FX positioning: Where are the dollar longs?

The dollar’s appreciation in November still hasn’t emerged in CFTC FX positioning data that continues to show most G10 currencies’ net positions rising against USD. EUR positioning has slightly decreased but has not dipped into oversold territory, while GBP shorts have mounted. Still, there is no evidence that this is due to rising Brexit risk.

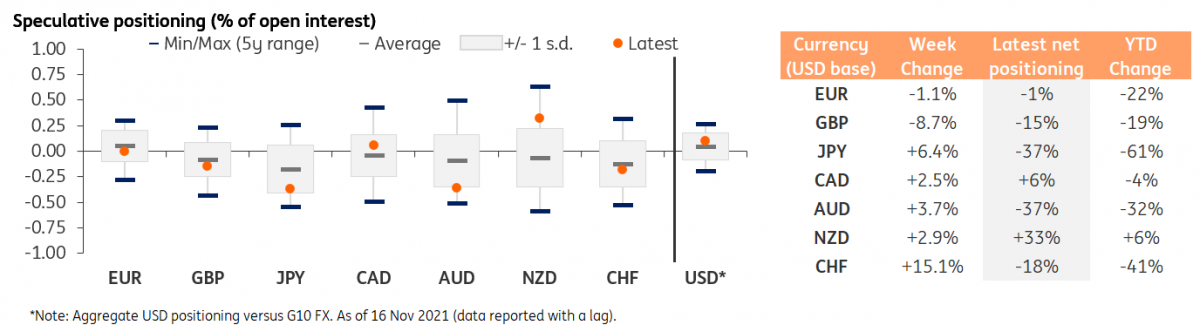

Strong dollar not emerging in positioning data

November has so far been a month dominated by a strengthening of the dollar across the board, but this has however not translated into a rise in USD net positioning as reported by the CFTC. USD net aggregate positioning versus reported G10 currencies (i.e. G9 excluding NOK and SEK) was unchanged in the last weeks of October and the first week of November, and then inched lower (now at +9.8% of open interest) in the week ending 16 November.

The surprise increase in USD net shorts was largely due to the jump in JPY, CAD and AUD net longs, which more than offset the slight decrease in EUR net positioning and the drop in GBP net positioning.

It is not uncommon to see CFTC FX positioning lag the moves in the spot market, and we can reasonably expect an increase in USD net-longs across the board in the next CFTC COT report.

Source: CFTC, Macrobond, ING

EUR positioning still neutral

Despite having moved from 1.15 to 1.13 in the week ending 16 November, EUR/USD positioning only decreased marginally (-1% of open interest) and did not move into oversold territory. This is another sign of dislocation between positioning and market dynamics, and we think we will see the EUR/USD positioning gauge move lower in the coming weeks. For now, it seems like the pair is not likely to receive much support from an overstretched short positioning in the near term.

In the rest of G10, GBP positioning fell (we discuss this in greater detail below), while all other G10 currencies rose in terms of net longs. Some short-squeezing in JPY seemed warranted by a drop in US 10y yields in early November, and also given how overstretched the yen’s net-short positioning was.

In the pro-cyclical space, AUD remains heavily oversold, and in sharp contrast with its closest peer NZD, with such divergence continuing to be fuelled by the very different monetary policy outlooks in Australia and New Zealand. The RBNZ is widely expected to hike rates again this week.

GBP shorts don’t seem Brexit-related

GBP positioning has continued to show quite elevated volatility, among the highest in G10. Net shorts increased by almost 9% of open interest in the week to 16 November, and reached -15% of open interest. Speculative positioning on the pound has dropped by around 25% of open interest in the past four weeks and, despite the tendency to show very wide swings, it seems to be signalling some worsening in market sentiment on the currency.

There is a chance that part of the market is growing increasingly concerned about a resurgence in Brexit risk, which has kept GBP positioning consistently in net-short territory in recent years. However, the lack of a risk premium being built into EUR/GBP (a key gauge of perceived Brexit risk by the market) strongly suggests the opposite: that investors have turned a blind eye on potential deterioration in EU-UK trade relationships. We discussed this in detail in “Brexit’s back”.

Read the original analysis: FX positioning: Where are the dollar longs?

Author

Francesco Pesole

ING Economic and Financial Analysis

Francesco is an FX Strategist and has been with the firm since May 2019. His main focus is on the G10 space and, in particular, commodity currencies. He began his career at Credit Agricole CIB and holds an MSc in Financial Markets and Investments