Fed Interest Rate Decision Preview: Is history a guide?

- Fed 0.25% rate hike is near universal in expectation.

- Balance sheet reduction, economic and rate projections are key questions.

- Inflation will vie with recession threat in the new Projection Materials.

- Caution will be the Fed’s overriding policy.

The Federal Reserve has made its choice.

On March 16 the Federal Open Market Committee (FOMC) will raise the fed funds rate for the first time in three years in an effort to fight rampaging inflation. Historically, this would be the opening salvo in a long campaign of rate increases.

This time the question of long-term Fed policy is very much unsettled.

The problems are two-fold: Will US economic growth, particularly consumer spending, falter under the draining impact of inflation? Can the Fed continue its rate hikes even if US growth plunges or the economy enters a recession?

Until the Ukraine war the first answer seemed to be no. Retail sales were very strong in January, despite a year of surging inflation. If the consumer economy remained healthy, there was a good chance overall growth would not fade. Consumption was aided by the exceptionally tight labor market.

Ukraine has complicated the consumer equation. Were oil to remain above $100 or $125 for an extended period, the resulting jump in consumer inflation and manufacturing costs would likely precipitate a recession.

Answering the second question is straightforward. The Fed will not hike rates in a slowly-growing or recessionary US economy.

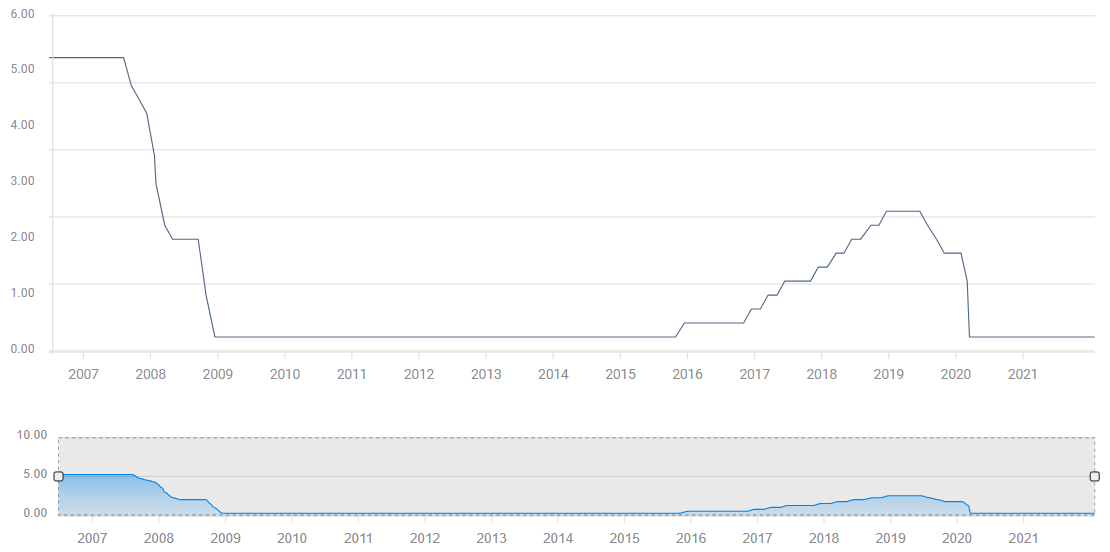

Federal Reserve rate history

The previous Fed tightening effort lasted two years, from December 2016 to December 2018, and took the fed funds from 0.5% to 2.5% in nine 0.25% increases.

That policy, begun by Fed Chairman Ben Bernanke and concluded by Chair Janet Yellen after six years of zero rates following the financial crisis of 2008, was not aimed at inflation. It was intended to ‘normalize’ rates, that is to bring bond and market returns back to their standard place in the economy.

Fed funds rate

FXStreet

Throughout that period the Consumer Price Index (CPI) was as often below the official 2% target as above and never commanded a policy response. Critics at the time questioned why the central bank was raising interest rates when neither of the traditional signals, inflation or an overheating economy, were present.

The current dilemma bears far more resemblance to the Fed’s policy choices under Paul Volker and Presidents Jimmy Carter and Ronald Reagan. Inflation was embedded in the US economy, reaching over 14% in early 1980, after years of profligate spending and a series of oil price shocks that began 1973.

