GBP/USD Annual Price Forecast: Policy and protectionism to pound Pound Sterling in 2025?

- GBP/USD faltered on its recovery from a four-decade low as sellers returned in the last quarter of 2024.

- Divergent Fed-BoE policy expectations and Trump’s protectionism could encourage the US Dollar in 2025.

- The UK economic pain is set to remain a drag on the Pound Sterling in 2025.

- Technically, GBP/USD remains a “sell-the-bounce” trade for 2025.

Unlike several unknowns looming at the onset of 2024, the Pound Sterling (GBP) gears up for the global implications of US President-elect Donald Trump’s protectionist policies and the path of monetary policies adopted on both sides of the Atlantic as 2025 unfolds. Meanwhile, the US Dollar (USD) holds an edge due to the US-UK macroeconomic divergence and its safe-haven status as markets stay vigilant over unprecedented geopolitical tensions that have emerged as key risks across the financial markets since 2022.

Reviewing the GBP/USD 2024 journey, the Pound Sterling failed to sustain the turnaround against the USD from a four-decade low of 1.0339 set in September 2022. The US Dollar staged a strong comeback in the final quarter, triggering a steep correction in the pair from 30-month highs of 1.3434 to settle roughly 1% lower in the year.

GBP/USD Weekly chart for 2024. Source: FXStreet

The monetary policy divergence between the US Federal Reserve (Fed) and the Bank of England’s (BoE) aided the GBP/USD recovery for most of the year, only to give into Trump’s tariff threats, Fed’s hawkish tilt and the UK’s economic underperformance in the quarter to December.

Key factors behind Pound Sterling's two-way business in 2024

The following factors drove the GBP/USD price action this past year, making it interesting for investors.

UK and US disinflationary trends

In 2023, UK inflation proved more persistent than that of other major economies, including the US. However, the scenario reversed in 2024 as the US's progress in disinflation stalled heading into the new year.

The US Consumer Price Index (CPI) inflation rate slowed for much of this year, falling to 2.4% year-on-year (YoY) in September before resuming its uptrend in recent months. The CPI rose 2.7% last month relative to November 2023, up from 2.6% in October.

Meanwhile, the core Personal Consumption Expenditures (PCE) Price Index rose at an annual pace of 2.8%, at the same pace at the beginning of this year in January. This is the Fed’s preferred inflation measure as base effects do not distort it and provides a clear view of the underlying trend of consumer behavior by excluding volatile items.

The UK CPI inflation rate slowed to 2.6% YoY in November from 4.0% in January, ranging close to the BoE’s 2.0% target hit in May and June. Meanwhile, UK Services inflation eased to about 5%, falling below that key level in September for the first time since May 2022. The BoE uses inflation in the services sector as a key input to gauge the level of inflation in the economy.

In its December policy statement, the BoE said the increase in UK headline inflation in November to 2.6% was slightly higher than previously expected, adding that services inflation remained “elevated.”

Goldman Sachs Research sees domestic inflationary pressures falling back next year. The US investment banking giant noted that “continued easing in labour market tightness – together with reduced catch-up effects now that inflation has returned close to target – are likely to result in a notable slowing in pay growth next year.”

Fed and BoE policy pivots

Witnessing a bumpy ride in the disinflationary trend and considering economic growth prospects, the Fed and the BoE finally adopted dovish policy pivots in the second half of the year.

In August, the BoE cut interest rates for the first time since the start of the COVID-19 pandemic, lowering borrowing costs by 25 basis points (bps) to 5.0% from a 16-year high of 5.25%. Governor Andrew clarified that the central bank would move cautiously with rate cuts going forward. The BoE paused in September and delivered another 25 bps rate cut to 4.75% in November, reflecting the continued progress in disinflation. However, the BoE policymakers wrapped up the year with a decision to leave rates unchanged at 4.75% in its December meeting after UK inflation climbed to an eight-month high.

Across the Atlantic, the Fed trumped the UK central bank’s move and cut the fed funds rate by 50 bps to the 4.75%-5.00% range in September, its first reduction in four years. After September’s large rate cut, a 25 bps reduction followed in each of the two remaining Fed meetings of 2024, bringing the policy rate to 4.25%-4.50 by the end of the year. The US central bank’s less dovish shift in the tone of the policy statement in December prompted markets to predict fewer rate cuts next year.

UK and US national elections

The GBP/USD recovery received a much-needed impetus from the Labour Party's historic win in the UK parliamentary election in July. The Labour Party secured a decisive majority in the 650-seat parliament, defeating the Conservative Party led by Rishi Sunak. The Pound Sterling capitalized on expectations that the incoming government would provide a period of economic stability after an often tumultuous 14 years of Conservative Party rule.

