Fed Preview: Five dollar-moving things to watch out for on the historic tapering announcement

- The Federal Reserve is set to announce the tapering of its bond-buying scheme.

- Markets will be watching the start date and pace of this purchase reduction.

- Comments on inflation, employment and future rate hikes are also set to move the dollar.

History does not repeat itself but often rhymes – the Federal Reserve has averted a 2013-style taper tantrum when it laid down the groundwork for the move. The time has now come to announce the cutting down of its $120 billion/month bond-buying scheme. That is priced in – but the devil is in the details.

Taper buildup

In the bank's last meeting in September, Fed Chair Jerome Powell explicitly said tapering in November is high on the agenda and also set a general end-date to that process, mid-2022. Inflation has met the threshold of "substantial further progress" set by officials and employment has "all but met" that goal according to Powell. Despite another downbeat Nonfarm Payrolls report – 194,000 in September – there is a consensus that it was sufficient to warrant printing fewer dollars

The Fed's meeting minutes from that gathering added even more details – a planned reduction of $15 billion in monthly bond-buys from mid-November or mid-December, thus making the process eight months long.

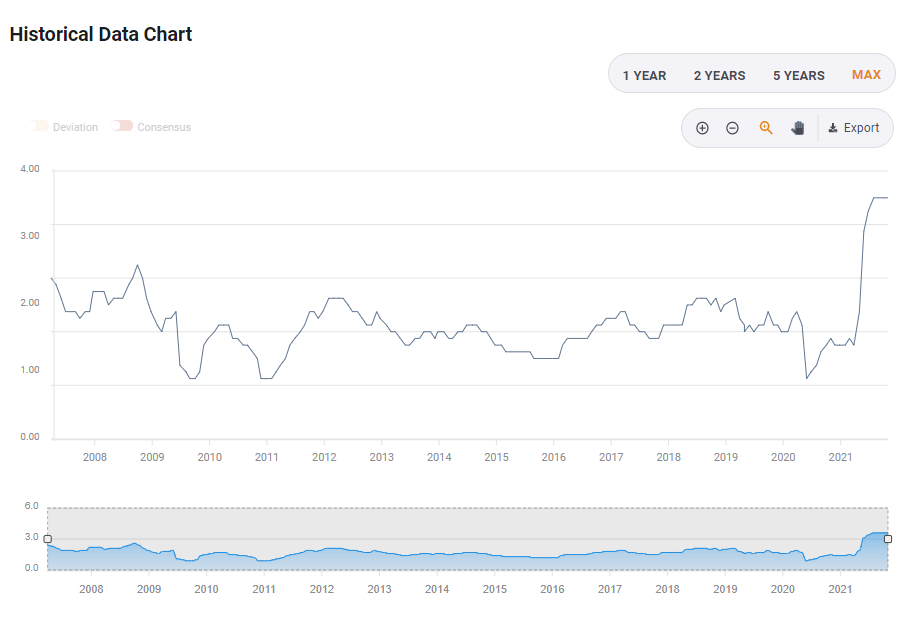

Since then, inflation, as measured both by the Consumer Price Index and the Personal Consumption Expenditure (PCE) remained high. More importantly, underlying inflation – excluding food and energy – refused to cool down. Core CPI stood at 4% in September and Core PCE at 3.6%, well above 2% that the Fed aims for.

Core PCE at multi-year highs:

Source: FXStreet

In his latest comments before the blackout period, Powell seemed more worried about inflation and more eager to act – raising speculation of a more aggressive move.

The Fed's November 3 meeting is taper time – that is the consensus, and it is fully priced in. Markets are still set to rock, responding to these five crucial details.

1) When?

The Fed makes its announcement in early November but could lower the pace of bond buys later on. Given the recent rise in inflation, it seems more likely that the reduction would happen fairly soon, either immediately or by the middle of the month. In this case, there would probably be a limited impact.

However, if the bank opts for mid-December – when market activity calms ahead of the holidays, the dollar could suffer. Any delay to the start date would not only mean more money creation but also postpone the timing of the rate hike.

2) At what pace?

The Fed will likely stick to the script from the Minutes, announcing a total reduction of $15 billion every month – $10 billion in government bonds and $5 billion in Mortgage-Based securities. That would be dollar-neutral or somewhat bearish for the greenback.

However, if fears of rising prices worry the Fed in November more than in September, it could opt to accelerate that process to $20 billion per month, thus concluding tapering within six months – and thus bringing forward expectations for the first post-pandemic rate hike. That would be significantly dollar-bullish.

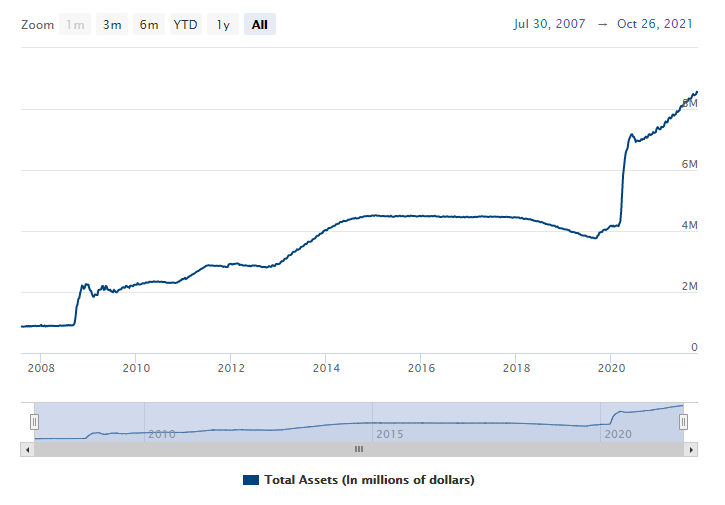

The Fed's balance sheet has leaped at the wake of the pandemic and has been growing fast:

Source: Federal Reserve

3) What does Powell say about inflation?

