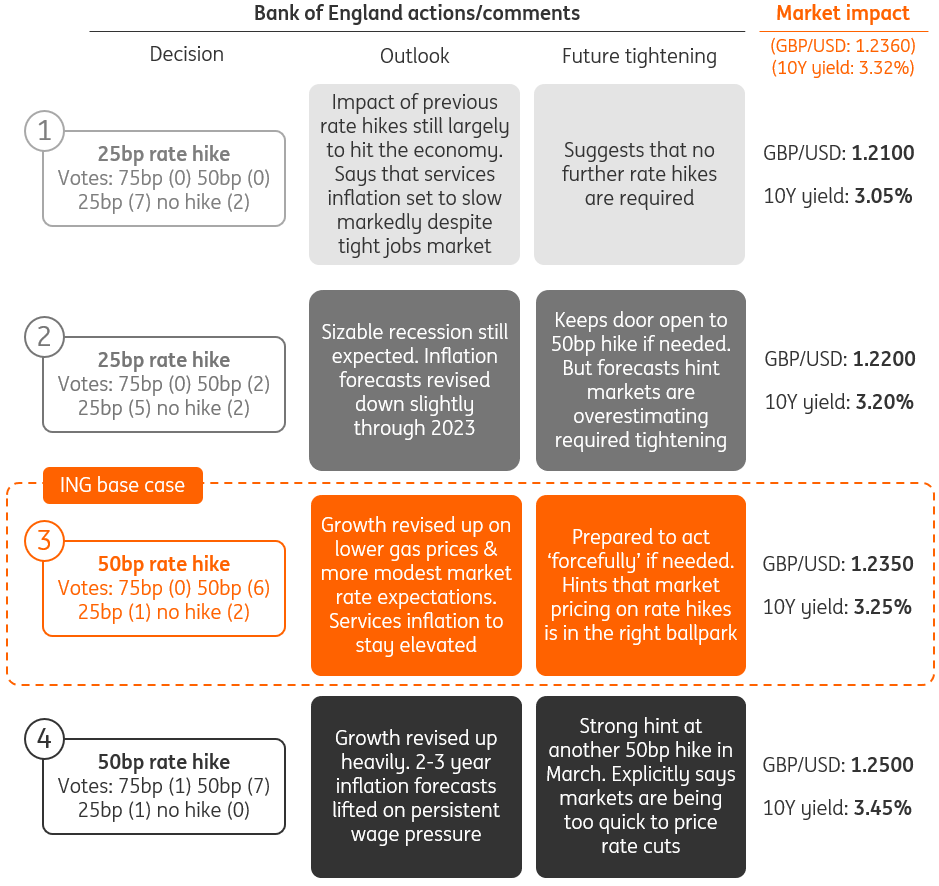

Four Bank of England scenarios for February’s meeting

Persistently high wage and service-sector price inflation points to another 50bp rate hike from the Bank of England next Thursday. If we're right, then we expect one final 25bp rate hike in March, marking the top of this tightening cycle.

Four scenarios for the Bank of England meeting

Source: ING

Market pricing based on spot values on 27 January

The Bank of England looks more likely to follow the European Central Bank than the Federal Reserve next Thursday, and we expect a 50 basis point rate hike for the second consecutive meeting. While the minutes of the December meeting appeared to open the door to a potential downshift to a 25bp move in February – and this meeting looks like a closer call than markets are pricing – the reality is that the recent data has looked relatively hawkish.

Wage growth is persistently high, looking both at the official numbers and the BoE’s own business surveys. Headline inflation came in a little lower than the Bank projected back in November, but services CPI – seen as a better gauge of domestically-driven inflation – has come in above expectations.

Still, if we get a 50bp hike on Thursday then it’s likely to be the last. BoE officials have hinted previously that much of the impact of last year’s rate hikes is yet to hit, and cracks are forming in interest-rate-sensitive parts of the economy. Headline inflation should begin to come down more rapidly from March too, as the impact of last year's energy bill surges drop out, and core goods/food pressure begins to ease more noticeably.

We expect one final 25bp hike in March, taking the Bank Rate to a peak of 4.25%. The key question for Thursday is whether the Bank itself acknowledges its work is nearly complete. We suspect it’s more likely to keep its options open.

