FOMC Minutes show concern that markets do not believe the Fed's resolve

The Fed is concerned that the markets do not understand it means business.

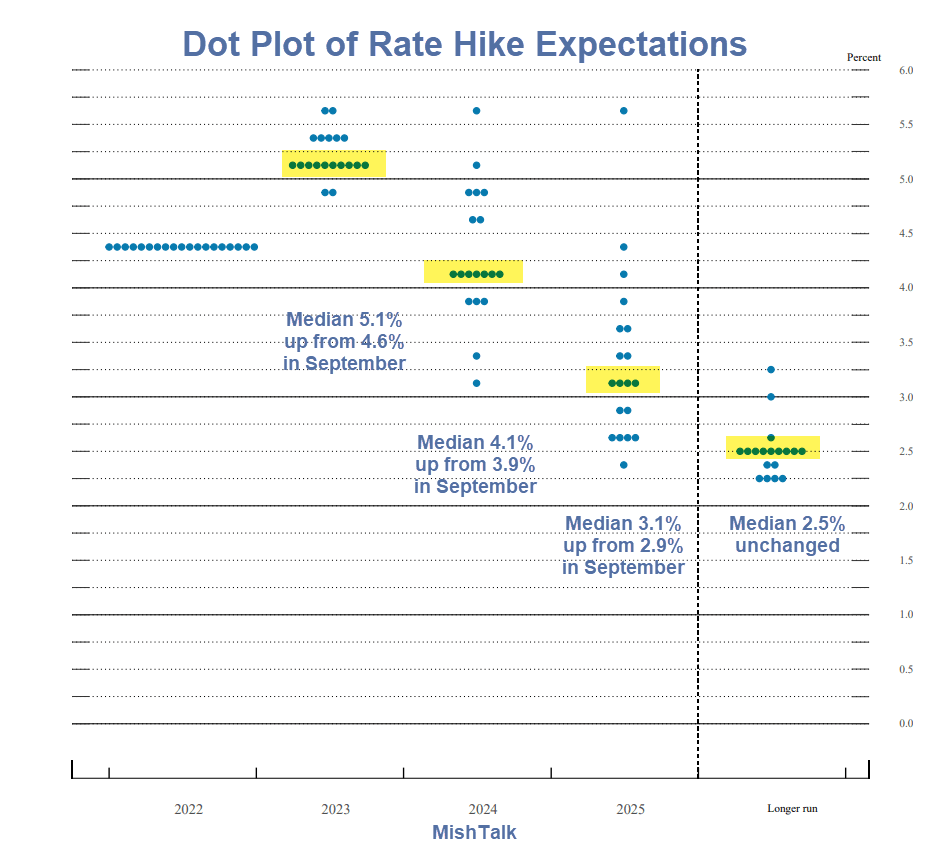

Dot Plot of Fed Rate Hike Projections

FOMC Minutes

Let's dive into Minutes of the Federal Open Market Committee December 13–14, 2022 for clues on what the Fed is thinking, emphasis mine.

Concern over misperceptions

Participants noted that, because monetary policy worked importantly through financial markets, an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the Committee’s reaction function, would complicate the Committee’s effort to restore price stability.

Several participants commented that the medians of participants’ assessments for the appropriate path of the federal funds rate in the Summary of Economic Projections, which tracked notably above market-based measures of policy rate expectations, underscored the Committee’s strong commitment to returning inflation to its 2 percent goal.

Recession risk

Many participants highlighted that the Committee needed to continue to balance two risks. One risk was that an insufficiently restrictive monetary policy could cause inflation to remain above the Committee’s target for longer than anticipated, leading to unanchored inflation expectations and eroding the purchasing power of households, especially for those already facing difficulty making ends meet.

The other risk was that the lagged cumulative effect of policy tightening could end up being more restrictive than is necessary to bring down inflation to 2 percent and lead to an unnecessary reduction in economic activity, potentially placing the largest burdens on the most vulnerable groups of the population.