However, the upbeat momentum lost traction as the pair peaked near 1.3400 in September. A correction ensued as the market's attention turned to the November 5 US Presidential election. The US Dollar jumped back into the game, anticipating a victory for Republican nominee Donald Trump. Trump’s fiscal and trade policies are seen as inflationary, calling for higher interest rates and a stronger US Dollar.

Donald Trump emerged victorious in the 2024 election and made a remarkable comeback, securing more than the 270 Electoral College votes needed to win the presidency. The Greenback rode the wave of ‘Trump trade’ optimism, knocking GBP/USD to its lowest level in six months at 1.2488 before recovering to near the 1.2700 region.

GBP/USD key drivers for 2025: Trump wild card comes in

US and UK economic outlooks

Contrasting economic outlooks on both sides of the Atlantic will likely cause the Fed and BoE policy divergence to stand out in the year ahead. The US economy continued to show resilience, with the real Gross Domestic Product (GDP) expanding at a solid 2.8% annualized rate in the third quarter (Q3) of 2024, slowing slightly from a 3.0% increase in Q2.

The economy shrugged off the lag effects of elevated interest rates and long-standing worries over the widening budget deficit of more than $1.8 billion in fiscal 2024, helped by robust consumer spending. Another major factor for growth was federal government spending, which exploded higher by 9.7%, pushed by a 14.9% surge in defense outlays, per CNBC News.

In fact, the Atlanta Fed's GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2024 is running at 3.1%. Additionally, the Fed raised its median YoY real GDP forecast for Q4 2025 slightly to 2.1% in December from 2.0% projected in September.

On the other hand, the British economy showed no growth in Q3, missing the 0.1% growth expected by economists and having expanded 0.4% in the year's second quarter.

Suren Thiru, Economics Director at the Institute of Chartered Accountants in England and Wales, commented: "these figures suggest that the economy went off the boil even before the budget, as weaker business and consumer confidence helped weaken output across the third quarter, particularly in September.”

Meanwhile, the BoE staff downgraded their economic forecast for the fourth quarter of 2024, now predicting no growth, compared with the 0.3% expansion predicted in its November report.

The latest projections from the Office for Budget Responsibility (OBR) showed a GDP growth of 2.0% next year, compared with the OBR's previous expectations for growth of 1.9%. The OBR projections were published after the UK Chancellor Rachel Reeves revealed a slew of expected tax rises to the tune of £40bn in the Labour government’s first Autumn Budget in 15 years at the beginning of the fourth quarter.

Goldman Sachs and KPMG economists forecast the UK’s GDP to increase by 1.2% in 2025, slower than the BoE’s projection of 1.5%. Meanwhile, Senior Economist at S&P Global, Marion Amiot, sees the UK economy expanding by 1.5% next year. Geopolitical risks and the potential for trade frictions could outweigh the positive effects of a less restrictive monetary policy and a pick-up in consumption and business investment.

Fed and BoE interest rates trajectory

The perfect combination of strong growth and potential pick up in inflationary pressures endorses the Fed’s hawkish shift. Markets predict the growing labor market slack will likely be offset by higher prices from tariffs on goods and mass deportations of immigrants that Trump has promised next year.

