Forecasting the upcoming week: Another go around the NFP wheel

US employment and labor data will take center stage once again as markets wind themselves up to another monthly update to US NFP net jobs additions report next Friday.

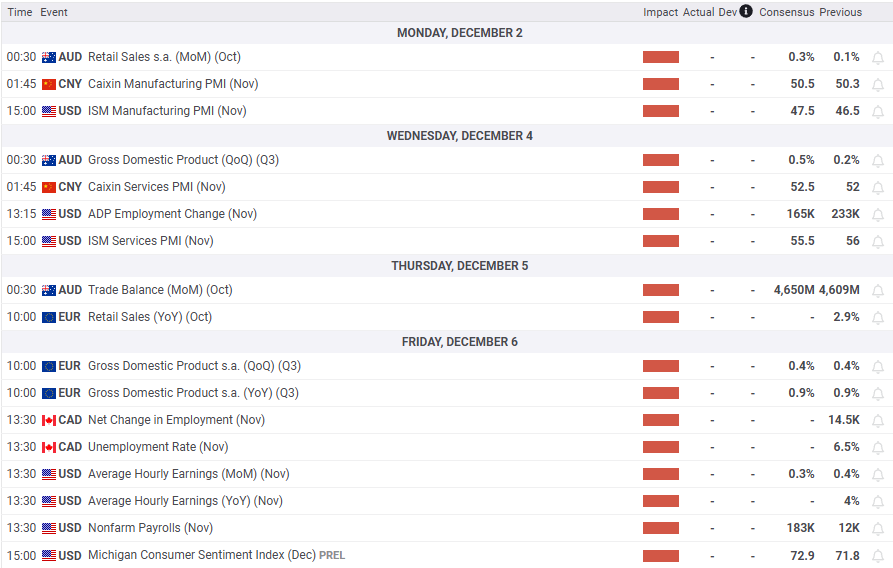

The US Dollar Index (DXY) ended the week on the low side, declining 1.64% from Monday’s opening bids and wrapping up Friday below the 106.00 handle. The Dollar Index snapped a near-term bull run, closing in the red on a weekly basis for the first time in November. Despite the soft spot, the Greenback has had a solid run, climbing nearly 8% bottom-to-top from September’s lows near 100.00 and closing in the green for all but two of the last nine consecutive weeks. Next week gives another print of US Nonfarm Payrolls (NFP), but traders will have to wade through a week’s worth of preview labor data before November’s net NFP jobs additions land on Friday.

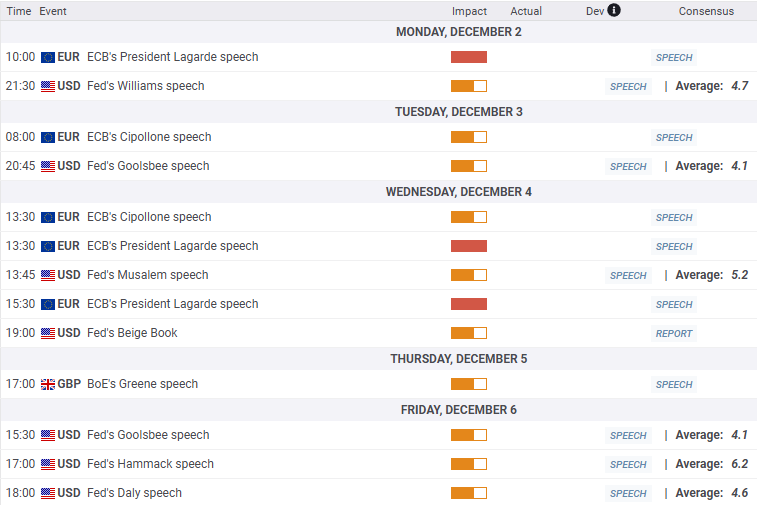

EUR/USD rose 1.57% this week, owing more to broad-market Greenback weakness than any particular bullish momentum behind the Euro. Fiber traders saw a wide swath of European data come in as-expected this week, and more of the same is on the docket for next week. European Central Bank (ECB) President Christine Lagarde will make several appearances throughout the week, but the head of the central policy-setting agency is unlikely to deliver much new to investors.