Here's what we expect:

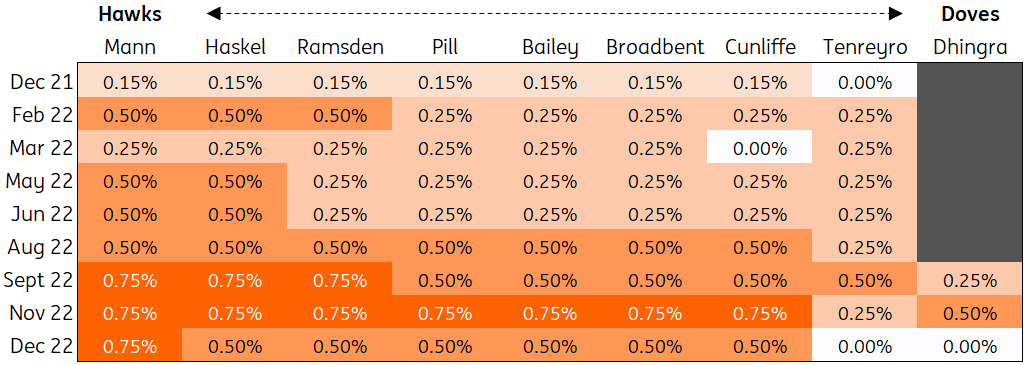

1. The vote split

December’s meeting saw the number of policymakers voting for a 75bp hike drop from seven to one, and the committee’s two most dovish officials opted for no rate hike at all. The lesson then and throughout 2022 was that the committee tends to move by consensus, and that means that the vote split is unlikely to be particularly narrow, even if the meeting is a tough one to call. Either we’ll get a similar number of officials voting for 50bp again, or we’ll see the vast majority scale back their vote to 25bp, akin to the kind of shift we saw in December.

Our base case is that we see six of the nine policymakers voting for a 50bp hike, one for 25bp and two for no change.

How each official has voted on interest rate decisions since 2021

Source: Bank of England, ING

Dr Swati Dhingra joined the committee in August 2022 and began voting in September

2. New forecasts

Calmer markets and scaled-back rate hike expectations since the mini-Budget crisis last year mean we shouldn’t be surprised to see the Bank upgrade its growth forecasts. Lower gas prices should theoretically help too, though this is a little more awkward for the BoE given that the government hasn’t yet cancelled plans to increase household bills in April, even if such a move now looks unlikely. That also means we’ll have to take the new inflation forecasts with a slight pinch of salt, and our own view is that headline CPI will end the year 1pp lower if April's planned increase is scrapped and consumer bills return to levels consistent with market pricing from the third quarter.

Still, it's the medium-term story that matters more. Keep an eye on the so-called ‘constant rate’ inflation forecasts, where the Bank assumes the Bank rate will remain unchanged from now on. If these show inflation at, or very close to, 2% in a couple of years' time, then that would be a sure-fire sign that policymakers think we’re close to the peak for Bank Rate.

3. Guidance on future policy decisions

Governor Andrew Bailey hinted recently that current market pricing, which sees a peak for Bank Rate at 4.4%, is in the right ballpark. That suggests little reason for the Bank to rock the boat too much on Thursday with new forward guidance, and we suspect it will want to keep options open.

The Bank will likely repeat that it’s prepared to act ‘forcefully’ in future if required (though we learnt in December’s minutes that 50bp hikes classify as ‘forceful’). We also doubt Bailey will be willing to be drawn on whether the Bank could pivot back to a 25bp hike in March, nor indeed whether that would be the last move in the cycle. Where he may be tempted to push back is on policy easing, especially now markets are almost pricing in one 25bp rate cut by the end of this year. Chief Economist Huw Pill’s recent emphasis on the UK sharing the worst bits of the US and eurozone’s inflation problems – structural labour shortages with the former, the energy crisis with the latter – feels like a line we’ll hear a lot over the coming months as officials try to dampen expectations of policy easing.

