GBP/USD outlook: Near-term structure weakens after a double failure at 1.1500 barrier

GBP/USD

Cable remains in red for the second day, pressured by weaker risk sentiment and downbeat report from the BoE, which showed raised expectations for inflation in one year time to 9.5% from 8.4% estimation in August and expectations for 4.8% inflation in three years.

Inflation in UK eased to 9.9% in September from 10.1% in August, but still about five times above the central bank’s 2% target.

BoE remains on track for further rate hikes to in fight to bring red-hot inflation under control, though high borrowing cost would further hurt already weakened economic growth.

Overall negative near-term picture could be partially offset by better than expected UK PMI data which showed unexpected increase of activity in construction sector, sending the index to three-month high.

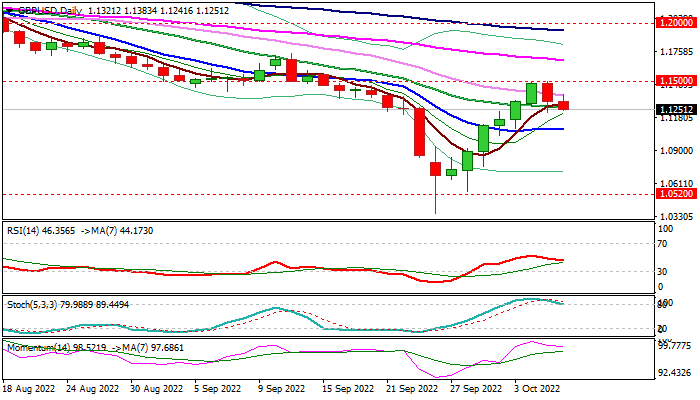

Daily studies show near-term structure weakening, following a pullback after repeated reject at round-figure 1.15 resistance, as negative momentum is rising and stochastic emerging from overbought territory. Fresh bears tested initial support at 1.1225 (Fibo 23.6% of 1.0348/1.1495 recovery leg), but need break here to further weaken near-term structure and open way for attack at key supports at 1.1082/1.1057 (10DMA/Fibo 38.2%) and psychological 1.10 level, to generate stronger reversal signal on break. Falling 30DMA offers immediate resistance at 1.1373, guarding the upper pivot at 1.1500, violation of which would bring bulls back to play.

Res: 1.1373; 1.1410; 1.1460; 1.1500.

Sup: 1.1225; 1.1082; 1.1057; 1.1000.

Interested in GBP/USD technicals? Check out the key levels

Author

Slobodan Drvenica

Windsor Brokers

Industry veteran with over 22 years’ experience, Slobodan Drvenica joined Windsor Brokers in 1995 when he was an active trader for more than 10 years, managing the trading desk and own account departments.