Volker’s effective though brutal policy took the fed funds rate to 12% and precipitated the steepest US post-war recession, though the subsequent economic rebound led to the excellent economy of Reagan’s second term which lasted until the turn of the century.

The point of this brief rehearsal of Fed history is to highlight the main question facing the Fed: Can the US economy withstand the long series of rate hikes needed to quell inflation?

First let's look at the price and growth conditions.

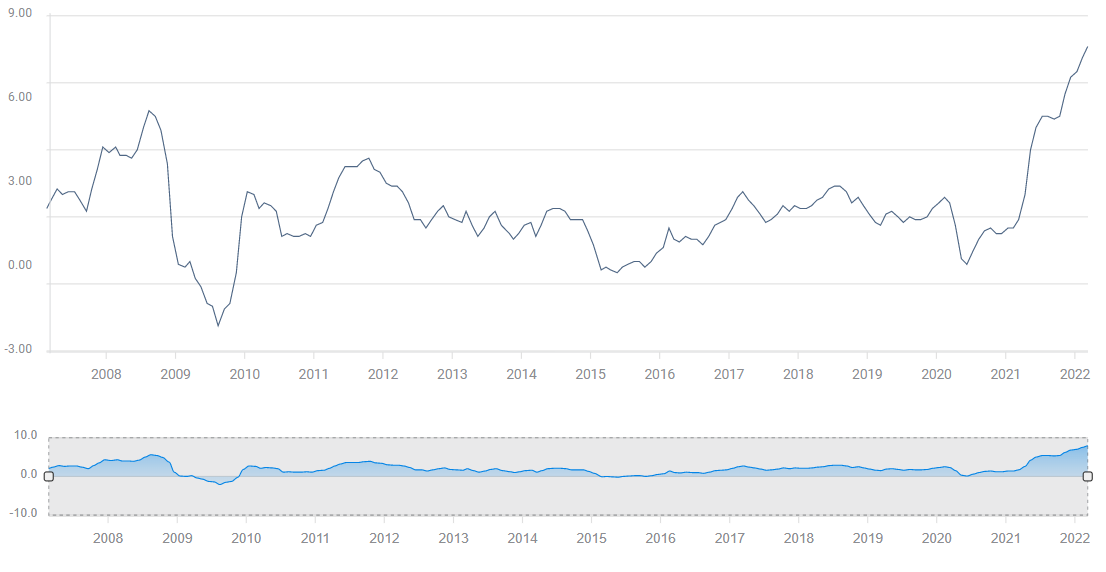

Inflation

The factors behind the astonishing increase in consumer prices in 2021 are well known.

A combination of lockdown and supply chain disruptions, government policies that encouraged labor reluctance, stimulated spending and flooded the economy with liquidity at the same time and the natural surge of consumer spending after two-years of deprivation and deferment, collided in an eminently predictable volcano of inflation.

Consumer price inflation soared 564% in 14 months, from 1.4% in January 2021 to 7.9% in February 2022. In the second half of last year, inflation became the main economic topic, as outsized increases in food, gasoline, cars and many other items, commandeered attention and converted the Fed in short order from apologist to first responder.