In the previous press conference, the Fed Chair refrained from using the adjective "transitory" when referring to price rises. That, alongside comments about inflation being sustained for longer, have been acknowledgments of reality.

If he says that this situation is set to be sustained into the second half of 2022 and then calm, that would be dollar-neutral, as he would be echoing economists and fellow central bankers. It could be seen as "long transitory."

However, if he conveys a message of concern about price rises becoming sustained – for example through wage hikes– it would send the dollar higher, as it would mean the Fed is ready to act more aggressively to fight inflation, potentially by raising rates.

Conversely, if Powell points to global supply chain issues as the culprit for rising core prices – energy is another issue – then it would be dollar-negative. Why? He would be stating what seems obvious, that monetary policy cannot solve jams at ports.

4) How much slack is there in the job market?

Earlier in the recovery from the pandemic, Powell stressed that millions of unemployed Americans have yet to return to work, making the case for more monetary support. While the jobless rate dropped below 5%, a satisfactory level in absolute terms, it is based on substantially lower participation in the labor force – 61.6% as of September vs. around 63% beforehand.

The gap in participation has yet to be closed:

Source: FXStreet

Some have taken the pandemic as an opportunity to retire earlier and others are part of what is dubbed "The Great Resignation" – people rethinking their jobs and careers on the sidelines. The mix of demography, structural changes – and also more than 10 million open jobs – has left many economists puzzled about how much slack there is the workforce.

If Powell reiterates that he wants to see more job gains before tightening policy, it would be bearish for the dollar.

However, if he acknowledges that fewer people are on the sidelines and suggest America is closer to full employment, it would imply faster tightening. That would boost the greenback.

5) When will the Fed raise rates?

A direct answer is unlikely and there is no new "dot-plot" accompanying this decision. However, Powell may take two different approaches which would be critical to the dollar's reaction. It may come in a response to a reporter's question.

One approach would be to stress that the end of the tapering process does not indicate interest rates would rise immediately afterward. Such a message could balance a more hawkish tapering path, for example of $20 billion per month. In that case of emphasizing that raising borrowing costs is a distinct and more remote decision, he would send the dollar down.

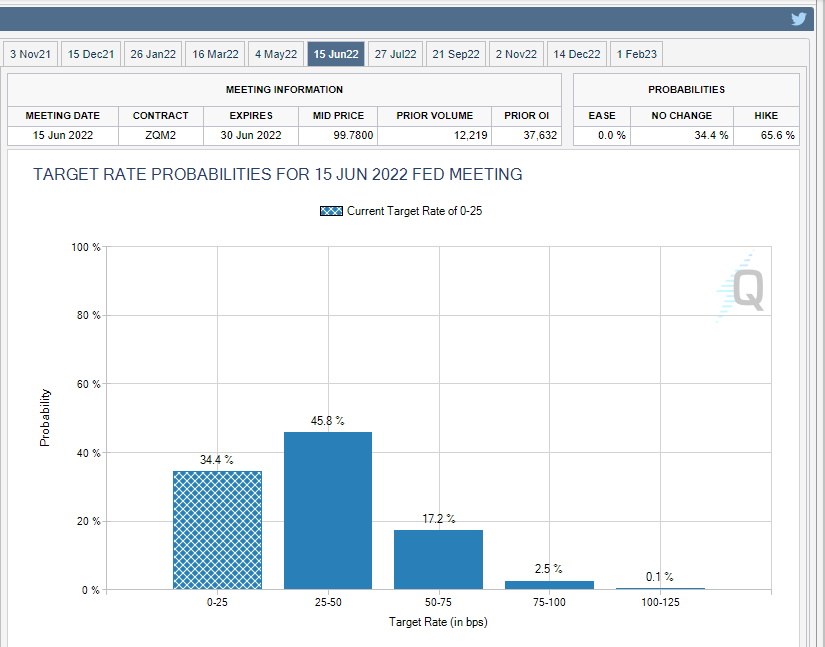

Conversely, markets are pricing in a two-thirds chance of a rate hike already in June and Powell could tacitly endorse that view just by refraining from a straight answer. That would be seen as not pushing back against market expectations – an endorsement of sorts that would raise speculation of an early hike – and send the greenback roaring higher.

Source: CME Group

Conclusion

The Fed is set to announce tapering and markets are interested in what's next. An early start, fast pace, hawkish view on inflation, a view that that the labor market is tight – and no rejection of market expectations would send the dollar up. Taking tapering slowly, blaming inflation on supply chains, seeing slack in the labor market and calling for patience on rates would be dollar negative.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.