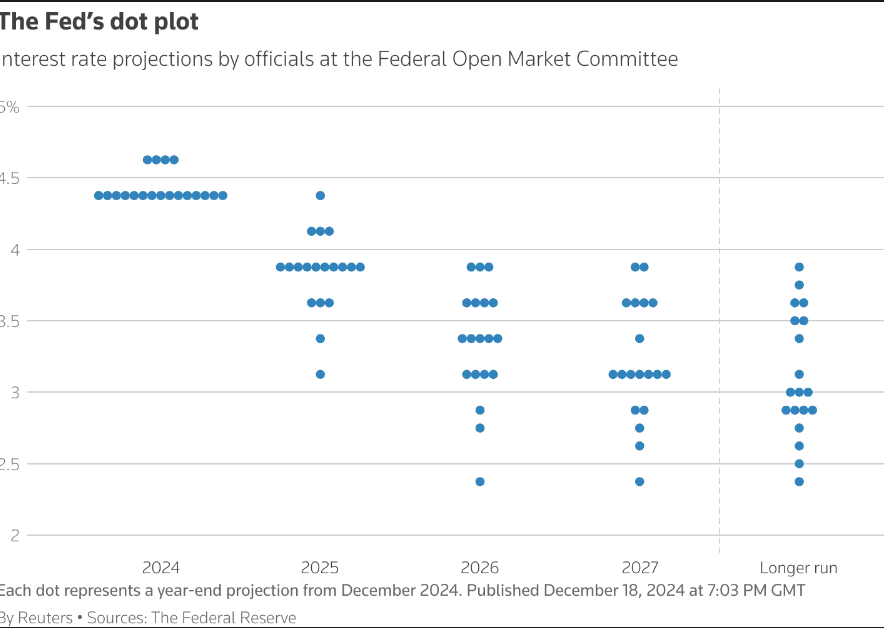

In its December Statement of Economic Projection (SEP), the so-called dot plot, the Fed projected inflation jumping from 2.2% in their prior projections to 2.5% for the first year of the new Trump administration.

Against that backdrop, Fed officials pencilled in half a percentage point in policy easing next year rather than the full percentage point officials anticipated as of September.

Source: Federal Reserve

Speaking at the press conference after the December meeting, Fed Chair Jerome Powell noted that progress on inflation is slower than hoped. “It’s been frustrating,” he said, adding that "from here, it's a new phase; we are going to be cautious about further cuts. It's appropriate to proceed cautiously.”.

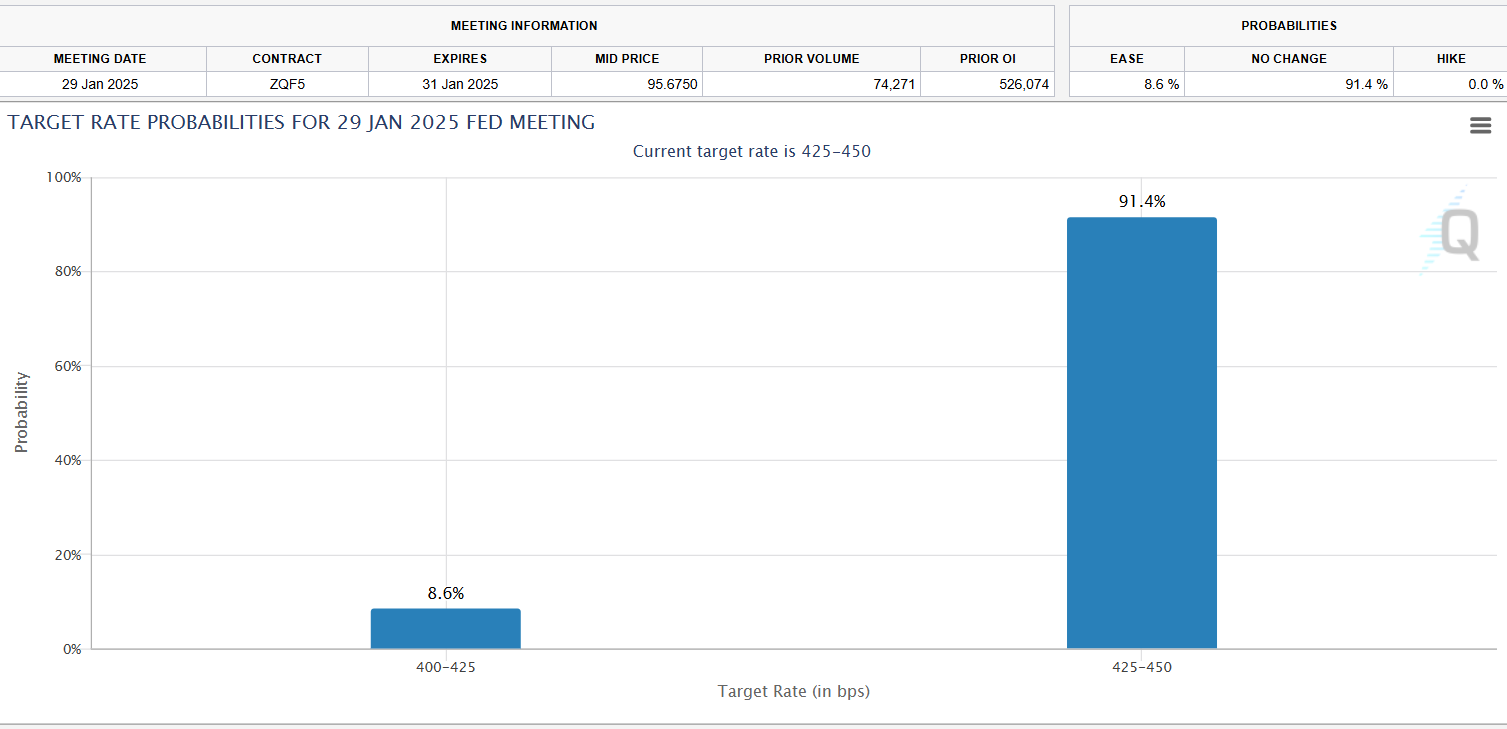

The probability that the Fed will pause its easing cycle in January stands at 91%, while that in March is at a coin’s flip level, according to CME Group’s FedWatch tool.