CPI

FXStreet

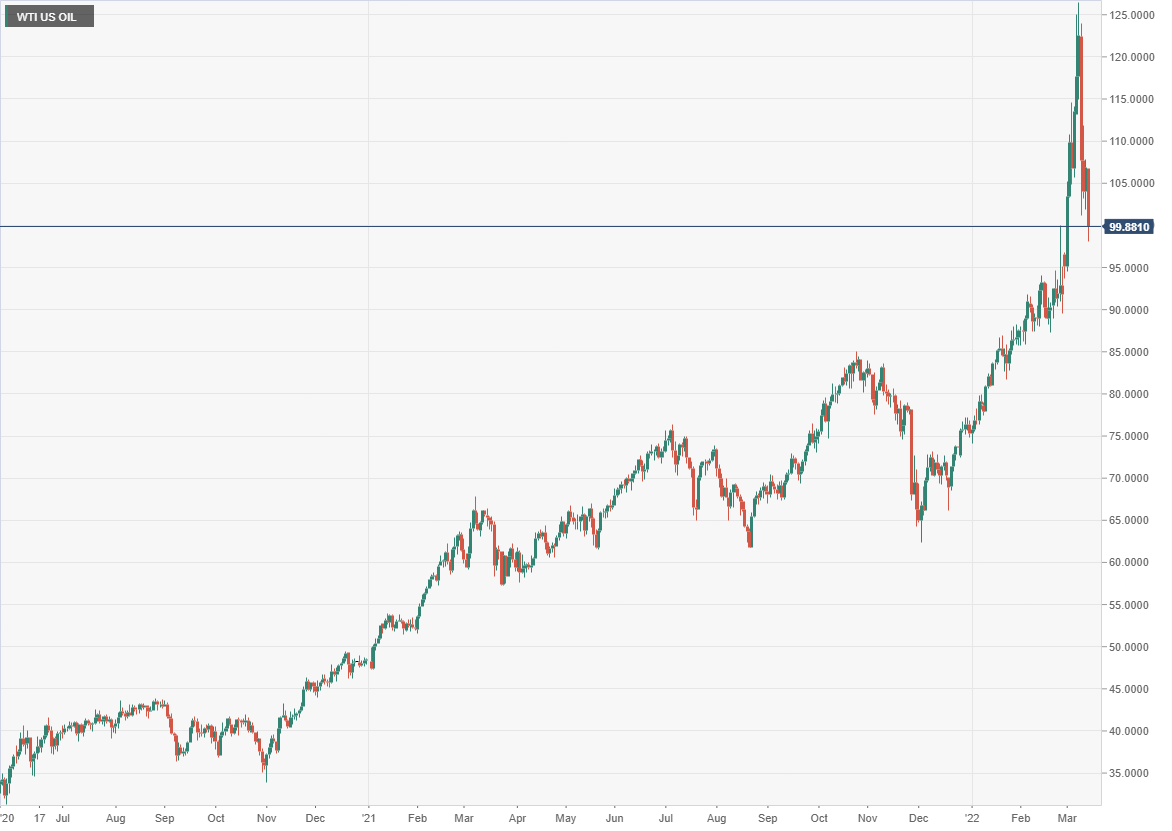

The large energy component of consumer inflation, direct in fuel and gasoline costs, and indirect in the energy component of every product and service was not a result of the Ukraine war.

Oil and energy prices began to rise long before the Russian invasion. From the November 2, 2020 open at $35.90 to that Thursday, February 24 morning, WTI had increased 162% to $91.92.

Surprisingly, the impact of the invasion on oil pricing has been small. From WTI’s opening price on February 24 as above, to its mid-morning price on Monday March 14 at $98.70, the gain was just 7.3%. Future permutations depend on the course of the Ukraine war and sanctions.

Another inflation consideration is the pandemic threat in China which has committed its health policy to eliminating Covid. Shenzhen, the largest city in Guangdong province, has ordered all non-essential businesses to suspend production and have employees work from home starting Monday. If closures were to spread to many Chinese factories, component and product shortages would give US inflation another leg higher.

US economic growth

The US economy expanded at a 7% annualized rate in the fourth quarter. In the Atlanta Fed GDP Now model, growth has fallen to 0.5% in the first quarter. That reading is supported by some statistics but not others.

American consumers are unhappy. The Michigan Consumer Sentiment Index slipped to 59.7 in March, its lowest score in a decade.

Wages have not kept pace with inflation. Real Average Hourly Earnings lost 0.8% in February, as pay was flat and CPI rose 0.8%. Over the prior 12 months US real wages fell 2.6%, leached into decline by inflation.

Other data seem undeterred. Purchasing Managers Indexes in manufacturing and services easily maintained their expansive outlook in March, though employment was weaker than expected in both and for services fell into contraction.

American firms hired 678,000 workers in February, far more than forecast, and the three-month average of 582,000 was very good. The unemployment rate fell to 3.8%, comparable to the excellent pre-pandemic economy.