GBP/USD closed higher by 1.51% this week, marking the first bullish weekly close for Cable for the first time in eight weeks. The pair pared back some of its recent losses, but intraday price action still remains down over 5% from September’s peak bids of 1.3434. Next week is a dry showing for the Pound Sterling on the economic calendar with little of note slated for release.

USD/JPY clinched its first week of firm downside momentum since July, shedding 3.40 through Friday’s close and ending a week in the red for only the third time since mid-September. Headline Japanese Tokyo Consumer Price Index (CPI) inflation rose to 2.6% YoY, printing above the Bank of Japan’s (BoJ) allegedly-elusive 2% target for nine of the last 12 consecutive months. Despite Japanese inflation primed to overshoot the Japanese central bank’s maximum target for the majority of the calendar year, perma-dove BoJ officials have already flipped the script on investors, cautioning that long-overdue interest rate hikes will be dependent on additional factors besides inflation remaining positive yet unvolatile for an unspecified period that may extend through the second half of 2026. It’s becoming apparent to Yen traders that there functionally isn’t an economic scenario where the BoJ will be comfortable with raising rates and allow investors to treat the Yen as anything other than a funding currency.

AUD/USD clawed its way into a second week of gains despite kicking the week off with a quick dip into 16-week lows. A data-light calendar did few favors for the Aussie, keeping AUD/USD flows tied to broader market sentiment in the Greenback. Next week brings a fresh round of economic data for Aussie traders to chew on, kicking things off with Australian Retail Sales early Monday morning. Australian Purchasing Managers Index (PMI) and Gross Domestic Product (GDP) figures are both expected to deliver improved prints later in the week. Several spotlights on Chinese economic data could also drive the Aussie, with Chinese Caixin Manufacturing PMI data for November on Monday and the Services component expected on Tuesday.

Events to note next week:

Anticipated central banker appearances next week:

Central banks FAQs

Central Banks have a key mandate which is making sure that there is price stability in a country or region. Economies are constantly facing inflation or deflation when prices for certain goods and services are fluctuating. Constant rising prices for the same goods means inflation, constant lowered prices for the same goods means deflation. It is the task of the central bank to keep the demand in line by tweaking its policy rate. For the biggest central banks like the US Federal Reserve (Fed), the European Central Bank (ECB) or the Bank of England (BoE), the mandate is to keep inflation close to 2%.

A central bank has one important tool at its disposal to get inflation higher or lower, and that is by tweaking its benchmark policy rate, commonly known as interest rate. On pre-communicated moments, the central bank will issue a statement with its policy rate and provide additional reasoning on why it is either remaining or changing (cutting or hiking) it. Local banks will adjust their savings and lending rates accordingly, which in turn will make it either harder or easier for people to earn on their savings or for companies to take out loans and make investments in their businesses. When the central bank hikes interest rates substantially, this is called monetary tightening. When it is cutting its benchmark rate, it is called monetary easing.

A central bank is often politically independent. Members of the central bank policy board are passing through a series of panels and hearings before being appointed to a policy board seat. Each member in that board often has a certain conviction on how the central bank should control inflation and the subsequent monetary policy. Members that want a very loose monetary policy, with low rates and cheap lending, to boost the economy substantially while being content to see inflation slightly above 2%, are called ‘doves’. Members that rather want to see higher rates to reward savings and want to keep a lit on inflation at all time are called ‘hawks’ and will not rest until inflation is at or just below 2%.

Normally, there is a chairman or president who leads each meeting, needs to create a consensus between the hawks or doves and has his or her final say when it would come down to a vote split to avoid a 50-50 tie on whether the current policy should be adjusted. The chairman will deliver speeches which often can be followed live, where the current monetary stance and outlook is being communicated. A central bank will try to push forward its monetary policy without triggering violent swings in rates, equities, or its currency. All members of the central bank will channel their stance toward the markets in advance of a policy meeting event. A few days before a policy meeting takes place until the new policy has been communicated, members are forbidden to talk publicly. This is called the blackout period.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.