipping into the recession.

- Impact of uncertainty is pretty substantial, but it can slow the economy.

- We are very near a neutral level of rates.

- The US economy is restraining itself and faces headwinds, so Fed needs patience on rates.

- Patience on rates is needed until inflation is rising faster.

St. Louis Federal Reserve President and the non-voting member of the rate-setting FOMC James Bullard said on February 21 on CNBC:

- Fed is in a good place today.

- I think rates are a bit tight right now and the December rate hike was a "step too far."

- I would like to see inflation numbers improve.

- Political factors not involved in FED decisions.

- Fed is likely near the end of interest rate increases and program to reduce bonds it holds on its balance sheet.

- Growth is slowing in China, and it will continue to slow.

- China has a longer-term issue of an aging population.

- The probability of recession in the US has picked up because the yield curve has nearly inverted.

- The US economy is slowing although not terribly and it needs productivity growth.

Atlanta Federal Reserve President Raphael Bostic and the non-voting members of the rate-setting FOMC said in Dublin on February 21:

- Fed is close to neutral policy rate right now.

- The US economy is pretty good; inflation is not much faster.

- It is imprudent to project policy path given the uncertainty.

Atlanta Federal Reserve President Raphael Bostic and the non-voting members of the rate-setting FOMC said at the Monetary Policy Forum in New York on February 22:

- Monetary policy is near the end of an entire arc.

New York Federal Reserve President John Williams and the permanent voting member of the rate-setting FOMC said on February 22:

- New inflation dynamics mean the Fed can safely "look through" transitory inflations shock.

- I say we must ensure inflation does not get anchored below the target.

- We must remain vigilant about the possible inflation surge.

- Traditional trade-offs between employment and inflation and "alive and kicking".

San Francisco Federal Reserve President and the non-voting member of the rate-setting FOMC Mary Daly said on February 22:

- I do not believe Phillips curve is dead.

- Complacency can go both ways on upside and downside inflation risks.

- Inflation expectations matter more now than they used to.

- It is important to not be complacent but also not to be overly worried about inflation.

- Wage growth is not having much effect on price inflation.

- There are few signs that wage inflation is running away

- The decline of the employer-provided cost of living adjustments weakens the link between wage, price growth.

The Federal Reserve’s Monetary Policy report said on February 22:

- Timing and size of future adjustments to the Fed funds rate will depend on incoming data.

- Softer conditions late in the year and muted inflation warranted patient approach to further rate increases.

- Partial US government shutdown likely held down GDP growth in first quarter 2019 “somewhat,” largely due to lost work of federal workers and contractors.

- Consumer spending, business investment appear to have weakened near the end of last year.

- Hourly compensation has “stepped up” since June 2018 but growth rates remain moderate by historical standards.

- The financial system remains 'substantially more resilient' than before financial crisis but notes 'high' debt of businesses and some deterioration of credit standards in the second half of 2018.

- Potential downside risks to international financial stability include 'political and policy uncertainty' and “intensification of trade tensions”.

- Longer-run size of the Fed balance sheet will be “considerably large”' than before the financial crisis.

Technical analysis

GBP/USD daily chart

Technically the GBP/USD broke away from the downward sloping trend that saw the currency pair fall as low as 1.2770 last week and now it dwells at the confluence area formed by the 200-day moving average of 1.2995 and a 38.2% Fibonacci retracement level of 1.2975.

The third week of February saw GBP/USD jump up to a range of 1.3000-1.3100, with the currency pair ending the week on the weaker side of the range.

With the GBP/USD trading at around 1.300, just above a 200-day moving average (DMA) of 1.2995, further move on the upside is limited by 1.3100. The support for GBP/USD is at around 1.2975 representing 38.2% Fibonacci retracement of a long-term uptrend from 1.2110 to 1.4370.

After the week of trading above the 1.3000 level, the Slow Stochastics moved all the way up from the Oversold to the Overbought territory, ready to make a bearish crossover. The reversal of the Relative Strength Index to the upside is also losing steam. The break of the confluence of 200-DMA and the Fibonacci level is likely to see Sterling falling towards 1.2770 once again.