Inflation risk skewed to the upside, economy to downside

With inflation still elevated, the staff continued to view the risks to the inflation projection as skewed to the upside.

Moreover, the sluggish growth in real private domestic spending expected over the next year, a subdued global economic outlook, and persistently tight financial conditions were seen as tilting the risks to the downside around the baseline projection for real economic activity, and the staff still viewed the possibility of a recession sometime over the next year as a plausible alternative to the baseline.

Participants generally noted that the uncertainty associated with their economic outlooks was high and that the risks to the inflation outlook remained tilted to the upside. Participants cited the possibility that price pressures could prove to be more persistent than anticipated, due to, for example, the labor market staying tight for longer than anticipated.

Concern over stretched budgets

In their discussion of the household sector, participants noted that growth in consumer spending in September and October had been stronger than they had previously expected, likely supported by a strong labor market and households running down excess savings accumulated during the pandemic. A couple of participants remarked that excess savings likely would continue to support consumption spending for a while.

A couple of other participants, however, commented that excess savings, particularly among low-income households, appeared to be lower and declining more rapidly than previously thought or that the savings, the majority of which appeared to be held by higher-income households, might continue to be largely unspent. Several participants remarked that budgets were stretched for low-to-moderate-income households and that many consumers were shifting their spending to less expensive alternatives.

Concern over tight labor markets and wage growth

Participants observed that the labor market had remained very tight, with the unemployment rate near a historically low level, robust payroll gains, a high level of job vacancies, and elevated nominal wage growth.

Participants noted that, in the latest inflation data, the pace of increase for prices of core services excluding shelter—which represents the largest component of core PCE price inflation—was high. They also remarked that this component of inflation has tended to be closely linked to nominal wage growth and therefore would likely remain persistently elevated if the labor market remained very tight.

Jobs

Some participants pointed out that payroll gains had remained robust even as they slowed in recent months. Nevertheless, they noted that some other measures of employment—such as those based on the Bureau of Labor Statistics’ household survey and the Quarterly Census of Employment and Wages—suggested that job growth in 2022 may have been weaker than indicated by payroll employment.

In the context of achieving the Committee’s broad-based and inclusive maximum-employment goal, a number of participants commented that as the labor market moved into better balance, the unemployment rate for some demographic groups—particularly African Americans and Hispanics—would likely increase by more than the national average.

Early retirements

With the labor force participation rate little changed since the beginning of 2022, some participants commented that labor supply appeared to be constrained by structural factors such as early retirements, reduced availability or increased cost of childcare, more costly transportation, and reduced immigration.

More restrictive stance due to uncertainty

In light of the heightened uncertainty regarding the outlooks for both inflation and real economic activity, most participants emphasized the need to retain flexibility and optionality when moving policy to a more restrictive stance.

Participants generally observed that a restrictive policy stance would need to be maintained until the incoming data provided confidence that inflation was on a sustained downward path to 2 percent, which was likely to take some time. In view of the persistent and unacceptably high level of inflation, several participants commented that historical experience cautioned against prematurely loosening monetary policy.

Some Fed comments echo many things I have written about recently. Here are some examples.