Retail Sales have been uneven, 0.5% negative in the fourth quarter, up 3.8% in January. February’s result is expected to be a more normal 0.4% when released on March 16.

US economic growth, Ukraine and otherwise

In January and February, the US economy was poised to amplify the recovery that had been building for most of 2021. Inflation had not curtailed consumer spending or more importantly, hiring, despite its record increase.

After Ukraine the inflation calculus depends on the war and its long-term impact on energy prices. The upper end of the WTI range since the invasion would add nearly 40% to oil prices. Natural gas costs would rise commensurately. Such a price shock would very likely bring on a recession in the US and around the world.

The military, political and economic endgame in Ukraine is unknown.

It is doubtful Russian President Vladimir Putin will be deterred by sanctions. The military balance probably favors the Russians but it is also highly uncertain whether Putin wants the bloody disaster of an urban battlefield in Kyiv.

Market responses are tenuous and news driven. If the war accelerates into a fight for the cities of Ukraine, global oil prices will skyrocket, with all the doleful economic consequences.

If the war is settled, oil prices will fall but how far is debatable, since the rise to over $90 for WTI had nothing to do with Ukraine.

Reality will probably be somewhere between those extremes.

FOMC: Policy choices

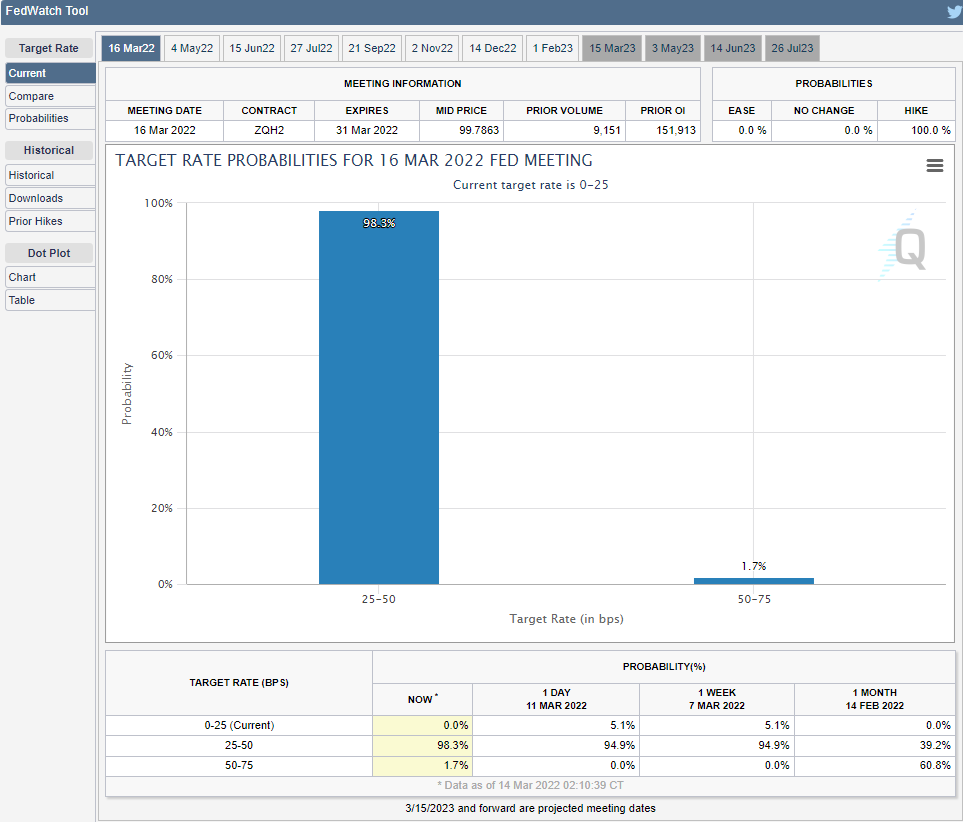

Fed choices at the March meeting fall on three topics: The fed funds rate, balance sheet disposition and the bank's economic and rate projections. The first two are policy decisions, the third results from the individual assessments of the participants collated by the bank.

Markets are certain the fed hike will be 0.25%. Fed futures on Monday had the odds at 98.3%.