The week ahead in economic events

UK economic calendar February 25-March 1

US economic calendar February 25-March 1

FXStreet Forecast Poll

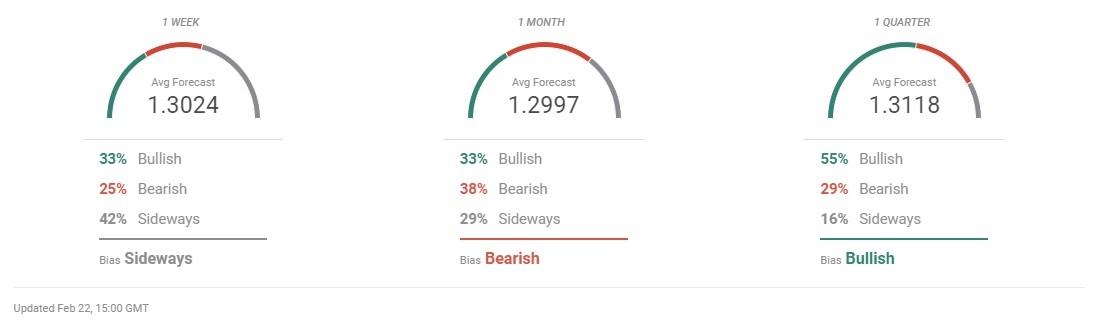

The FXStreet Forecast Poll i is expecting Sterling to move sideways to 1.3024, up from 1.2766 last week and up from 1.2995 prediction two weeks ago. The forecast is highly uncertain with the bullish-to-bearish ratio at 33%-25% and the majority of 42% predicting sideways trend.

For 1-month ahead, the forecast is bearish predicting 1.2997, up from 1.2864 FX rate predicted last week and 1.2929 predicted two weeks ago. Bullish-to-bearish forecast is evenly spored to 33%-38% and 29% of sideways predictions, down from 56%-35% distribution last week.

The vast majority of the forecasters in the FXStreet Forecast Poll i is bullish over the 3-months horizon with GBP/USD prediction almost unchanged from last week at 1.3118 with 55%-29% of bullish-to bearish forecasts, down from 72%-20% last week.

Note: All information on this page is subject to change. The use of this website constitutes acceptance of our user agreement. Please read our privacy policy and legal disclaimer. Opinions expressed at FXstreet.com are those of the individual authors and do not necessarily represent the opinion of FXstreet.com or its management. Risk Disclosure: Trading foreign exchange on margin carries a high level of risk, and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to invest in foreign exchange you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss of some or all of your initial investment and therefore you should not invest money that you cannot afford to lose. You should be aware of all the risks associated with foreign exchange trading, and seek advice from an independent financial advisor if you have any doubts.

Recommended Content

Editors’ Picks

EUR/USD extends recovery beyond 1.0400 amid Wall Street's turnaround

EUR/USD extends its recovery beyond 1.0400, helped by the better performance of Wall Street and softer-than-anticipated United States PCE inflation. Profit-taking ahead of the winter holidays also takes its toll.

GBP/USD nears 1.2600 on renewed USD weakness

GBP/USD extends its rebound from multi-month lows and approaches 1.2600. The US Dollar stays on the back foot after softer-than-expected PCE inflation data, helping the pair edge higher. Nevertheless, GBP/USD remains on track to end the week in negative territory.

Gold rises above $2,620 as US yields edge lower

Gold extends its daily rebound and trades above $2,620 on Friday. The benchmark 10-year US Treasury bond yield declines toward 4.5% following the PCE inflation data for November, helping XAU/USD stretch higher in the American session.

Bitcoin crashes to $96,000, altcoins bleed: Top trades for sidelined buyers

Bitcoin (BTC) slipped under the $100,000 milestone and touched the $96,000 level briefly on Friday, a sharp decline that has also hit hard prices of other altcoins and particularly meme coins.

Bank of England stays on hold, but a dovish front is building

Bank of England rates were maintained at 4.75% today, in line with expectations. However, the 6-3 vote split sent a moderately dovish signal to markets, prompting some dovish repricing and a weaker pound. We remain more dovish than market pricing for 2025.

Best Forex Brokers with Low Spreads

VERIFIED Low spreads are crucial for reducing trading costs. Explore top Forex brokers offering competitive spreads and high leverage. Compare options for EUR/USD, GBP/USD, USD/JPY, and Gold.