Federal Reserve Preview: Dollar buying opportunity? Why Powell is unlikely to cement a pivot

- The Federal Reserve is set to raise rates by 75 bps for the fourth consecutive time.

- A slowdown in housing and a dovish Fed attack have lowered expectations for December's move.

- Rising core inflation and longing job gains leave room to counter that notion.

- Fed Chair Powell is unlikely to commit to slowing down the pace as markets expect.

- The dollar may stage a rebound in response to the Fed decision.

Is it the Federal Reserve's last hurrah? That notion of an upcoming slowdown in US rate hikes has been supporting equities and weighing on the US dollar during the bank's blackout period. I believe these great expectations have gone too far, opening the door to a greenback comeback.

First, let's clear out the obvious – the Fed is set to raise interest rates by 75 bps for the fourth time in a row. That would put the Federal Funds rate at a range of 3.75-4%, up from 3-3.25%. Fed Chair Jerome Powell and his colleagues do not like surprising markets.

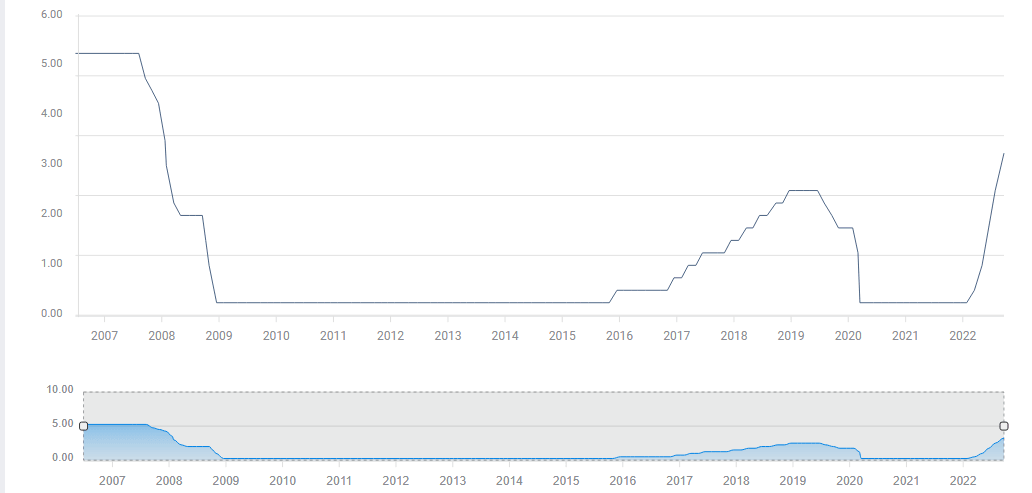

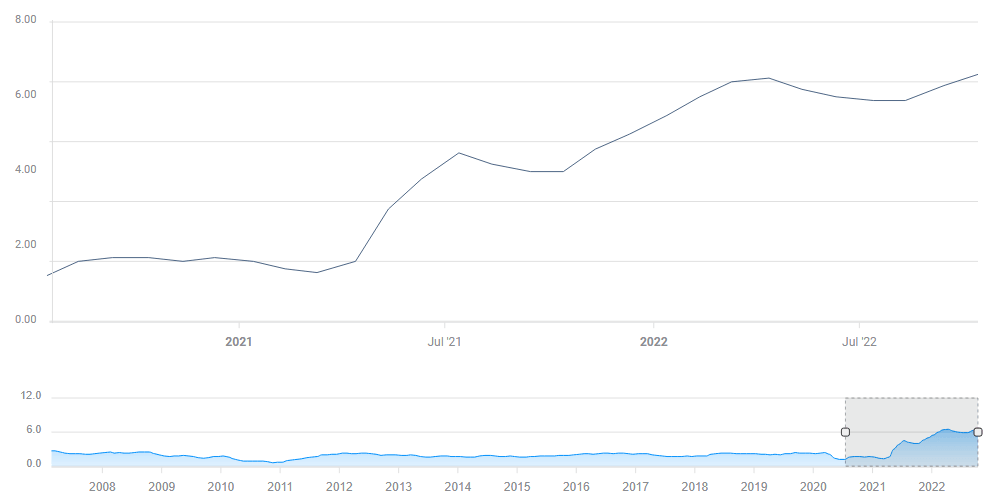

Interest rates nearing pre-2008 peak:

Source: FXStreet

The big questions are: 1) what can we expect in December, 50 or 75 bps? 2) Where will the Fed stop, roughly above 5% or under it?

Previously on Fed Watch

Super strong inflation figures published on October 13 raised expectations for a steep path of rate hikes, namely a 75 bps hike in December and even a small chance of a 100 bps move now. The peak, or terminal rate, hit 5% according to bond markets.

But then came the "dove attack" of October 21. Just before members entered a period of silence ahead of their decision, they sent two clear signals of a more moderate path. First came out Nick Timiraos of the Wall Street Journal – aka "the Fed whisperer" – subtly hinting a potential slowdown in December.

