Federal Reserve Preview: Powell to propel US Dollar higher with hawkish tone

- The Federal Reserve is widely expected to leave its rates unchanged at 5.25%-5.50% and signal a hike in November.

- Investors will also eye changes in the bank's projections for borrowing costs next year, which currently point to four cuts.

- Fed Chair Jerome Powell's tone will likely be hawkish, having the final say for the US Dollar.

Making it up as they go – that is a less generous way to describe the Federal Reserve's declared data-dependent policy in recent months. Giving Fed Chair Jerome Powell and his colleagues more credit, the bank is slowing down its tightening campaign but has yet to declare victory on inflation, and for good reasons. This is why a hawkish tone is likely this time, favoring the US Dollar.

Here is a preview of the Federal Reserve's decision on Wednesday, at 18:00 GMT.

Fed worries about undefeated inflation, resilient consumer

US CPI inflation. Source: FXStreet

The Fed has more impact on costs related to other goods, services, and housing, and little impact on energy and food prices, which are set on global markets. The Core CPI, which excludes volatile items, is down from a peak of 6.6% YoY in September 2022 to a fresh cycle low of 4.3% in August.

Nevertheless, the Washington-based institution aims for levels around 2%. The recent 0.3% rise in Core CPI MoM causes unease as it exceeds the previous months' increases. . It shows price pressures have not been crushed, not yet.

Core CPI inflation MoM. Source: FXStreet

Uncertainty dominates other data points as well. Apart from inflation, the Fed is mandated with pursuing full employment. The most recent Nonfarm Payrolls reports show a moderation in job growth, but wage growth is still elevated at 4.3% YoY.

Consumers, which are responsible for roughly 70% of the US economy, have yet to halt their shopping sprees. The past two retail sales reports showed healthy expansion rates – 0.6% in August and 0.5% in July.

House prices are down by 1.2% YoY, according to the Case Shiller House Price Index (HPI) for June, but the data beat estimates for the fifth time in a row.

The Federal Reserve increased interest rates to a range of 5.25%-5.50%, but has been tapering down the pace of hikes, pausing in June for the first time in over a year. It then raised borrowing costs in July, in what seems like an unofficial shift to hiking every other meeting for the remainder of the year.

The rate decision and hints for the next meeting in November is one of three things to watch out for.

Three market-moving factors in Fed decision

1) No rate hike, but probably a hint for one in November

The Fed is extremely likely to leave interest rates unchanged at 5.25%-5.50%, as that is what it signaled to markets, as it usually does. Chair Powell and company refrain from surprising investors. A no-hike scenario is fully priced in.

However, the next move is uncertain, and the "dot plot" is critical here.

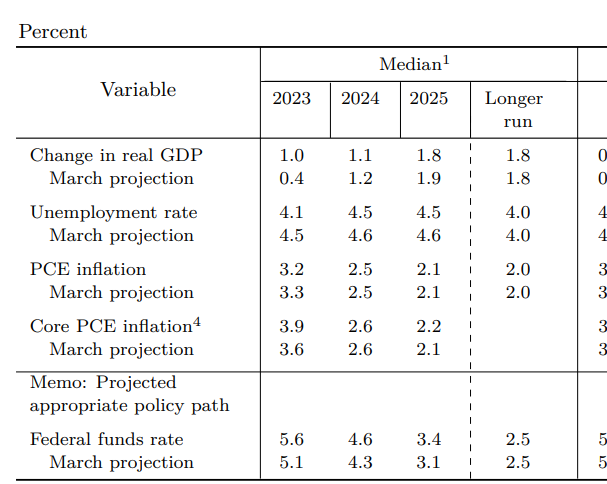

The September meeting includes new projections, officially called "Summary of Economic Projections” or "dot plot" in the jargon. Each member of the Federal Open Markets Committee (FOMC) puts down estimates for economic growth, employment, inflation and interest rates.

Markets digest numerical data faster than words, and the interest rate expectation for the end of 2023 is critical. In the last Fed projections back in June, the median hit 5.6%, two rate hikes above the level back then. With one hike done in July, leaving the figure at 5.6% would signal the bank is not done yet – or at least not willing to admit it now.

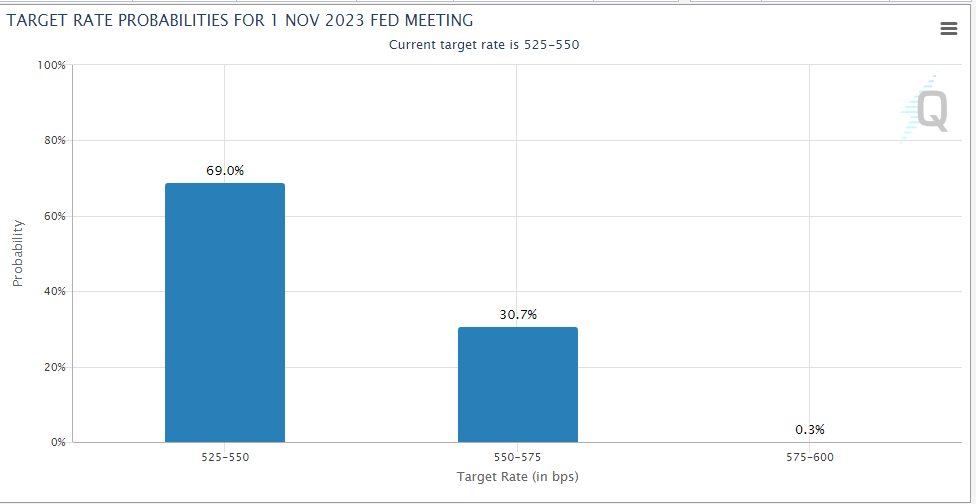

Bond markets project only a 30% chance of a hike in November:

Bond market pricing of interest rates, as of September 19, Source: CME Group

If the projection for 2023 remains unchanged, there is room for a bump up in yields, pushing the US Dollar up, and weighing on stocks and Gold.

I expect Powell to keep the door open to another move, especially after the recent upbeat economic data.

2) Fewer cuts in 2024 may add to US Dollar oomph

The Fed and investors are already looking at next year, when they expect lower inflation and a slower economy to trigger interest rate cuts.

The June dot-plot pointed to a median borrowing cost of 4.6%, a full percentage point – or four standard 25 bps cuts – from the bank's peak projection for 2023.

June SOMP. Source: Federal Reserve

Here, investors and the Fed are more aligned. Bond markets price the first cut for July 2024, the fifth of eight decisions. That allows for four consecutive cuts in the second half of the year.

Will the Fed's median rate remain at 4.6% in its new projection for 2024? I expect a small bump up, perhaps to 4.8%, which would scare investors. An unlikely decrease to 4.3%, as seen in the dot plot in March, would cheer markets.

I want to stress what Powell will emphasize – these projections are not commitments, and the further they are in the future, the less they matter. Nevertheless, markets need to act with certainty despite uncertainty.

3) Fed Chair Powell's tone will likely be hawkish

The Fed announces its decision and releases an accompanying statement at 18:00 GMT, with the dots set to overshadow any changes to the text. These were minor last time. The last word belongs to Chair Powell, who starts his press conference at 18:30 GMT.

Circling back to the beginning of this preview, the almighty central banker will likely insist on being dependent on incoming economic data, opening the door to hiking or cutting rates as needed.

Nevertheless, his tone is set to make a difference. A focus on battling inflation would weigh on sentiment, sending stocks and Gold lower, while boosting the US Dollar.

If Powell expresses concerns about the economy – mentioning weakness in the Chinese economy, downward revisions to past employment gains or S&P Global's soft PMIs – the US Dollar would be the sole loser. I see this as unlikely. Most figures have been upbeat of late, including reemerging inflation in services and housing.

Here is one last hawkish chart. The most respected forward-looking indicator for the largest sector, the ISM Services Purchasing Managers' Index (PMI), also shows signs of bottoming out. It signaled accelerating growth with a score of 54.5 in August.

ISM Services PMI. Source: FXStreet.

Final thoughts

The Federal Reserve is set to leave its rates unchanged, but it is also expected to signal one last move this year and slower cuts next year. This willingness to squeeze inflation – even at a high cost – will likely hit markets and boost the US Dollar.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.