FX and US election cheat sheet

Two weeks until 5 November, and we are observing a growing shift in sentiment across financial and betting markets in favour of Donald Trump. The polls still point to a toss-up, but the risks remain skewed towards a stronger dollar and weaker risk-sensitive currencies as Trump hedges grow into the vote. FX implied volatility is also likely to rise.

The latest polls suggest the upcoming US election is a close call, but financial and betting markets have recently swung more in favour of a Donald Trump win. We will walk you through the numbers in key battleground states, discuss how we see market positioning in the two weeks leading to the election, and explore the potential initial reactions in FX.

The 2024 US swing states cheat sheet

-638652706021434887.png)

Polls averages and simulations from FiveThirtyEight (ABC News); betting odds from Kalshi and Betfair. Other sources: CNN, Associated Press, ING calculations

Battleground numbers

The table above summarises what polls and betting markets are telling us about the upcoming Presidential election for seven battlegrounds (or “swing”) states and the national outlook. According to the latest poll aggregates, 226 electoral college votes are either solidly or leaning Democrat, while 219 are for the Republicans. The seven battleground states listed are closely contested, with leads within the statistical margin of error. To reach the 270 electoral college win threshold, Harris needs to secure 44 of the 73 available swing state votes; Trump needs 51 – assuming all lock/lean states don’t flip.

Trump is marginally ahead in the swing states

If the latest poll averages (third column) prove correct, Trump wins the election with Republican lock/lean votes (219) + Arizona (11) + Georgia (16) + North Carolina (16) + Pennsylvania (19) = 281 electoral college votes. Harris would need to win all states where she is already ahead in the polls (including Michigan, Nevada and Wisconsin) plus another 13 electoral college votes from the swing states where Trump is currently leading. That means securing Arizona (11) alone wouldn’t be enough, and Harris would need to win either Georgia (16), North Carolina (16) or Pennsylvania (19), with the latter widely seen as the state that can tip the balance.

Polls versus bets

While there is no simple market measure of the Harris/Trump implied probability, betting markets are often taken as a benchmark. In the table above, we see that the traditional bookmaker (Betfair) odds highly favour Trump. We also looked at the CFTC-regulated portal Kalshi, where it is possible to buy/sell the equivalent of binary options on either candidate.

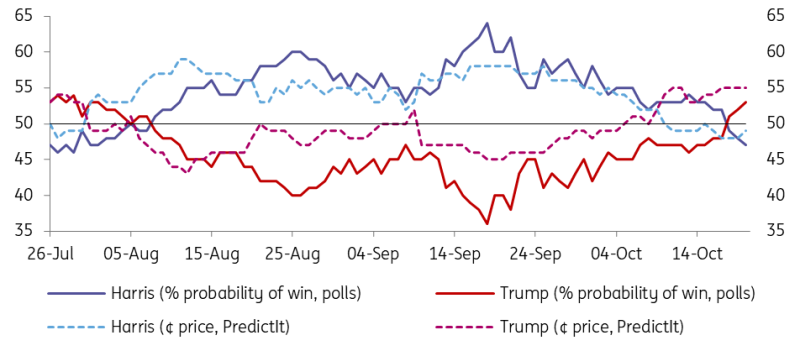

Betting markets have given Trump a better chance than the polls

Source: ING, FiveThirtyEight (ABC News), PredictIt

Kalshi’s election winner market only started in October, so the chart above uses data from PredictIt, an analogue election-betting website. Both Kalshi and PredictIt implied probability of a win has generally been leaning more in favour of Trump relative to what poll-based simulations were suggesting. Remember that these portals work similarly to stock markets, where the price is determined by buying and selling volume.

The rise in bets on Trump in such markets is probably a reflection of both polls and some hedging, considering a Trump win is seen as the more impactful event for markets. Incidentally, in both 2016 and 2020, the Republicans fared markedly better than polls and betting markets had anticipated, and that can also explain why betting markets have been favouring Trump this time.

FX implied volatility to rise into the vote

In the last two US presidential elections, the cost of FX hedging increased significantly in the two weeks leading up to the vote. One way to measure this is the ratio of one-month implied volatility to one-month historical volatility. A ratio above 1.0 suggests that markets anticipate larger spot movements in the upcoming month compared to the previous 30 days.

Rise in FX implied volatility may have only just started

Source: ING, Refinitiv

As you can see above, the implied/historical volatility ratio increased markedly in the 14 days preceding the 2020 and 2016 election days for G10 dollar crosses. We expect a similar dynamic this time, especially considering the latest polls are narrowly favouring Trump, whose win can generate larger volatility across the currency market. Since that hedging demand should mostly be related to protection for a Trump-led dollar rally, we think the balance of risks remains skewed to a stronger USD into the vote.

