Federal Reserve Rate Policy Decision: The taper is coming, “soon”

- Fed leaves fed funds rate, bond program unchanged as widely expected.

- Federal Reserve Chair Jerome Powell promises a taper “soon” but declines to say when.

- Market interest rates will likely rise long before the Fed begins a fed funds cycle.

- Economic projections indicate slower growth, higher inflation and a rate hike in 2022.

The Federal Reserve held the base rate near zero, lowered its growth estimates and predicted higher inflation, but it was Chair Powell’s insistence that a taper is coming that garnered market attention.

These developments of the September Federal Open Market Committee (FOMC) meeting were largely foreseen, through the official statement added a phrase making the prospective bond taper bank policy.

“ If [economic] progress continues broadly as expected, the Committee judges that a moderation in the pace of asset purchases may soon be warranted,” said the FOMC statement.

Mr. Powell noted several times in his news conference that the time for the withdrawal of monetary policy support for the US economy is approaching.

"Many on the committee feel that substantial further progress test for employment has been met. Others feel it's close. They want to see a little more progress. There is a range of perspectives. I guess my own view would be the substantial furthered progress test for employment is all but met," observed Mr. Powell.

Treasury yields and fed funds

The Fed chair struck another theme that has been a constant as the central bank has worked to prepare markets for the inevitable end of the monthly purchase of $120 billion of Treasuries and asset-backed mortgages.

Bank officials have insisted that beginning the taper is not, in Mr. Powell’s words, a “direct signal” for a rate hike.

While that may be strictly true, once the announcement is made with the start date and amount of the taper, it is very likely that Treasury yields will move higher. As Treasury yields climb so will commercial interest rates. For the business and consumer worlds, a taper anouncement will be a rate hike.

Mr. Powell noted that the criteria for raising the fed funds rate are very different than for ending the pandemic's emergency policy accomodation. That does not change the fact that the economic impact of higher interest rates will be felt long before the Fed hikes its official base rate.