CME

Under Chair Jerome Powell the Fed has stressed its policy transparency. In fact, the governors have been willing to act without warning, witness the pandemic response, and without explanation, consider the shift to inflation concern after months of transitory assurance.

Growth in the first and second quarters is more problematic than extant data shows. Inflation has not receded and when the price increases from the Ukraine war are included, CPI will move higher in the coming months. With growth uncertain but statistics still firm and inflation sure to accelerate, there is a credible case for hiking rates 0.5% this month, establishing a beachhead against prices and then waiting to see if the economy does indeed slow down.

The differential economic impact of an additional 0.25% fed funds hike is negligible, but the potential effect on inflation psychology would not be. Chances are fast rising that US growth will succumb to the inflation shock. If it does, rate hikes will halt.

Nonetheless, the Fed is not expected to take this aggressive approach.

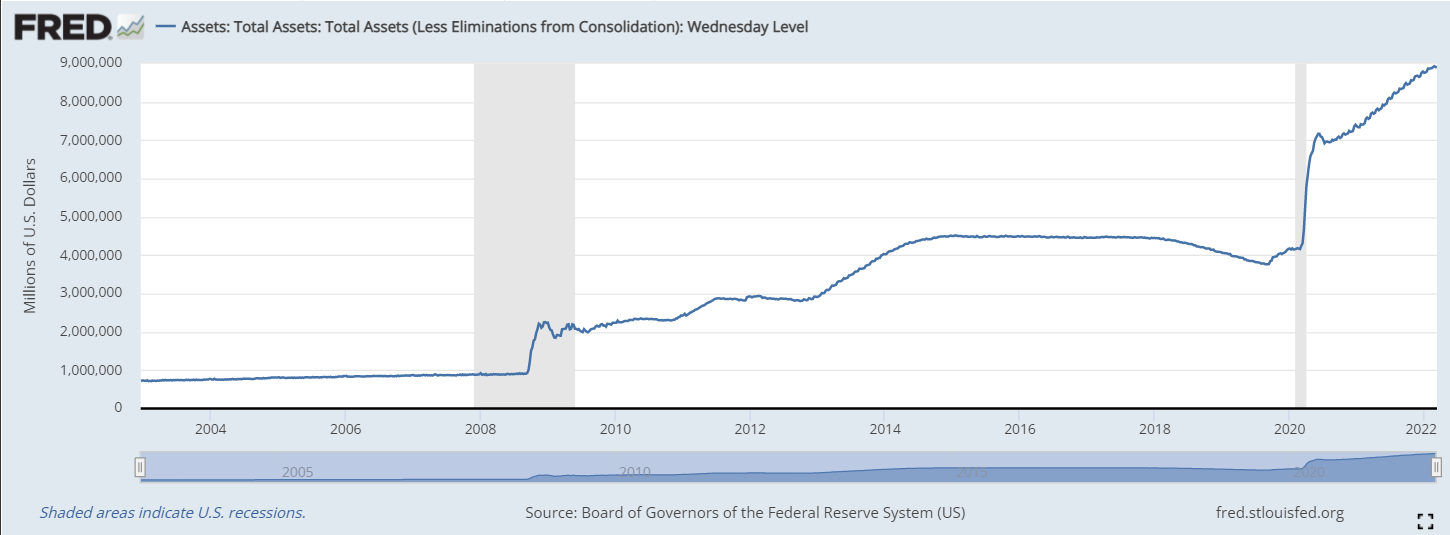

Balance Sheet

Markets are uncertain whether the Fed will begin reducing its balance sheet at this month’s meeting.

The governors have two possible methods, passive retirement or active sales. In the first, the proceeds of maturing securities are not reinvested, reducing the portfolio by established amounts each month. In the second, bank traders hit price bids in the Treasury market for whatever amount of reduction is required. Active sales would spark a sharp price decline in the Treasury market as bonds holders attempt to get ahead of Fed sales. Yields, which trade inversely to prices, would move rapidly higher.

While both options are technically possible, the rate shock inherent in active sales is an insurmountable obstacle for the policy makers.