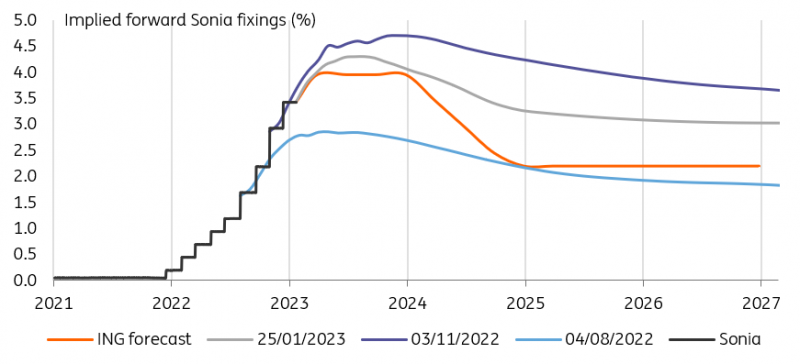

Sterling rates to tighten to euro, and a more inverted curve

The sterling rates curve still trades with a remnant of the risk premium that appeared in the run-up to the September budget debacle, making it one of the few markets where we think rates are unjustifiably high. Things have changed since then, however. Markets have come around to our more benign view on the terminal rate in this cycle, now implying hikes will stop around 4.25%. Instead, the discrepancy is to be found in longer maturities where the curve implies the Bank rate will remain elevated longer than at other central banks.

What markets expect from the Bank of England over the coming months

Source: Refinitiv, ING

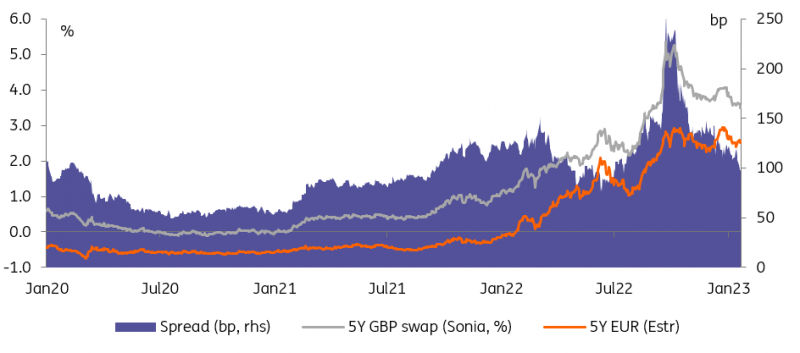

That markets taking a more hawkish view of BoE policy than signalled, for instance in its forecast, is nothing new. What’s changed is the way participants look at inflation risk. This has prompted yield curves to take a much more benign view of Fed and ECB policy. Each country is different but we find the treatment of sterling rates increasingly at odds with that of the dollar and euro. As a result, we expect the differential between 5Y sterling and euro swap rates to shrink to 75bp. This convergence should also be helped by the worsening of UK economic surprise indices, just as their eurozone equivalent goes from strength to strength.

The spread between euro and sterling swap rates is likely to narrow

Source: Refinitiv, ING

We also think the GBP curve is due to flatten further. One likely driver is the market's growing confidence that the BoE, like the Fed, will soon be in a position to cut rates, although we wouldn’t expect this before 2024. Another less probable driver would be if the BoE feels the need to tighten policy more than expected in the coming meetings. We very much doubt that longer rates would follow the short end higher, pricing instead a growing risk of rate cuts down the line to cushion the economic hit.

We think the GBP curve is due to flatten further

Source: Refinitiv, INGRead the original analysis:

GBP: Temporary strength

The BoE’s broad trade-weighted measure of sterling has bounced around 6% since the dark days of September and will marginally ease the BoE’s fears of imported inflation. Given that a 50bp hike is not fully priced for Thursday, sterling could enjoy some limited and temporary strength should the BoE indeed hike 50bp. Depending on the post-FOMC state of the dollar, that could briefly send GBP/USD back into the 1.24/25 range and EUR/GBP back to the low 0.87s.

However, the challenges facing sterling have not gone away. Large twin deficits, weak growth and what throughout the year should be building expectations that falling prices – especially from March/April onwards – will provide room for the BoE to cut rates around the turn of the year.

In terms of a profile, we think a continued narrowing in GBP rates premium to the EUR can push EUR/GBP higher through the year towards the 0.90/91 area. GBP/USD should be supported by the better EUR/USD trend, but will probably struggle to hold any gains to the high 1.20s – potentially seen in the second quarter.

Read the original analysis: Four Bank of England scenarios for February’s meeting

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.