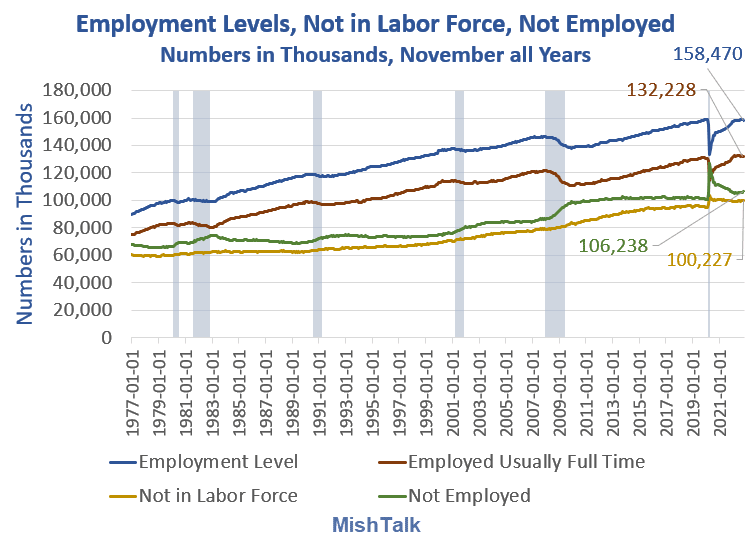

Age 16+ there are 158 million people working, 106 million not working

On January 2, I noted Age 16+ There are 158 Million People Working, 106 Million Not Working

Key age 16 and over stats

-

158 million employed.

-

132 million usually working full time.

-

106 million not employed.

-

6 million unemployed.

Gotta love this stat: 106 million people age 16 and over are not employed but only 6 million of them are unemployed.

There are 22.7 million people of retirement age who are still working. At an increasing rate over time, these people will retire. Replaced by whom? At what levels of productivity?

By the end of the decade nearly all of this group will be retired. Who will support this group and increasing Medicare needs given the percentage of full time workers keeps dropping.

So yes, early retirement and boomer retirements are both in play and both contributing to the tight labor market.

At the same time millions of others struggle to make ends meet.

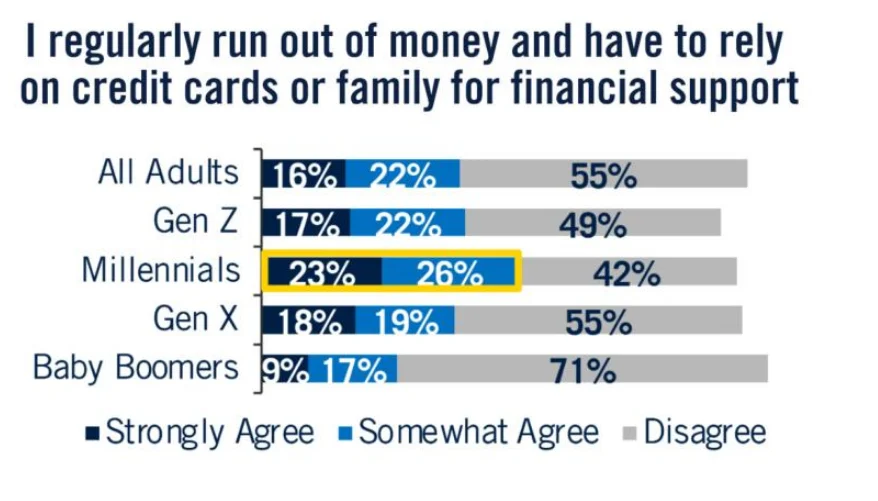

Huge temporary growth in gig work to make ends meet

Of those working, There's a Huge Temporary Growth in Gig Work to Make Ends Meet

Nearly half of millennials agree or somewhat agree with the statement "I regularly run out of money and have to rely on credit cards or family for financial support."

The Philadelphia Fed just revised jobs lower by 1.2 million for Q2

The Fed mentioned QCEW in its minutes.

I wrote about that on December 16 in The Philadelphia Fed Just Revised Jobs Lower by 1.2 Million for Q2

The Philadelphia Fed does not believe the strong jobs growth. I have been talking about the discrepancy between jobs and employment for months.

Strong jobs?