FX liquidity can dry up close to the vote

In particular, we remain concerned that some de-risking in the FX market can lead to poorer liquidity conditions. The Norwegian krone is often a good indicator of such conditions, given it is the least liquid G10 currency. Despite good fundamentals, we suspect EUR/NOK can trade back above 12.0 before the US election.

FX market isn't fully pricing in Trump

Since mid-October, markets have gradually priced in more Trump risk, mainly through higher US rates, pressure on emerging market currencies and some USD strength. This means that a potential “relief” rally following a Harris win can now be larger and hit the dollar harder.

That said, the FX market is not fully pricing in a Trump victory. The dollar’s strength is still mostly a function of stronger US data, and EUR/USD (currently at 1.082) is trading less than 1% below its short-term fair value. An undervaluation of at least 2% (the 1.5 standard deviation) would be needed to conclude there is a Trump-related risk premium embedded in the pair.

EUR/USD is not embedding a Trump risk premium

Over the recent period, EM currencies have sold off on the strong dollar but have not – yet – substantially underperformed G10 currencies. This may change. Most vulnerable could be CEE currencies, which have double exposure through EUR crosses and large export openness, translating into sensitivity to potential changes in global trade in the case of a Trump victory.

At the moment, HUF seems the most exposed within the region where the central bank does not have many options to defend the currency and the market has already outpriced any rate cuts over the last two weeks. On the other hand, the CZK and PLN seem more defensive and may also benefit from a possible relief in case of a Harris victory.

Elsewhere, things could have been worse for the Latin and Asian currencies were it not for recent Chinese stimulus measures. Yet both blocs still look vulnerable to further losses under a full Trump 2.0.

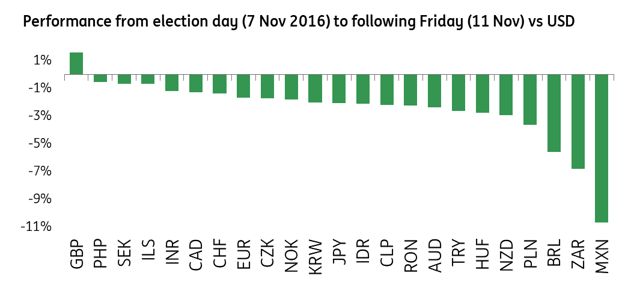

FX market reaction to Trump's 2016 win

Source: ING, Refinitiv

Gauging the initial FX impact

The 2020 Presidential election was somewhat unique, and results were significantly delayed due to the very high number of mail-in ballots and the Republicans contesting the count in some states. In the table at the top of this article, we summarised the point at which the key swing states were called by the Associated Press in the past three elections. It’s worth noting that Biden’s win was not officially called until the Saturday after the vote (so four days after).

There is probably a greater risk of a delay in the count and official results for this election compared to any other election before 2020, and news agencies may well be more careful in calling a state or the Presidency than in previous instances. Most swing states are on the East Coast, where polls close between 7PM and 8PM ET, but the high volume of mail-in ballots can cause delays. The preliminary results in Pennsylvania can have one of the deepest market impacts as this is seen as a must-win state for Harris, but local regulation allows mail-in votes to be counted only on Election Day, which can lead to a lengthy count.

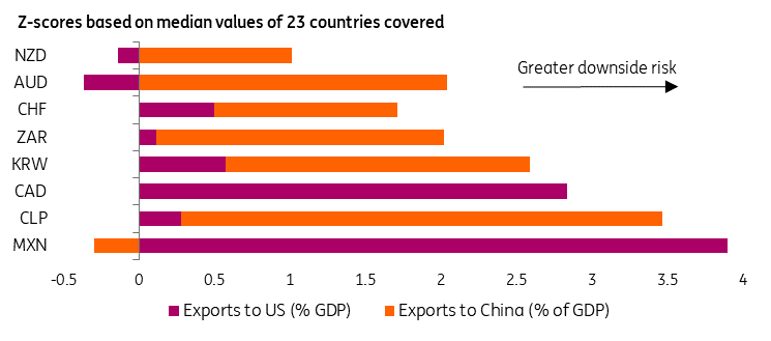

Anyway, there is a good possibility the FX market will “call” the winner already on the night between 5 November and 6 November. We expect the initial reaction to mostly entail protectionism-related trades. This means the wider swings can be seen in AUD and NZD in the G10 space; in EM, Asian currencies and MXN will be particularly sensitive.

Which currencies are most exposed to Trump tariffs?

Source: ING, IMF, Macrobond

Read the original analysis: FX and US election cheat sheet

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.