Second, San Francisco Fed President Mary Daly released unscheduled remarks saying she sees the peak rate staying within the limits of the Fed's September projections, which stood at around 4.6%. These two moves, came on top of a surprisingly dovish remark from James Bullard, known as the uber-hawk. He said 2023 could be "disinflationary."

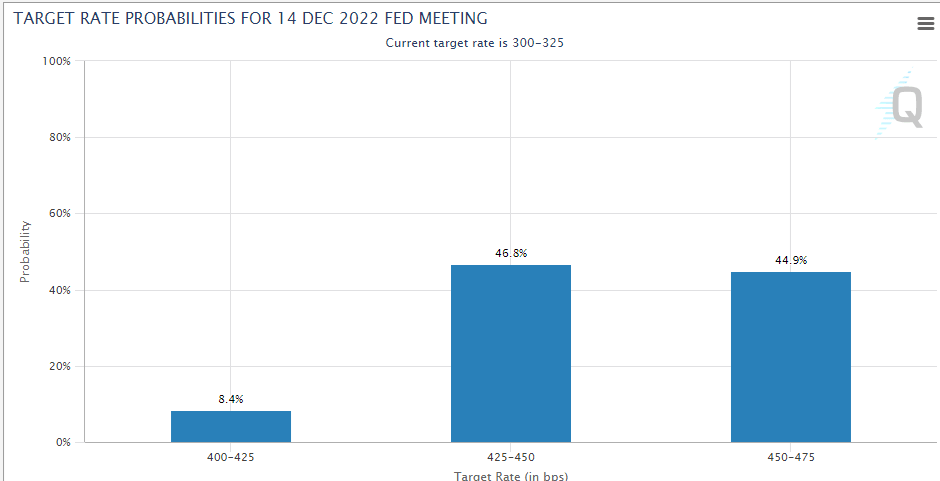

The probability of a 75 bps hike in December stands at only 44.9% at the time of writing:

Source: CME Group

The expectations game continues until the last moment. A fresh piece from Timiraos over the weekend focuses on consumers' big cushion of savings and corporations' lower debt-servicing costs. To make things clear he says:

For the Fed, a more resilient private sector means that when it comes to rate rises, the peak or “terminal” policy rate may be higher than expected.

He already hints at peak rate expectations gone too far and that may already skew the expectations.

But apart from expectations, what do the data say? Has the Fed done enough?

Tentative signs of a slowdown

The housing market feels rising interest rates more than any other. Mortgage rates for 30 years have hit 7%, pending home sales tumbled by some 10% and house prices fell by 1.3% in August, according to Case Shiller. Year over year, costs are undoubtedly undoing, reversing some a considerable chunk of the pandemic boom.

Source: FXStreet

As the Fed's policy works with a lag, perhaps it should take stock of its achievements in the housing market, expecting broader prices to fall. However, the labor market is doing well, seeing 263,000 jobs gained in September, according to the latest Nonfarm Payrolls report. The pre-pandemic average was 200,000.

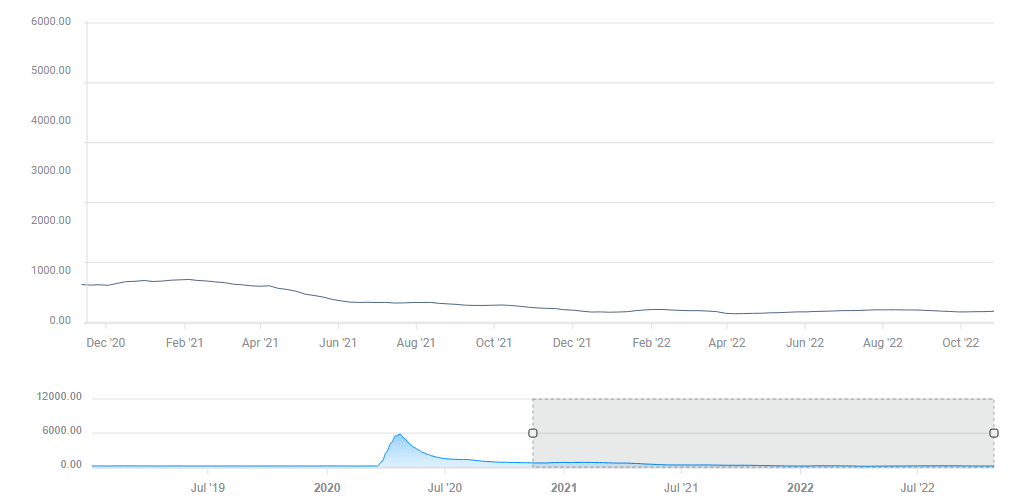

The Fed is fully willing to accept pain in the jobs market as a price worth paying to see inflation down. We're not there yet. Weekly jobless claims, which provide more up-to-date data on employment, show strength.