Fed interest-rate probabilities for the January meeting. Source: CMEGroup

On the other side, the BoE stood pat on its policy rate in December but “the split vote decision and the dovish tone of the Minutes suggest that a February (2025) interest rate cut remains very much in play, if not yet a done deal,” Thiru said.

In a dovish tilt, the voting composition was more divided than expected, with three members of the Monetary Policy Committee (MPC) voting to reduce rates, while six favoured a hold. Markets had expected only one member to vote for a cut.

The fragile economic situation in the UK appeared to be the primary reason behind the surprise dovish vote split.

BoE Governor Andrew Bailey said that “we think a gradual approach to future interest-rate cuts remains right. But with heightened uncertainty in the economy, we can’t commit to when or by how much we will cut rates in the coming year.”

“Investors took the vote split and Bailey’s comments as surprisingly dovish, adding to bets for reductions in 2025. Money-market pricing implied two quarter-point cuts and a strong chance of a third,” per Bloomberg.

Trump’s protectionism

During his election campaign, US President-elect Donald Trump unveiled plans to impose 20% tariffs on all imports to the US. On November 26, he pledged a 25% tariff on all products from Mexico and Canada from his first day in office and an additional 10% tariff on goods from China.

The incoming US Trade Representative Jamieson Greer announced the UK as a possible partner for a future free trade deal in return for potential changes to food standards and greater market access for US healthcare companies.

Greer said, “I recommend that the United States seek market access in non-Chinese markets in incremental, sectoral and bilateral agreements with other countries.” “Focusing on trading partners such as the United Kingdom, Kenya, the Philippines and India would be a good start,” he added.

Following Donald Trump’s victory in the US election, Rachel Reeves, the UK Chancellor, said she has plans to strike a free trade deal with the US to live up to her promise to boost economic growth.

In an ITV interview, Reeves said that “there's more than £300 bn of trade flows between the UK and the US every year, and we want to see that trade increase.”

That said, the impact of Trump’s tariffs on the UK is expected to be minimal. However, mounting tensions over a global tariff war and its spillover on the Euro area growth could sag confidence, having a rub-off effect on the British economy.

GBP/USD 2025 Technical outlook: Downside bias prevails

GBP/USD: One-month chart. Source: FXStreet

GBP/USD’s topping out its gradual recovery at two-and-a-half-year highs of 1.3434, and the ensuing downtrend carved out a rising wedge formation on the monthly time frame.

Confirmation of a rising wedge or a bearish wedge pattern generally indicates a reversal of the prior trend in the asset price.

The downside break of the nearly 18-month-old pattern materialized after the pair convincingly breached the lower boundary of the bearish wedge at 1.2682.

The 21-month Simple Moving Average (SMA) coincides with that support, making it a powerful one.

Adding to the bearish outlook, the Relative Strength Index (RSI) indicator broke below the 50 level in November, entering negative territory for the first time since March.

Pound Sterling buyers could find immediate support at the October 2023 low of 1.2037 if the downside bias gathers traction next year.

The next critical support aligns at the March 2023 low of 1.1802. A breach of that level could initiate a fresh downtrend toward the 1.1000 psychological level.

The 1.1500 static support could come to the GBP/USD rescue ahead of that cap.

On the flip side, strong resistance at around 1.2900 could threaten recovery attempts, where the 50-month SMA and the 100-month SMA close in.

Fresh buying opportunities will likely emerge above that level, providing extra legs to the turnaround toward the upper boundary of the pattern at 1.3490.

However, the bearish momentum could only be negated on a sustained move above the wedge resistance.

The next topside targets are the January 2022 high of 1.3749 and the June 2021 high of 1.4249.

To conclude, the path of least resistance appears to the downside for the GBP/USD pair amid bearish technical indicators and a lack of healthy support levels.

To conclude

The implications of incoming US President Donald Trump’s trade policies and mounting concerns over the UK economic slowdown will continue to act as a headwind for the GBP/USD in the year ahead.

The US and UK central banks’ policy mix will also play a pivotal role in the pair’s price direction as markets remain wary about unprecedented geopolitical risks in 2025.

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, also known as ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.