Federal Reserve scenarios: More twists and turns to come

Having priced a high chance of an inter-meeting Fed rate cut last week, interest rate expectations have moderated in the wake of better data and calming words from Fed officials. Nonetheless, uncertainty surrounding the path for Fed policy rates remains high so here we look at our base case versus market pricing and how alternative scenarios could pan out .

Markets trim bets on aggressive rate cuts but uncertainty is high

Weaker survey data, softer inflation, subtle shifts in the Federal Reserve's thinking and a poor July jobs report saw markets dramatically ramp up interest rate cut bets last week. These moves were then amplified in feverish markets as the unwinding of the yen carry trade saw a flight to safe havens. At one point the market was anticipating an inter-meeting interest rate cut by the Fed with nearly 140bp of cuts priced by the end of this year. Calm has since returned with just under 40bp now priced for the September FOMC meeting, with 100bp of cuts seen between now and the end of the year. In the wake of last week’s market volatility, we thought it would be useful to compare our view of what the Federal Reserve is likely to do, set against the market pricing. We have also added a couple of other scenarios – one where the labour market deteriorates more rapidly than we are forecasting and another where inflation stays higher for longer, generating fears of stagflation. This is to illustrate the point that economic uncertainty means elevated market volatility could remain with us for a while.

What the market is currently pricing

A fairly dovish-sounding Jerome Powell at the most recent FOMC meeting suggested greater confidence that inflation is on a sustainable path to 2%, meaning the Fed can start to think more about its second target – maximum US employment. The subsequent soft jobs report with unemployment hitting 4.3% has led to a narrative that the Fed is behind the curve and needs to cut interest rates more aggressively if it is to avoid a recession and achieve its aim of a soft landing. As the market currently sees the situation, the Fed will deliver 100bp of cuts this year and the Fed funds gets to a “neutral” level of 3-3.25% by mid-2025.

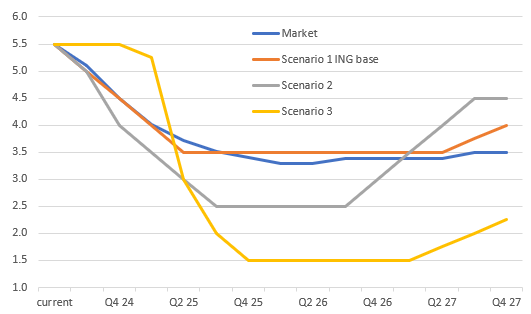

The potential path for the Fed funds rate under different scenarios

Source: ING, Bloomberg

Scenario one (ING base case)

Fed cuts rates 50bp in September with 25bp cuts in November and December. The Fed funds rate is then lowered to 3.5% in 2025 (50% probability).

The economy is still growing, adding jobs, and inflation is above target. But of course, the Fed doesn’t want to cause a recession by keeping policy too tight for too long, if it can avoid it. Inflation continues to look well-behaved, allowing the Fed to put more and more emphasis on its labour market target of “maximum employment”. Nonetheless, the Fed acknowledges that its June forecasts were far too optimistic (unemployment ending the year at 4%, for example). In the absence of any financial system threat, the Fed kicks off its loosening cycle with a 50bp cut as it “catches up” with where the data currently is, but then reverts back to the more typical 25bp increments. It takes policy to a “neutral” level of 3.25-3.5% with a “soft landing” achieved.

This is a mildly bearish scenario for the dollar. EUR/USD can probably trade up to 1.10 at the start of the Fed easing cycle, but further gains may be harder to come by as Europe is also engaging in a tighter fiscal/looser monetary policy mix.

Scenario two

Worries about job lay-offs prompts the Fed to cut rates more aggressively to try and head off the threat of a downturn (35% probability).

The rise in unemployment has so far been caused by labour supply exceeding demand for workers, rather than job lay-offs. However, that narrative starts to change with the number of firings increasing, and in an environment of diminishing inflation worries, the Fed cuts rates more aggressively and takes the policy rate into mildly stimulative territory. It then starts to move policy to a more neutral footing in late 2026 as the economy stabilises.

The dollar drop should be deeper here, given that a terminal rate of 2.5% is well below what is currently priced in the forwards curve.

Scenario three

Stagflation fears mean higher near-term rates, which prompt a recession. Fed eventually responds more aggressively, leading to lower longer-term borrowing costs (15% probability).

Inflation remains stickier than hoped and forces the Fed to keep policy tighter for longer. With the jobs market weakening, stagflation fears rise. A deepening recession from late 2024 into early 2025 helps to dampen price pressures, giving the Fed scope to start cutting rates from the late first quarter of 2025. The Fed need to go harder and faster to offer support for the economy and prevent inflation from undershooting its target too much. Monetary policy moves into stimulative territory and then it starts to normalise from mid-2027 onwards.

Stagflation is not a good look for FX markets. The US yield curve would re-invert again which will favour the dollar against the pro-cyclical currencies and most emerging currencies in general. Heavy losses could ensue for commodity currencies until the Fed signals the all-clear on inflation. Thereafter, the dollar could fall sharply across the board and to deeper levels than in Scenarios 1 and 2 - as the Fed cut rates below 2%.

Politics will also play a role

It is important to point out that this is a macro scenario analysis. We have not overlayed US election risk. That is described more directly in an earlier note we published here. The basic assumption being that Donald Trump’s policy mix of extended and potentially expanded tax cuts, immigration controls and trade tariffs would likely be more supportive of domestic demand growth in the near term (especially relative to Kamala Harris’ policy of letting tax cuts sunset in 2025). This may keep inflation a little more elevated while immigration controls could, at the margin, lift wage pressures while tariffs will disrupt supply chains with the risk of higher prices for consumers. Slightly stronger growth with higher inflation may make the Fed more wary about cutting rates under a Trump presidency whereas in a Harris presidency, the Fed may feel there is more scope for looser monetary policy, perhaps to the tune of a 50bp lower terminal interest rate.

Politics of course plays a big role in the dollar story too. The path of the dollar after November will largely be determined by who is in the White House and the makeup of Congress. A looser fiscal-tighter monetary policy mix under Donald Trump would be a stronger policy mix for the dollar. Kamala Harris as president would likely see the dollar soften on the prospect of tighter fiscal policy - plus a less aggressive trade and foreign policy agenda.

Read the original analysis: Federal Reserve scenarios: More twists and turns to come

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.