Fed Preview: Taking a break after two months of madness? Addicted markets may fall, dollar rise

- The Federal Reserve is set to leave its policy unchanged in the first scheduled meeting since January.

- Some may fear the bank has run out of ammunition after massive moves in response to coronavirus.

- Stocks may fall and the safe-haven dollar may rise in response.

Throwing the kitchen sink sounds like an understatement to what the Federal Reserve has done so far in face of the coronavirus crisis. When it seemed it had already exhausted its weapons, the world´s most powerful central bank surprised again and again. Markets have recovered in recent weeks and the Fed may find it unnecessary – as well as hard – to find any additional tools in its shed. By acknowledging the calm as the economy continues suffering, it may contribute to fueling a new fire.

Two months of madness

The bank kicked off its response to the coronavirus crisis on February 28, when Jerome Powell, Chairman of the Federal Reserve, issued an extraordinary statement vowing to support the US economy.

A few days later, the bank announced an unscheduled meeting in which it slashed the Federal Funds Rate by 50 basis points to 1%, later eliminating the borrowing cost to zero – in a rare Sunday announcement to front-run the market open.

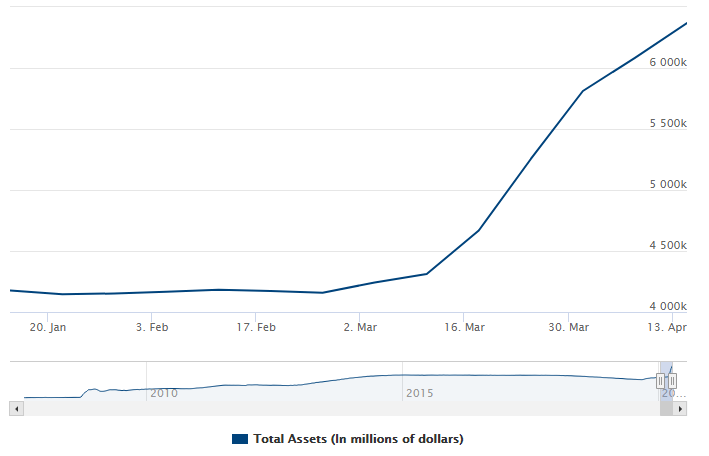

The Fed also reignited its Quantitative Easing programs, initially announcing the purchase of some $700 billion in government bonds and Mortgage Based Securities (MBS) and later kicked off unlimited QE – the nuclear option. The bank's balance sheet has neared $6.4 trillion as of April 14, up some 50% since the beginning of the year and easily surpassing the previous peak of around $4.5 trillion.

Source: Federal Reserve

The Washington-based institution also addressed the funding distress in markets that led to March's "sell-everything" mode and the rush to the dollar. It launched swap lines with major central banks before expanding them and adding additional peers.

Bond-buying has been expanded into corporate debt, including "fallen angels" – a nice term used to describe junk bonds that have been downgraded to that status recently. The Fed's most-recent significant move was veering into lending in various Main Street programs totaling a whopping $2.3 trillion, in addition to frequent announcements of liquidity injections.

Powell's powerful action – including massive money-printing – has calmed markets but may still be dollar-positive.

What else can the Fed do?

After so much action since late February, can Powell provide surprises at the end of April? The upcoming meeting is the first scheduled one since January, as the Fed skipped its planned one in late March. Back in mid-February, Powell said that he would use "aggressive" forward-guidance if needed. While he did far more than pledging support, the bank might release new forecasts, serving as guidance for markets.

The US economy lost well over 20 million jobs since mid-March and consumption collapsed by 8.7% last month. Forward-looking Purchasing Managers' Indexes are pointing down. On the other hand, coronavirus statistics have been suggesting that the US has potentially reached a peak.

The bank releases its growth, employment, inflation – and most-importantly interest rate projections – in its March, June, September, and December meetings. As it missed last month's scheduled event, it will likely publish them now. If projections take a deep dive, it would imply that the Fed will continue doing whatever it takes.

However, downbeat projections would also depress markets as they dampen companies' prospects. In turn, the safe-haven dollar may benefit from fresh demand.

Apart from the forecasts, the Fed's statement and Powell's press conference – implementing social distancing measures and potentially via video – will move markets. If officials convince markets that they have additional tools at their disposal, investors may react positively and the greenback may give ground.

Monetary financing?

However, if the pledge to support the economy is vague and especially if Powell seems reluctant to act, markets may turn down and the greenback could see fresh demand. The notion that the bank has run out of ammunition may scare investors.

The path to recovery depends first and foremost on winning on the health front. Without keeping COVID-19 cases and deaths down, the reopening of the economy will be sluggish. The second factor is the stimulus from the federal government. Lawmakers have approved several aid packages and could do more.

The Federal Reserve could pledge to but any bond that the government issues – going towards Modern Monetary Theory (MMT). In that case, the dollar would fall as markets would find new hope.

Will Powell open the door to unlimited money printing going directly to the government? The Fed has shown – int he 2008 crisis and now – that it is ready to do the unthinkable. However, that step will probably wait for another day.

Conclusion

The Federal Reserve' April meeting may provide insights about how the bank sees the economy after two months of coronavirus carnage and massive monetary support. Inaction amid potential inability to act may weigh on markets and boost the dollar. If the Fed convinces markets that it has more tools – or the extreme and unlikely case of considering MMT – the dollar would fall.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.