FOMC July Minutes Preview: Can it influence September Fed rate hike expectations?

- Markets are yet to decide on the size of the next Fed hike.

- FOMC will publish the July meeting minutes on August 17.

- Policymakers are likely to reiterate their commitment to monitor the data closely.

The US Federal Reserve will release the minutes of its July policy meeting on Wednesday, August 17, at 18:00 GMT. The dollar started the new week on a firm footing and the US Dollar Index is already up 1%. Since the Fed’s decision to abandon rate guidance and turn data-dependent in July, markets have been trying to figure out the size of the September rate hike.

The upbeat July jobs report, which showed that Nonfarm Payrolls rose by 528,000, caused the probability of a 75 basis points (bps) rate hike to rise to 70%. Just a few days later, the US Bureau of Labor Statistics announced that inflation in the US, as measured by the Consumer Price Index (CPI), fell to 8.5% in July from 9.1% in June. This reading came in lower than the market expectation of 8.7%. More importantly, the annual Core CPI remained unchanged at 5.9%, reviving optimism about inflation having peaked in early summer. The odds of a 75 bps rate increase fell all the way to 30% on soft inflation data.

Since then, FOMC policymakers pushed back against the market view of the Fed turning dovish and starting to lower rates in the second half of 2023. Richmond Fed President Thomas Barkin said they need to continue to raise the rates to get them into the restrictive territory. San Francisco Fed President Mary Daly said that markets were getting ahead of themselves by expecting rate cuts next year and noted that she would be open to a 75 bps hike in September if data warranted it. Finally, Minneapolis Fed President Neel Kashkari said that they were “far far away” from claiming victory on inflation.

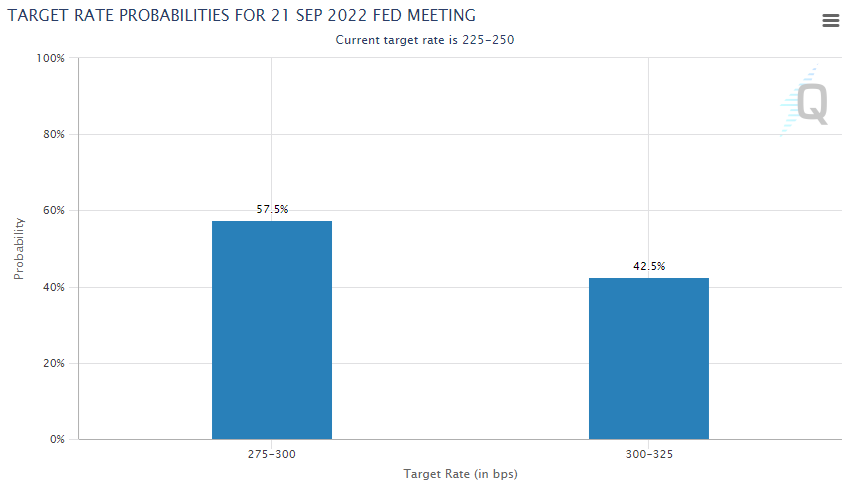

According to the CME Group FedWatch Tool, markets are currently pricing in a 42.5% chance of a 75 bps hike in September.

The FOMC’s July minutes will not reflect how policymakers see the policy outlook shaping following the latest employment and inflation data. Nevertheless, in case the publication shows that rate-setters discussed a 100 bps rate hike in July, that could be seen as a hawkish development and help the dollar gather strength. Also, any comments on the September rate decision could trigger a market reaction. If policymakers see a 50 bps rate increase as the most probable scenario unless inflation surprises to the upside, the greenback is likely to come under selling pressure with markets scaling back hawkish bets.

In case the minutes do not offer any fresh insight into the rate outlook, investors could refrain from betting on a specific rate hike next month. Policymakers are likely to reiterate that they will continue to monitor the macroeconomic developments closely and that they will not overreact to a single data point.

To summarize, the Fed minutes could do little to nothing to help investors make up their minds about the next policy move. The tight labor market conditions should allow the US central bank to stay on an aggressive tightening path despite growing signs of a slowdown in economic activity. Meanwhile, inflation stays way above the Fed’s target rate and policymakers made it clear that they want to see price pressures easing for consecutive months before thinking about reassessing the policy strategy.

Ahead of the September 20-21 FOMC policy meeting, markets will have August inflation and employment data to assess and they are unlikely to decide on the size of the next Fed rate increase by scrutinizing the July meeting minutes.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Eren Sengezer

FXStreet

As an economist at heart, Eren Sengezer specializes in the assessment of the short-term and long-term impacts of macroeconomic data, central bank policies and political developments on financial assets.