Fed March Meeting Preview: Too many moving parts

- Fed is forecast to lift its policy rate by 25 bps to 4.75-5% after March policy meeting.

- Fed's dot plot will reveal the revised terminal rate projection.

- There are too many uncertainties surrounding Fed's policy outlook after SVB crisis.

The US Federal Reserve (Fed) will announce its interest rate decision and release the revised Summary of Economic Projections (SEP), the so-called dot plot, on Wednesday, March 22. Markets expect the Fed to raise its policy rate by 25 basis points to the range of 4.75-5% but there are too many uncertainties surrounding the US central bank’s policy outlook in the wake of the market turmoil that started with the collapse of Silicon Valley Bank (SVB).

Here is a timeline of what happened:

- March 10, Friday: SVB failed after a run on deposits that started on Wednesday, March 8.

- March 12, Sunday: The Federal Deposit Insurance Corporation (FDIC) took control of the New York-based Signature Bank.

- March 12, Sunday: The Fed introduced Bank Term Funding Program (BTFP) to provide additional funding to depository institutions.

- March 13, Monday: HSBC announced that it will be buying SVB’s UK business. Small and medium-sized US banks’ shares suffered heavy losses with the First Republic Bank stock falling nearly 60%.

- March 15, Wednesday: Shares of Credit Suisse fell nearly 30% after the bank’s biggest investor, Saudi National Bank, said that it will not be providing financial support due to regulatory restrictions.

- March 15, Wednesday: The Swiss National Bank (SNB) and the Swiss Financial Market Supervisory Authority (FINMA) came out with a statement late Wednesday, saying that Credit Suisse met the capital requirements to receive additional liquidity.

- March 16, Thursday: European Central Bank (ECB) raised key rates by 50 basis points (bps) as expected. During the press conference, ECB Vice President Luis de Guindos said that banks in the Eurozone were resilient with a “robust liquidity position.”

- March 16, Thursday: First Republic Bank received $30 billion in deposits from 11 big US banks.

- March 16, Thursday: Credit Suisse said it will borrow $54 billion from the SNB.

- March 19, Sunday: Swiss authorities persuaded UBS Group AG to buy Credit Suisse to contain the banking crisis.

- March 19, Sunday: The Federal Reserve (Fed) announced that it will offer daily swaps to the Bank of Canada (BoC), the Bank of Japan (BoJ), the SNB and the ECB to ensure they have enough liquidity to continue operations.

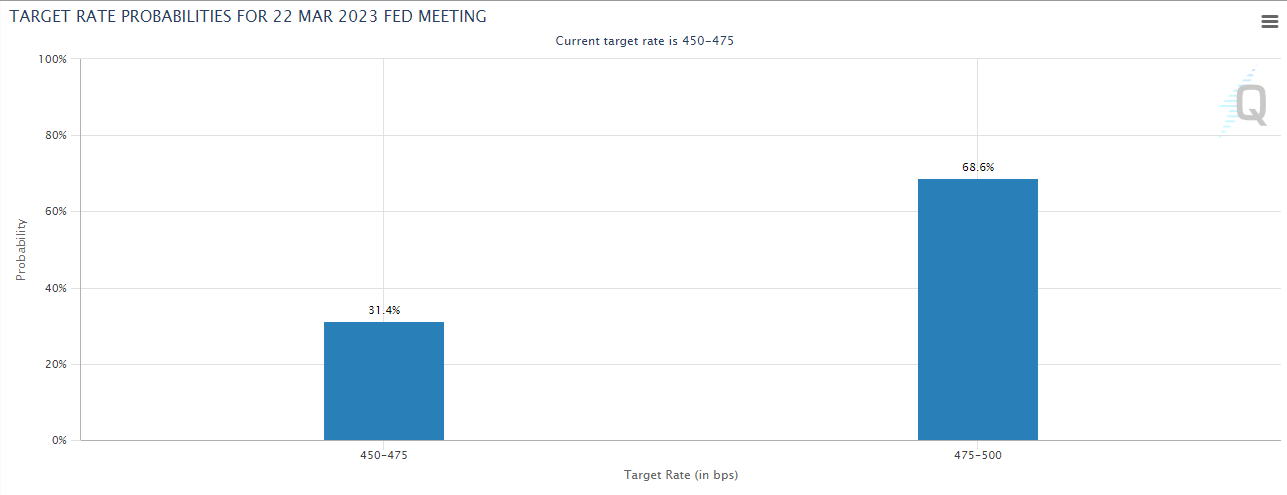

At the time of press, the CME Group FedWatch Tool shows that markets are pricing in a nearly 70% probability that the Fed will hike its policy rate by 25 bps. It’s worth noting, however, that that probability dropped below 50% several times since the beginning of the turmoil.

Dovish scenario

The obvious dovish shift in the Fed’s policy would include a no-change in the policy rate. It’s not easy to figure out the possible market reaction to such a decision. On the one hand, this move could provide some relief to markets by suggesting that the Fed will prioritize stabilizing financial markets in the near term by lifting its foot off of the tightening pedal. However, investors could also see that as an alarming sign that things are worse than they appear to be. Even though a dovish outcome is likely to hurt the US Dollar, safe-haven flows could help the currency stay resilient against its rivals.

In case the Fed raises the policy rate by 25 bps but the dot plot shows at least one rate cut before the end of the year, that could also be assessed as a dovish shift in the policy outlook. Unlike the above-mentioned scenario, this stance is likely to weigh on the USD without triggering a flight to safety.

Hawkish scenario

Although it’s extremely unlikely, a 50 bps Fed rate increase should trigger a rally in the US Treasury bond yields and the US Dollar Index, given the current market positioning.

If the Fed opts for the 25 bps hike, a terminal rate projection above 5.5% with the SEP showing no rate cuts this year should trigger a similar but less-severe market reaction.

Neutral scenario

A 25 bps rate increase with a terminal rate projection at or below 5.5% should make it difficult for markets to find direction. FOMC Chairman Jerome Powell’s comments on the policy outlook could provide valuable insights into the policy outlook.

If Powell downplays the growing fears over a global financial crisis and notes that they will remain focused on battling inflation, this is likely to be assessed as a hawkish tone. In case Powell reiterates the data-dependent approach and refrains from committing to specific policy steps in the future, that could be seen as neutral. Finally, it could be seen as a dovish shift in language if the chairman says that they could adjust interest rates to respond to a possible further tightening of financial conditions.

Summary

The Fed faces a tough balancing act as the negative impact of higher interest rates on the banking sector becomes more apparent by the day. Meanwhile, latest data reaffirmed that labor market conditions remain tight and inflation is still sticky with core services prices holding uncomfortably high.

The Fed is unlikely to use interest rates as its primary tool to ease financing conditions. The US central bank already took several actions to help the banking sector out.

At this point, it’s very difficult to foresee how the Fed’s policy will be shaped in the remainder of the year. The significant daily changes on the Fed’s rate hike probabilities witnessed in the past 10 days highlights the increased uncertainty created by the changing economic environment. Thus, it would be very risky to commit to a specific market position, at least until the Fed dust settles toward the end of the week.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Eren Sengezer

FXStreet

As an economist at heart, Eren Sengezer specializes in the assessment of the short-term and long-term impacts of macroeconomic data, central bank policies and political developments on financial assets.