![]() ING Global Economics Team

ING Global Economics Team

ING Economic and Financial Analysis

Elevated inflation and strong activity and jobs numbers have pushed market expectations for the timing of the first interest rate cut to December. We still see an opportunity for a September rate cut. Nonetheless, the Federal Reserve will remain wary and signal that if inflation stays high, so will interest rates.

Robust data forces the Fed to sound less dovish

At the March FOMC meeting, the Fed stuck with the view that the most likely path forward involved three 25bp interest rate cuts in 2024 with a further three in 2025. While they won’t be updating these forecasts again until June, the fact that inflation continues to run too hot for comfort and that the economy is still growing strongly suggests a more cautious take on prospects for policy easing at next Wednesday’s FOMC press conference.

Core CPI has come in at 0.4% month-on-month for three consecutive months, more than double the rate we need to see to bring inflation down to 2% year-on-year over time. Meanwhile, the consumer continues to spend aggressively and the economy added 829,000 jobs in the first three months of the year. This led Fed Chair Jerome Powell to state on 16 April that “recent data have clearly not given us greater confidence” that inflation is coming under control and “instead indicate that it’s likely to take longer than expected to achieve that confidence.” He additionally warned that “if higher inflation does persist we can maintain the current level of restriction for as long as needed.”

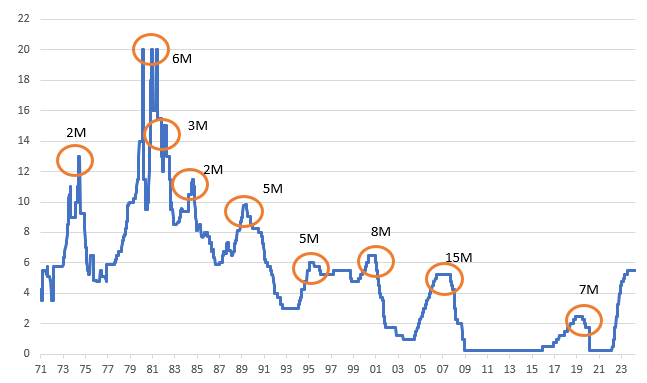

Fed funds ceiling rate with time period between last rate hike and first rate cut (%)

Source: Macrobond, ING

Surveys still suggest a case can be made for a September rate cut

Consequently, markets are now pricing next to no chance of any action on 1 May with only 3bp of cuts priced by June, 20bp by September and 36bp by December. This is a remarkable swing given it was only three months ago that the market was fully discounting 150bp of rate cuts this year starting at the March FOMC meeting.

We are forecasting the first move coming at the September FOMC meeting with two further cuts in November and December. Business surveys suggest more and more caution on the outlook for the economy with employment components pointing to a pronounced slowing in hiring in coming months. We also expect inflation to gradually converge on 2% as cooler economic activity and subdued labour cost growth help dampen price pressures, which in turn is compounded by softening pricing power. Nonetheless, there is little sign of this happening just yet and the risk remains that the Fed ends up bringing interest rates to a more neutral level more slowly and over a longer period than we are currently forecasting.

Treasuries remain under pressure on soft policy versus the implied inflation threat

With the Federal Reserve a tad slavish to inflation data, the focal point of the curve is the 10-year rather than a stable funds-rate-bullied front end. That makes the curve quite directional, meaning that the shape of the curve is coming from longer tenors. Without a new impulse from the Fed, and with inflation continuing to tick firmer than comfortable, the 10-year Treasury yield is liable to continue to trek towards the 5% area, steepening the curve from the back end. That said, should the Fed surprise us and get ahead of this with some hawkish commentary, and even go as far as threatening a hike, then we could see the 10-year yield come off its highs on the theory of more Fed inflation protection.

The FOMC will likely continue its discussion on balance sheet roll-off, too. Policymakers have already intimated an intention to cut the pace of roll-off in half, with particular reference to the pace of the Treasury bond roll-off. The Mortgage-Backed Security roll-off remains behind schedule in any case, on account of a lower pre-payments profile. In fact, the slower MBS roll-off results in the aggregate roll-off pace being around $75bn per month, rather than the $95bn per month originally planned. Meanwhile, liquidity conditions remain ample, with bank reserves still elevated in the US$3.3tn area, and cash going back to the Fed on the reverse repo facility still in the US$440bn area. We think there is a comfortable US$0.75tn liquidity excess in those numbers.

Data, not the Fed, in the driving seat for FX

The dollar has ended the day lower on the last three consecutive Fed meetings. In effect, the market had bought into the Fed’s communication from those meetings that the disinflation trend was visible and the Fed wanted to cut. However, the dollar has rallied 2%+ since the Fed’s last meeting in March - confirming data supremacy in FX market pricing. And with both activity and price data heading in the wrong direction for the Fed over the last six weeks, it is hard to see Chair Jerome Powell on 1 May offering much resistance to a market that is minded to buy dollars.

If the dollar is to go lower later this year, it will then have to be the data which drives it. We have recently seen the dollar selling off on the soft April US PMIs and we think there would be a good reaction lower should real sector activity finally slow or some new, reassuring signs of disinflation trends emerge. Until then, wide rate differentials, geopolitical risk and the uncertainty around the US November presidential election suggest the dollar can hold recent gains.

Read the original analysis: Fed likely to hold rates steady and warn of the risk of delay to cuts

Content disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more here: https://think.ing.com/content-disclaimer/

Recommended Content

Editors’ Picks

EUR/USD flat lines above mid-1.0900s, investors seem non-committed amid rising trade tensions

The EUR/USD pair reverses an Asian session dip to the 1.0880 area and for now, seems to have stalled its retracement slide from the vicinity of mid-1.1100s, or the highest level since September touched last week. Spot prices currently trade around the 1.0960 region, nearly unchanged for the day amid mixed cues.

GBP/USD bounces off one-month low, defends 200-day SMA and retakes 1.2900

The GBP/USD pair attracts some dip-buyers near the 1.2830 region, or over a one-month low touched during the Asian session on Monday and for now, seems to have stalled its retracement slide from a six-month peak touched last week.

Gold buyers refuse to give up amid global trade war and recession risks

Gold price is holding the quick turnaround from one-month lows of $2,971, consolidating the recent downward spiral. The extension of the risk-off market profile into Asia this Monday revives the safe-haven demand for Gold price.

Bitcoin, Ethereum and Ripple head to yearly lows while ETH hits two-year bottom

Bitcoin price hovers around $78,600 on Monday after falling nearly 5% the previous week. Ethereum and Ripple also followed in BTC’s footsteps and declined 13% and 10%, respectively, in the previous week.

Strategic implications of “Liberation Day”

Liberation Day in the United States came with extremely protectionist and inward-looking tariff policy aimed at just about all U.S. trading partners. In this report, we outline some of the more strategic implications of Liberation Day and developments we will be paying close attention to going forward.

The Best brokers to trade EUR/USD

SPONSORED Discover the top brokers for trading EUR/USD in 2025. Our list features brokers with competitive spreads, fast execution, and powerful platforms. Whether you're a beginner or an expert, find the right partner to navigate the dynamic Forex market.