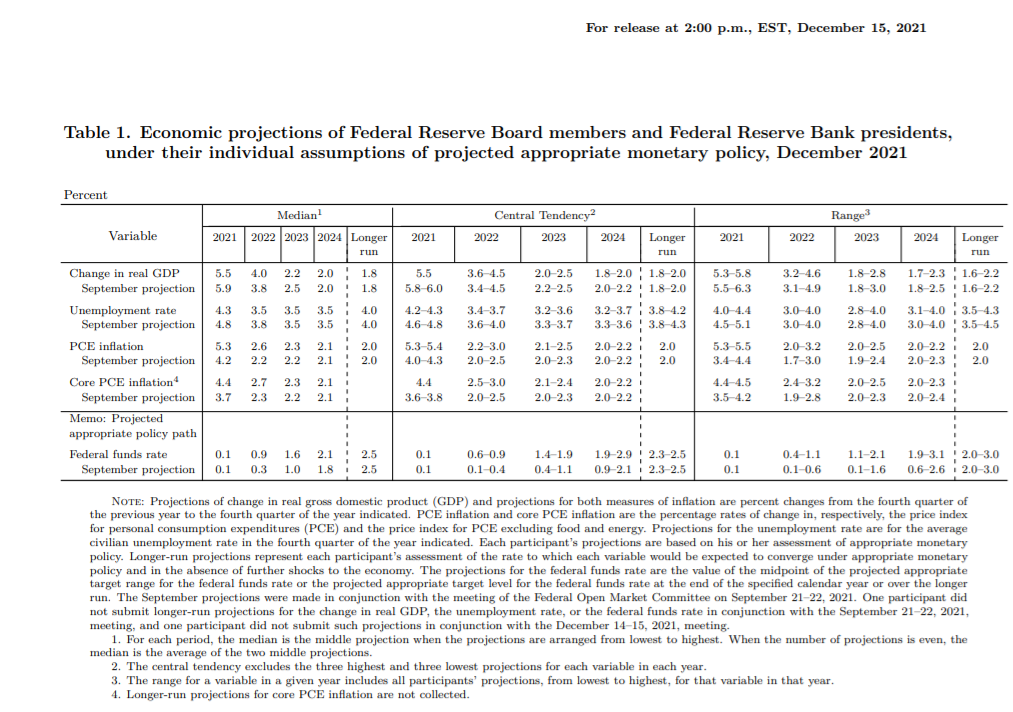

Projection Materials

The new Projection Materials are sure to see major adjustments especially in inflation, as the December version enshrined the now retired transitory analysis.

December 2021

Personal Consumption Expenditure (PCE) inflation was expected to be 2.6% this year and core PCE was to be 2.7%. Rates could easily double for the whole year and they would still be far below the current level. Do the governors and Fed economists still believe in transitory inflation?

Inflation is, in many senses, a known statistic. In relation to the Projection Materials, it is primarily a matter of what the Fed is willing to admit.

The same cannot be said for GDP. There is no market certainty about first-half GDP. December’s estimate lists 2022 growth at 4%. How much will this fall? Can it rise?

Estimates for the fed funds are the mirror image of the GDP analysis. In December, three hikes were posited, with a year end rate of 0.9%. Futures have six hikes with a year end rate of 1.50%-1.75%.

With the global and US prospects as undecided as they are, the Fed will likely be very circumspect with its projections. There is little sense in exciting markets with estimates that could change in an instant.

Market response

Markets will track the Fed’s rate and economic profile. Treasury yields and the dollar will rise with every degree of Fed rate aggression. Likewise, the higher the inflation and GDP estimates in the Projection Materials, the more secure markets will be in selling Treasuries and buying the dollar.

Equites initial reaction to rising rate prospects will likely be negative, but limited. Higher growth estimates from the Fed will work to assuage fears of and inflation-induced recession.

Economic prospects in the US and around the world are extraordinarily unsettled. That uncertainty will be reflected in Fed policy and economic projections. The governors will, in all probability, temporize and give the markets exactly what is expected to avoid any untoward reaction. Every aspect of this FOMC meeting, policy, projections and Chair Powell’s commentary will be cautious.

Even if the Fed knew the future with perfect clarity, now is not the time for bold and risky assertions.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.