European Central Bank Preview: Three reasons why Lagarde is set to lower the euro

- The European Central Bank is set to leave its policy unchanged amid fears of slower growth.

- Eurozone inflation is still below that in the US, and mostly energy-related.

- The void created by Weidmann's departure will take time to fill.

One significant gauge of inflation, breakevens are breaking down – the 5Y/5Y has surpassed 2%, hitting the highest since 2014. The European Central Bank closely watches this measure of projected price rises and may have reasons to worry and begin withdrawing stimulus. Not so fast.

Headlines about inflation, labor shortages and supply-chain hiccups have been gripping the headlines, and the ECB could react by trimming down its bond-buying schemes. The Pandemic Emergency Purchase Program (PEPP) is set to expire in March and the bank could just let it happen. In the past, officials suggested a new plan could substitute the current one.

Money markets are expecting the Frankfurt-based institution to raise rock bottom borrowing costs in addition to ending purchases. The main lending rate is 0% and the deposit rate is -0.50% –commercial banks are punished for parking money with the ECB and they will surely welcome any rate hike. However, they may have to wait, and the same applies for euro bulls.

The bank is set to leave its policy unchanged and wait for its December meeting – when it compiles new economic forecasts – to make any potential announcements. That means investors will be focused on ECB President Christine Lagarde's press conference.

Here are three reasons why Lagarde is set to lower the euro:

1) Higher inflation, but lower growth prospects

Contrary to booming America, Europe's recovery from the covid crisis has been slow and unexciting – eurozone output has yet to return to pre-pandemic levels. While the German government raised inflation projections, it said growth would be "considerably" below its previous forecast of 3.7%. Other institutions are also less optimistic.

The German IFO Business Climate reflects the cooldown, peaking in June and grinding its way down since then.

Source: FT

The ECB would be wary of withdrawing stimulus too early, for fear of killing the nascent and slowing recovery. It would prefer letting the US Federal Reserve do the heavy-lifting of tapering. That way, the resulting drop in EUR/USD would boost eurozone exports.

2) Inflation is mostly energy-related

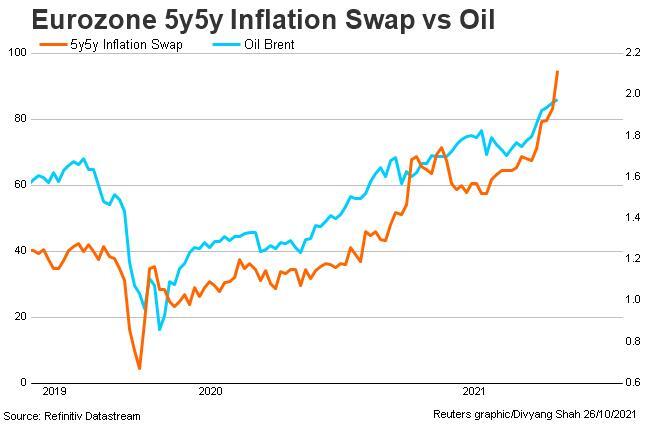

Circling back to that 5Y/5Y inflation gauge, it is clearly correlated to rising oil prices. The chart below shows how Brent Crude, the most relevant oil price for Europe, is up alongside expectations for higher prices.

Source: Reuters

Moreover, Europe's main cost crisis comes from stratospheric natural gas costs – which is related to political friction with Russia over the NordStream 2 pipeline more than anything else.

Perhaps most importantly, eurozone inflation is high in comparison to previous fears of deflation – not price rises in other places such as the US. The headline Consumer Price Index is 5.4% YoY in America vs 4% in Europe. while core CPI is 4% YoY in the US and roughly half of that in the old continent. America leads on both growth and inflation.

3) Hawks are crying

Germany leads the hawkish camp within the Frankfurt-based institution, but these inflation warriors are becoming endangered species. Jens Weidmann, the head of the German Bundesbank, recently announced his resignation. While he remains in office through the end of the year, his influence is all but gone.

After ten years at the job, his more orthodox approach to fighting inflation first and thinking about anything else later has been losing. The ECB set negative interest rates and launched a massive bond-buying scheme under then-president Mario Draghi, with Weidmann failing to change the bank's course.

Weidmann leaves a void. While his successor will probably be hawkish as well, that person would have less experience and influence. Moreover, his departure comes at a time of void leadership in Berlin – politicians are moving slowly toward a three-way "traffic-light" coalition that will have a long list of priorities apart from nominating a new Bundesbank president. In the meantime, other hawks are lonely.

The lack of leadership from those wanting to fiercely fight inflation leaves the doves to roam free. They could push Lagarde toward more bond-buying and pushback against raising rates.

Conclusion

Lower growth prospects, lesser inflation worries, and wounded hawks indicate a dovish message of ongoing support from the ECB. In turn, more euro-printing puts the common currency at a relative disadvantage against its peers, especially the US dollar.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.