Five factors moving the US dollar in 2021 and not necessarily to the downside

- Optimism about the recovery leads analysts to foresee a dollar downfall in 2021.

- The Federal Reserve is not the only central bank that is set to influence the greenback.

- President Biden’s stimulus efforts and the way he shapes relationships with China are also critical.

For the dollar, that light at the end of the tunnel turned out to be a truck roaring at full throttle to run it down. The news of coronavirus vaccines sent stocks higher and the safe-haven dollar lower. Alongside decisive US elections and later some fiscal stimulus, there was no need to run for shelter, and the dollar suffered.

The consensus trade is that the late 2020 trend is a friend – an extended greenback grind in 2021. Here are five factors that may add fuel to the fire or potentially calm it and extinguish it.

1) Federal Reserve policy in 2021

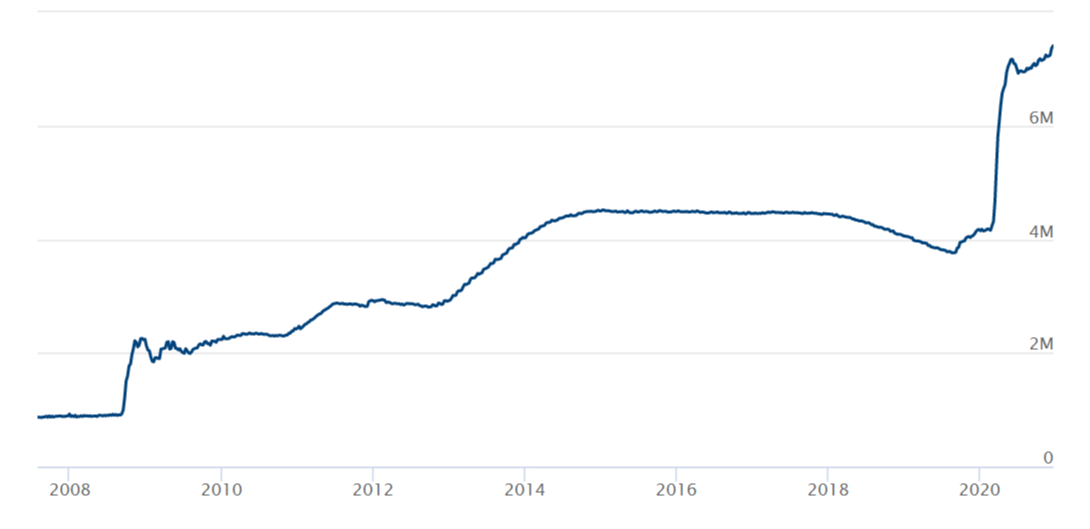

The world’s most powerful central bank remains the No. 1 force in moving currencies, and that is unlikely to change. The Federal Reserve has signalled it would not be raising rates through 2023. Jerome Powell, the bank’s Chairman, communicated how the bank would taper down its substantial bond-buying scheme and is also far off.

The Washington-based institution is creating some $120 billion out of thin air every month and remains ready to ramp it up if needed. Contrary to reactions in the UK and the eurozone, printing greenbacks has resulted in a straightforward devaluation of the dollar. With the pedal to the metal, further falls are likely.

Fed Balance Sheet 2008-2020

Source: Federal Reserve

However, nothing lasts forever, and that includes the bank’s rates and QE commitments. The Fed’s policy review in 2020 prioritized its full employment goal at the expense of allowing inflation to overheat. The bank would even welcome signs of price rises – reflecting a growing economy and also compensating for subdued inflation in previous years.

However, there is a case for prices to advance too quickly. The COVID-19 crisis caused production to shutter due to the lack of demand. If people can quickly return to normal lives, consumption is set to increase rapidly, especially backed by fiscal and monetary stimulus. That recovering demand may exceed supply and prompt short-term increases in prices.

Long-term inflation may also move higher as a result of deglobalization. The pandemic has shown the pitfalls of relying on cheap imports and the need to source products locally.

To battle rising inflation, the Fed could raise rates – boosting the dollar.

The Federal Reserve is unlikely to hike interest rates at first sight of inflation, but it may signal that it would withdraw bond-buying or move rates higher in 2022. Any indication that loose monetary policy is tightening would spook markets and already caused a reversal of the overextended greenback grind.

2) Recovery from the pandemic

Western countries began their vaccination campaigns before 2020 ended, providing hope that by some point in 2021, things will be back to normal. As long as immunization schemes move forward, markets are likely to continue their uptrend and the dollar its descent.

Israel is turning into a test case for vaccines – aiming to inoculate vulnerable populations by the end of January and a majority of the country by the end of March. If a country of nine million people eases restrictions of its third lockdown without enduring an increase in hospitalizations, it will serve as real-world proof that vaccines defeat the virus.

Throughout 2021, AstraZeneca, Johnson and Johnson, and other immunization projects are set to join the Pfizer/BioNTech and Moderna successes of 2020. The pace of vaccinations is set to accelerate and bring the world back to normal, boosting sentiment and weighing on the dollar.