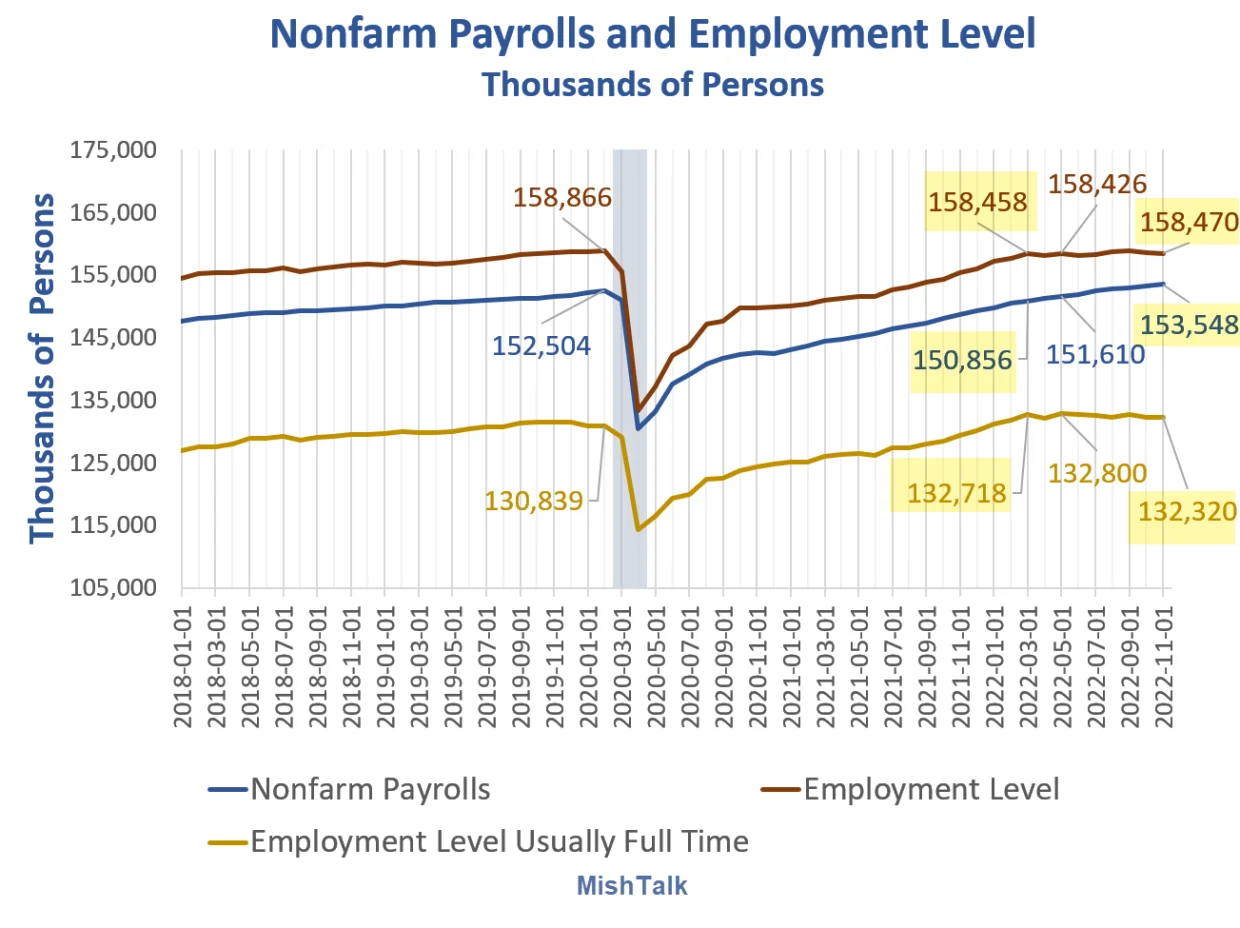

Payrolls vs employment since March 2022

-

Nonfarm Payrolls: +2,692,000.

-

Employment Level: +12,000.

-

Full Time Employment: -398,000.

I have been rethinking this.

Millions are retiring but millions of others are taking second part time jobs to make ends meet. So yes, we can be adding part time jobs while employment is stagnant.

The Fed picked up on this, at least enough to mention. But I have been commenting along these lines for months.

Fed's clear message

The Fed's message is clear.

The Fed is concerned over wage growth and persistent inflation more so than recession, stretched budgets, and the fact that housing and manufacturing that have both collapsed.

Meanwhile, ISM Manufacturing Now Signals Recession for the First Time in 30 Months

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc