Federal Reserve Preview: How to trade Powell's powerful market whipsaw

- The Federal Reserve is set to raise interest rates by 25 bps in its May meeting.

- Investors want to know if one more hike is coming in June.

- Recent economic data has been mixed, and the impact of the banking crisis is unclear.

- Fed Chair Jerome Powell will likely reject any notion of an imminent pause.

Are we there yet? The question that impatient children ask their parents on a road trip is what markets want to know from the Federal Reserve – if May's rate hike is the last one. Wishful thinking may lead to a cheerful reaction. However, Fed Chair Jerome Powell will likely wish to leave the door wide open for another move.

Here is a preview of the Federal Reserve's upcoming decision, published on May 3 at 18:00 GMT.

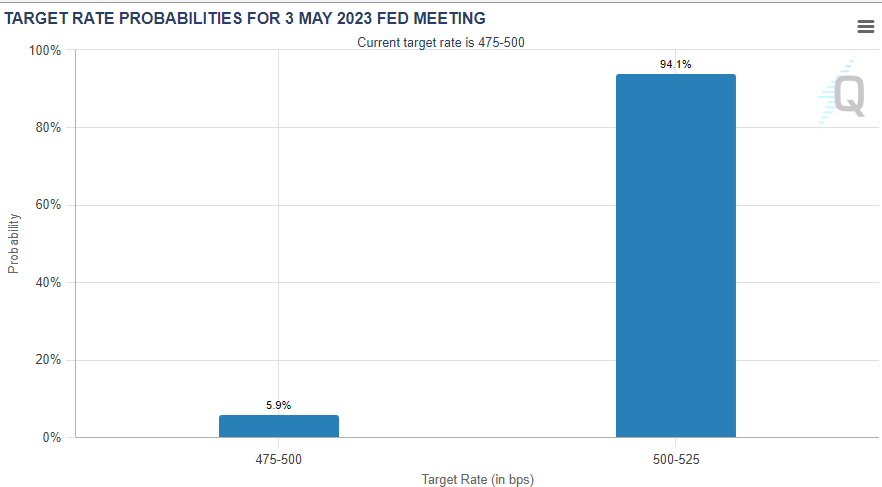

A 25 bps hike with massive uncertainty afterward for the Fed

First thing first: the world's most powerful central bank is widely expected to raise interest rates from a range of 4.75-5.00% to 5.00-5.25%. As a rule, the Fed refrains from surprising markets with its main decision and leaks to the press if push comes to shove: markets priced a 25 bps hike, and the Fed has accepted it, so that will happen.

Source: CME Group

The question is: what will the Fed do next? The Washington-based institution does not publish new projections in the May release, leaving markets to focus on the statement at 18:00 GMT and then on Powell's press conference at 18:30 GMT.

The Fed says it is data dependent – a debatable claim, more later – so what do economic figures say? Inflation is falling, but not enough. The Core Personal Consumption Expenditure (Core PCE), the bank's preferred inflation gauge, remained at 4.6% YoY in March, above expectations. On the other hand, the monthly pace is at a more moderate 0.3% MoM., reflecting an annualized pace of under 4%.

The Core Consumer Price Index (Core PCE) is still at 5.6%, which is too high, but headline CPI tumbled to 5%, and producer prices were surprised to the downside. All in all, inflation is moderating, albeit slowly, with greater hopes for the future.

Core CPI is "cresting"

Source: FXStreet

What about the labor market? The Fed has two mandates, price stability and full employment. The US economy created a healthy 236,000 jobs in March, beating downbeat estimates and exceeding the pre-pandemic average of 200,000. On the other hand, this is a material slowdown and wage growth fell to 0.2% MoM.

This mix of data is also seen in volatile Retail Sales figures, weak but recovering Purchasing Managers' Indexes (PMIs) and the recent Gross Domestic Product (GDP) data. While headline growth tumbled to 1.1%, consumer spending was upbeat.

The Fed has one eye on the data and another on the banks

As mentioned before, economic data is one of many games in town. The collapses of Silicon Valley Bank, Credit Suisse, and, most recently, First Republic Bank have also impacted monetary policy. First, while markets see these cases as idiosyncratic, there may be more skeletons in the closet. Any additional bank failure could spook businesses.

Idiosyncratic First Republic Bank

Source: TradingView

More importantly, big banks, who were always more cautious with lending, now wield more power. They may further tighten credit conditions amid less competition. The financial system withstood the shocks, but the economic impact still needs to be determined.

If companies have less funding, they may adapt by slowing their expenses and hiring. If banks are stingy, there is no need for further hikes from the Fed. Higher borrowing costs are still warranted to calm inflation if things have settled.

With the latest event happening only on Monday, the Fed may want to refrain from committing to the next moves based on the possibility the banking crisis has further to run.

How the Fed decision may play out in markets

Uncertainty about the nature of the slowdown and the impact of the banking crisis will likely lead the Federal Reserve to repeat its cautious stance. In March, due to uncertainty, the bank deliberately moderated its language – Chair Powell explained the change in his statement.

I expect this caution to cause investors to hope the Fed has ended its hiking cycle, beginning a pause period followed by cuts. Stocks and Gold would rally on such expectations, while the US Dollar would fall.

However, uncertainty means keeping all options on the table. Fed Chair Powell is set to reject any notion that the bank is done hiking in his press conference. He will go beyond token remarks of "doing what is needed" and firmly place another 25 bps hikes on the table.

In response to such remarks – and sticking to the bank's projections of refraining from cuts until year-end, markets may reverse course. Stocks and Gold would stumble, while the US Dollar would advance on such developments.

Final thoughts

The then Fed Chair Alan Greenspan once said, "If I've made myself clear, you must have misunderstood." While the modern Fed is far clearer, the reality is murky, which means a messy market reaction. The bank's decision often triggers a whipsaw in markets – and this time, it may be first against the US Dollar, then in favor. In any case, trade with care, as Fed decisions tend to be messy.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.