However, there is a downside potential as well. Covid, like any virus, can mutate and become resistant to the jabs, forcing researchers to go back to the labs and remake their inoculations. At the time of writing, the British variant likely succumbs to available vaccinations, but that is not the end of the story.

While the second generation of vaccines will likely come at an even greater speed than the first one, any delay in resolving medical issues would slow the recovery.

Coronavirus cases developments in the US, the EU, and the UK:

-637454446918660865.png)

Source: Financial Times

In that scenario of a constant struggle between scientists and the virus, 2021 would not be the end of the virus, and investors would flee to the safety of the dollar.

3) US fiscal stimulus

President Donald Trump signed a $900 billion stimulus bill less than a month before he leaves office. What will his successor Joe Biden do? The answer heavily depends on the Georgia runoff races on January 5. If Democrats win both contests, they will have an effective majority in the upper chamber of Congress.

Biden and Democrats will be unable to enact sweeping reforms – including business-unfriendly ones – but probably add between $1 or $2 trillion to government spending. Apart from aid to states and the unemployed, they could lift America’s often-crumbling infrastructure – another boost to the economy. In that outcome, the dollar would suffer.

Another upbeat scenario is that Senate Majority Leader Mitch McConnell – Biden’s former colleague and coming from the same cohort – would collaborate with the White House on certain issues. Biden would achieve less if Republicans hold the upper chamber, but markets – not only in the US – would welcome any additional cash.

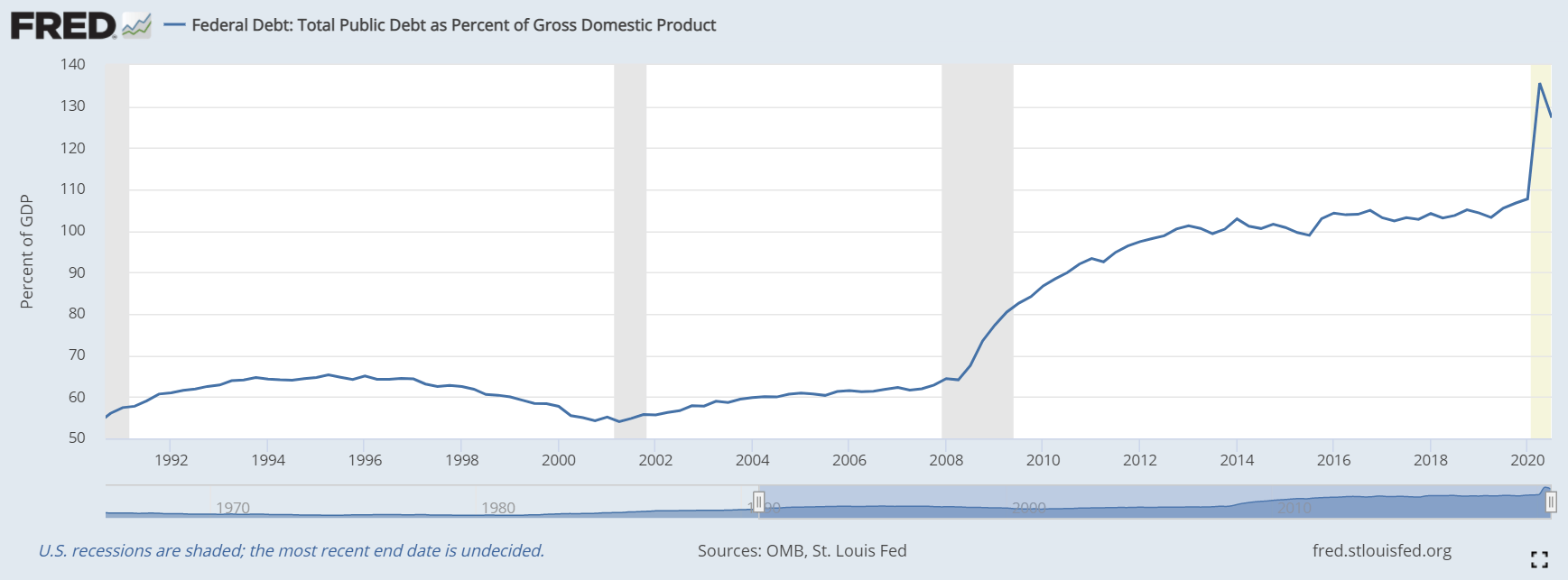

US debt-to-GDP, a question for another day:

Source: Federal Reserve

The flipside is that the GOP returns to sabotaging the economy as it did when Biden was Vice-President. If McConnell refuses to bring any suggestion to the Senate floor, recovery in both the US and the world would slow down, boosting the greenback.

Currency traders cannot take their eyes off Washington after Trump departs.

4) Global trade relations

Chinese President Xi Jinping and Trump clashed over trade in 2019 and tech and the virus in 2020. The change of guard at the White House means relations between the world’s largest economies are set to transform – but tensions are set to intensify rather than wane.