Weekly jobless claims stood at 219,000 in the week ending October 21, within pre-pandemic levels. Even if there is a lag, the Fed should do more.

Source: FXStreet

The Fed's focus is inflation, and there was an encouraging sign coming from third quarter Gross Domestic Product figures, which pointed to a moderation in headline inflation. Nevertheless, the Fed is worried about core inflation, excluding volatile energy and food costs. And there, it is hard to find any softening.

While Core PCE – the Fed's favorite underlying inflation gauge – missed estimates with 5.1% YoY in September, the monthly figure came out at 0.5%, as expected. Moreover, Core CPI, hit 6.6% YoY last month, the highest since "Eye of the Tiger" topped charts 40 years ago.

Three reasons to go hawkish

Even if there are signs of a slowdown in the US economy, it is hard to signal that the battle against inflation is at "the beginning of the end." I expect the Fed and its Chair Jerome Powell to provide a hawkish message for three reasons.

First, high core inflation shows it is too soon to change the tone. While Fed officials may share different takes on the current state, the most important comments come from the person at the top – and after setting rates, the impactful timing. It is too soon to send consumers a calming message.

Source: FXStreet

Secondly, the Fed announces its decision just six days before the mid-term elections, with inflation topping the list of concerns for voters. It would be politically unwise of Powell to provide even the smallest signal of easing off at this juncture. He needs a poor jobs report to be able to send a more dovish message to the public.

Third, the market has already lowered expectations more than enough. Bond yields have dropped and stocks have bounced. Markets tend to go too far, and I suspect that is the reason for Timiraos' weekend article.

What to watch out for

At November's meeting, the Fed does not release new forecasts, emphasizing other things, mostly Powell's tone. If he expresses worries about the housing sector, it would be dovish, but as argued above, there is a higher likelihood of a more combative tone on inflation, which would be hawkish.

Powell is set to clarify that the Fed is data dependent and makes its decisions on a meeting-by-meeting basis, without even hinting of any potential outcome in December. The mere uncertainty could be enough to scare stocks and boost the safe-haven dollar.

He is also likely to downplay the importance of the Fed's forecasts, saying they could change. That would be a hint that the terminal rate could exceed 5%.

A surprise dissent in the vote for the expected 75 bps hike could also trigger a small knee-jerk reaction. As such a move has been well-telegraphed, the chances are slim.

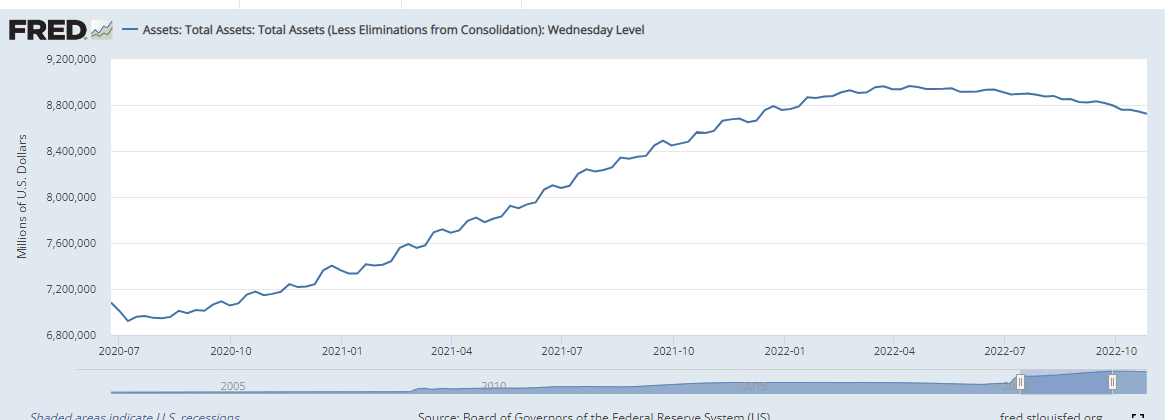

One thing that could steal the show would be comments about the Fed's balance sheet. The bank is withdrawing $95 billion out of markets every month, in a process known as "Quantitative Tightening."

Source: Federal Reserve

Will worries about future liquidity issues lead the Fed to consider slowing it down?

If Powell says it is under discussion, it will send a dovish message, while insisting it is off the agenda would send a hawkish one. Markets and the Fed are focused on interest rates, but without clarity on the topic, only "data dependency," any commentary on the balance sheet could grab the spotlight.

Final thoughts

A 75 bps hike is fully priced in, and what matters is hints about what's next. Despite signs of a slowdown, it is probably too soon to signal a slowdown, contrary to other central banks. There is a greater chance the pivot will have to wait.

I want to stress that the Fed decision is a multi-faceted event, including the rate decision, the press conference and several waves of reactions by analysts and markets. A straightforward reaction like the dollar surge in response to inflation reports is unlikely. Price action is set to be two-sided and choppy, so trade with care.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.