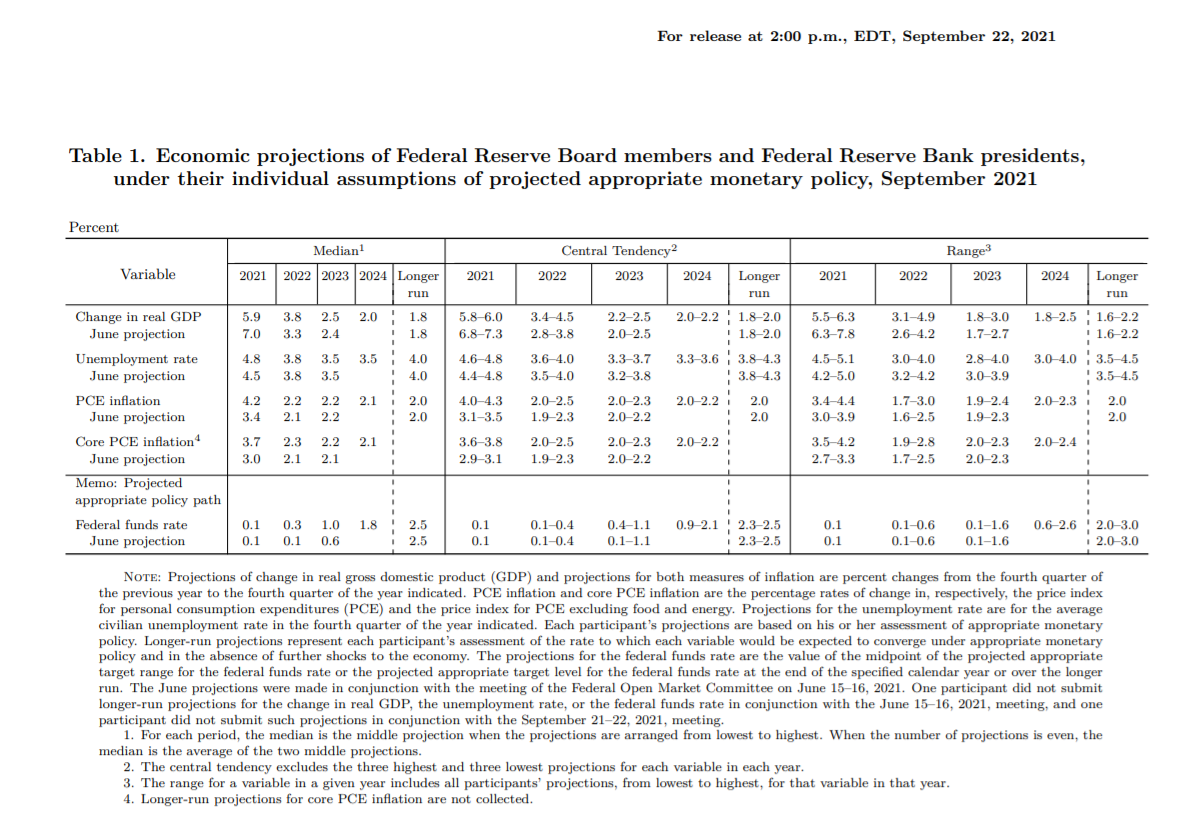

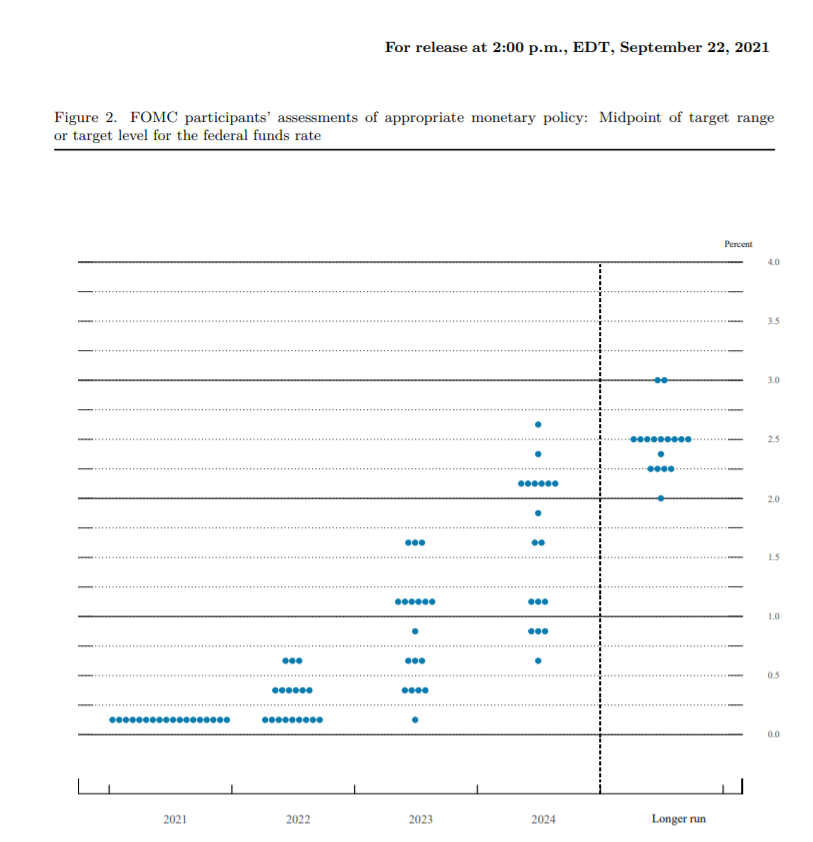

Projection Materials

The Fed’s quarterly predictions for the economy reflected the changes in the US since the last set in June.

Economic growth is now expected to be 5.9% this year, down from 7.0% in the June materials. Inflation is higher with overall Personal Consumption Prices (PCE) at 4.2% for 2021, up from 3.4% last time. Core PCE rises to 3.7% for the year from 3.0%. Finally, unemployment is predicted to fall more slowly, ending the year at 4.8% instead of 4.5%.

The growth figures acknowledge the slowing economy. The Atlanta Fed GDPNow model has the expansion at 3.7% annualized in the third quarter, after 6.4% in the first half.

Inflation is the most problematic for the Fed’s own assertions that US price increases will moderate back towards the bank’s 2% target.

In March, the members expected headline PCE inflation to be 2.4% for the year and core to be 2.2%. In just six months those projections have jumped nearly 60%.

Fed officials were making the same confident inflation predictions in January that they are making now.

With prices on the production side continuing to rise at a rapid rate, the Producer Price Index was 8.3% in July and labor shortages showing no signs of diminishing, there are many reasons to believe that the central bank is again underestimating the change in inflationary expectations driving American price increases.

The forecast for the first fed funds increase moved, just barely, into 2022. Nine of the 18 Fed members contributing their views expected the Fed to hike rates next year.

Market response

The dollar fell after the FOMC release as markets initially responded to the lack of a tapering date.

Mr. Powell’s repeated insistence in the press conference that the taper is the next policy change, and that the economy is ready, combined with the specific advance of a fed funds hike into 2022, brought traders to a different view.

By Wednesday’s close the greenback was ahead in every major pair except the aussie, kiwi and the Canadian dollar, which gained on the news reports that China’s Evergrande Property said it would make its scheduled bond payments on Thursday. .

The EUR/USD finished at 1.1688, its first close below 1.1700 since August 19 and only the second time since November 2, 2020. The USD/JPY finished at 109.78, up 55 points.

-637679560888451331.png)

Equities shed some of their pre-FOMC gains but closed with the three major New York averages up about 1%.

Treasury yields were slightly lower with the 10-year losing 3 basis points to 1.302% and the 2-year down less than a point to 0.236%.

10-year Treasury yield

CNBC

Conclusion

Mr. Powell achieved his goal. The taper has moved closer but Treasury rates did not soar and equities did not panic.

It remains to be seen how long the Fed Chair can keep this verbal prestidigitation intact.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.