As Vice-President, Biden was involved in the Trans-Pacific Partnership (TPP). The deal encompassed the world’s largest ocean – and was worth around 40% of global output – but excluded China. The thinking at the time was to force standards on Beijing. Trump withdrew from that accord in his first week in office and sought commerce clashes with countries around the world, friend or foe.

There is a rare bipartisan consensus in Washington against China that would support “ganging up” Western economies such as EU ones against Beijing. Xi and his colleagues are unlikely to bow to concerted pressure so easily, and Biden said he would not rush to undo Trump’s tariffs.

Additional sanctions against Chinese companies and tensions around Taiwan and Hong Kong cannot be ruled out throughout the year, and these may send investors to the safety of the US dollar.

The US and China are around 40% of the global economy:

Source: Visual Capitalist

The new president touted his working-class credentials on the campaign trail and will likely attempt to revive American manufacturing. Will the US and China accelerate their decoupling? These massive economies still depend heavily on each other, and the occasional soothing of tensions would weigh on the greenback.

Nevertheless, unless the rules of commerce are re-established – under a reformed World Trade Organization (WTO) – Sino-American tensions will probably be a positive factor for the dollar in 2021.

5) ECB action

The European Central Bank cannot compete in influence with the Fed, but its impact on the dollar is growing. The Frankfurt-based institution has upped its game around the pandemic and unchained itself from self-imposed limits to bond buying.

Another result of the covid crisis has been the common currency reaction to additional euro printing. Instead of a sell-off, every expansion of the ECB’s Pandemic Emergency Purchase Program (PEPP) boosted the euro. The new narrative is that the funds allow governments to support the economies and thus strengthen the currency.

At least in the early part of 2021, this phenomenon may continue in full force, boosting the single currency and pushing the euro higher at the expense of the dollar. Moreover, money coming out of Frankfurt may seek high yields outside the eurozone and beyond American shores in places such as emerging markets. That may also indirectly contribute to the downfall of the dollar.

However, the latter half of the year may see a change. The ECB could signal that it is letting its program lapse in early 2022 as planned, thus weighing on the currency and supporting the dollar. Moreover, the bank may further cut its deposit rate below -0.50% – a move that would depress the currency.

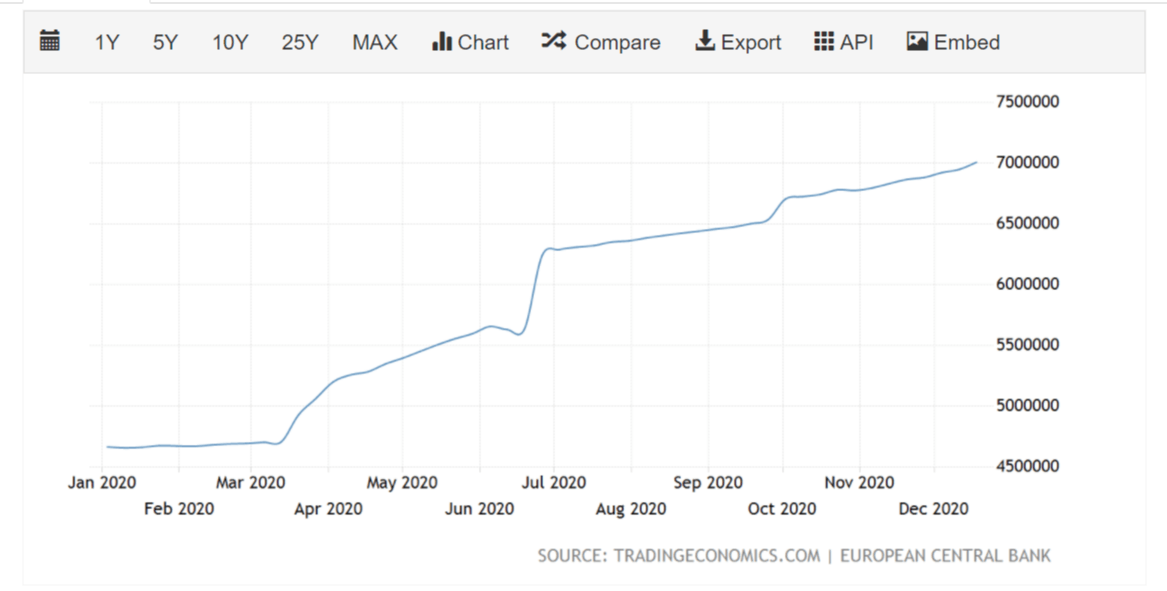

ECB Balance sheet:

Source: Trading Economics

While the ECB is unlikely to be a major factor in determining the dollar’s direction, it will likely have a growing influence.

Conclusion

The Federal Reserve actions, the recovery from the pandemic, US fiscal stimulus, trade tensions, and the ECB are all set to shape the dollar in 2021. However, as 2020 has shown, unforeseeable developments may also rock the world.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.