Fed preview: Opening the door but not pre-committing

-

We expect the Federal Reserve to maintain its monetary policy unchanged next week. Focus will be on upcoming rate cuts, which we expect to begin in September.

-

The two latest CPI prints have built significant confidence in inflation remaining en route to target, but with the economy still on a stable footing, we doubt Powell feels the need to pre-commit to rate cuts quite yet.

-

We expect the Fed to cut rates twice by 25bp this year, while markets price in a cumulative 64bp of cuts by year-end. We see risks skewed towards modestly higher short-end rates and lower EUR/USD during the press conference.

After Powell and Waller confirmed the Fed feels no urgency to cut rates just ahead of the blackout, markets have mostly priced out any speculation of a rate cut next week. With no new economic and rate projections on the agenda, the meeting’s focus will be fully on any communication around the start of rate cuts later in the fall.

We still like our call for quarterly rate cuts starting from September, while markets have swung from pricing only one 25bp cut this year to now pricing a cumulative 64bp by yearend and 142bp over the next year. The Fed could deliver a faster series of cuts if it believes the economy is on a brink of an abrupt slowdown, but we do not believe this is the case today. We list three arguments for why the Fed is likely to opt for a more gradual pace:

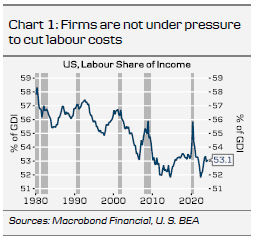

1). Labour markets are cooling, but not collapsing: The unemployment rate has risen to 4.1% from the low of 3.4% reached in April 2023, but largely as a result of rebounding labour supply. Number of layoffs remains historically low, because labour costs are not yet pressuring firms’ margins, given that that labour share of income remains modest (Chart 1). Labour demand has normalized to pre-pandemic levels, but as long as firms hold on to their existing workforce, this is not a signal of recession to come.

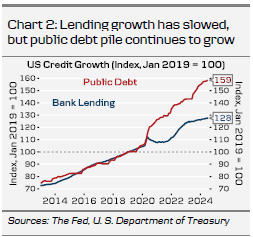

2). Fiscal policy continues to counteract tight monetary policy: Bank lending and broader credit growth remain muted, but rapid expansion in public debt continues to counteract the restrictive effect of higher rates (Chart 2). November election outlook will not materially impact the Fed’s decision making over the 1-year horizon.

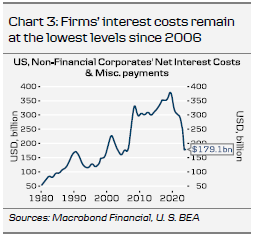

3). Fixed interest rates limit pressure on firms’ margins: Non-financial corporates’ net interest costs remain at post-GFC lows due to fixed-rate financing (Chart 3). High interest rates mean that expanding business is costly, but companies are not struggling with their existing loans for now. When firms are not pressured to cut costs, labour markets remain steady, in turn supporting consumer confidence.

The Fed will have access to the results of Q3 Senior Loan Officer Opinion Survey (SLOOS, due for public release on 5 Aug), which we expect to signal still weak credit demand as real interest rates remain at restrictive levels. We pencil in gradual cooling in both economic activity and inflation towards year-end but do not foresee a recession. As such, we doubt Powell feels the need to pre-commit to rate cuts at this point, which could spark a modestly hawkish reaction in the markets. Any more explicit guidance towards cuts either in the press release or during the press conference would have the opposite effect.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.